For a company earning Rs 400+ crore on annual basis, whose debt stand at Rs 87 crore at the end of Sep 2015 (as per Q2 FY16 investor presentation available on company’s website) and management is focused on reducing debt asap for that company debt o/s at the end of March 2016 is Rs 90 crore.

And then we say numbers are not cooked and management is honest.

Remember what WB and charlie says, management integrity is most important thing when they acquire any company or stock.

I would not label that hyderabad based companies to be alone in game of cooking up accounts. When promoters are strong, shareholders are not bothered much, auditors are fraud, regulators are sleeping then any company be it from delhi-ncr, mumbai, kolkata, chennai, HYD or any other place will cook up accounts to either to take stock price beyond fundamental values or to divert funds from shareholders to promoter or related entities.

As I am not insider, I can’t say if LYCOS is actually earning Rs 400+ Cr or not but even if they are earning that much and neither they are paying up debt nor dividend … then its a classical case of fund diversion where money is diverted on the name of product development.

Company has spent a lot of money on the name of product development such as Lycos TV, Lycos life, Crypto currency, etc. But at the end of the day we can see very well what kind of products are all those after so much of spending.

Also management was talking about sale of patents but just see their reaction if someone ask question related to that matter on concall.

Can anybody state the reason for such a drop of lycos internet?

It’s below 15.

PE is less than 2

It something wrong going with the company’s financials?

It seems they have started a dividend (albeit very small %). This may take care of some cash diversion fears via subsidiaries that were existing

Has a low PE

Strong presence and tie-ups in adtech world (Microsoft)

fears about bankruptcy of a subsidiary in India. This was addressed in the last concall. And as per my understanding should get cleared in next 3 months with a possible High cost outgo

I made an observation about the Auditor of Lycos. Many of its clients are politically well connected. Which explains CA’s clout among politicians of South. Also many of those companies like lanco are indulged in fraud as well. I think this stock is worthless really. There is a great chance of cooking of books in this company. It’s better to stay away. Promoter doesn’t seem to follow up on promises that are being made in Concall. Their recent acquisition of worthless software ( I used that software and that’s why I can say it’s very bad software for which millions in Stock are being paid) like mysms also brings management integrity in question. I was also very confident about this company a year back. But now investing in this company seems like a treacherous path to tread.

Wonderful observation about auditor. Though subjective in nature but definitely helps to any inquisitive mind interested in triangulation. Can you share the list of Auditors who have questionable past. Would be a great help as ready recknower for investor like me.

This is going to be my last post on Lycos. Anyone having any hope on this company should read this carefully. I was reading conference call of last quarter and CEO Suresh Reddy mentioned the name of some companies that LYCOS compete with.

Admob - They doesn’t have a website but when you’ll Google it’s name, you’ll get to know that company is all about ads and they have apps, solutions for the same.

I’ll throw in inmobi as well though he didn’t mentioned it in his conference call because it’s also in advertising space. ( http://www.inmobi.com )

First you should check all these websites out. And then you should also Google their names to see what search does it throws. Most likely first link you will see is what I had shared above.

Also notice how modern these websites look (first impression is everything right? and also since they are in advertising space atleast they should make themselves presentable first). Now google “Lycos” . First link you’ll get is Lycos.in and that’s a search engine you won’t use ever in this life.

Next link mail.lycos.com. Looks like website was last updated 4 years ago. I tried to sign up got stuck at mobile verification. Didn’t bother to continue.

Other links that followed https://lycos.life, and some other news related pages of Lycos Ltd (Facebook, moneycontrol, economic times, etc.)

NOTHING RELATED TO ADVERTISING on front page of Google search.

Ummm… Maybe I should try googling from US. So I used VPN to Google “Lycos” from US. But the results were same.

Now I tried Lycos Advertising. I gives me a two page website called http://advertising.lycos.com. Now independently compare this website with the other website I have mentioned in point 1 to 5 above.

Judge yourself how much capable Lycos can be in advertising space which is the ONLY source of revenue for it.

Why do I say ONLY?

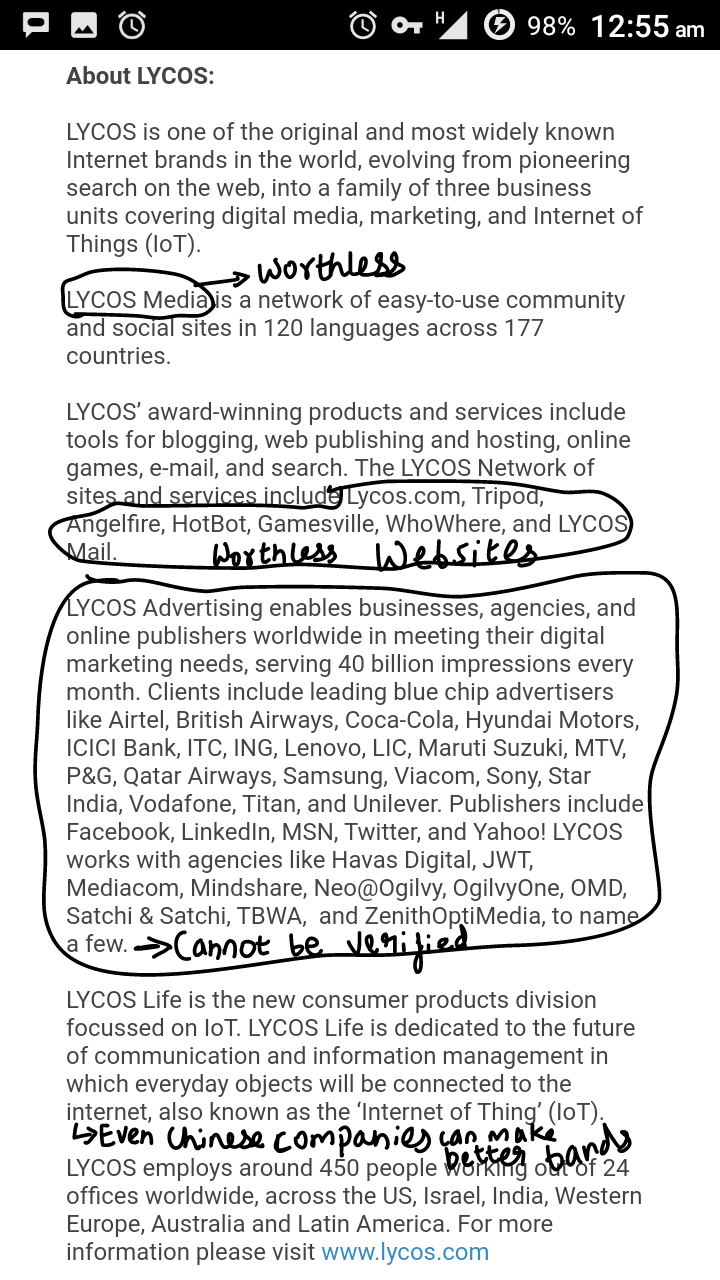

Just look at the image below on how lycos describes itself.

When I invested in this company and saw fitness band it introduced I tried really hard to believe it’s good. But reality is its ugly. It look like a watch for 5 year old kid which I would never ever wear. Even Chinese companies can make a better product without breaking a sweat.

Conclusion is except advertising Lycos doesn’t amount to much. And I have given my prima facie analysis of its advertising business.

@UtkarshP

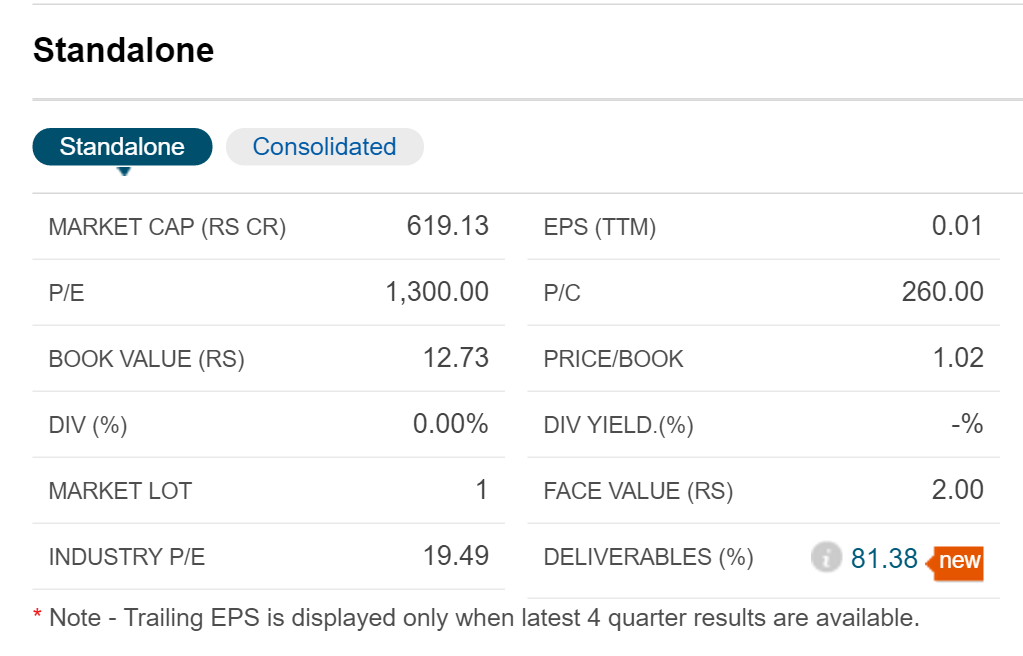

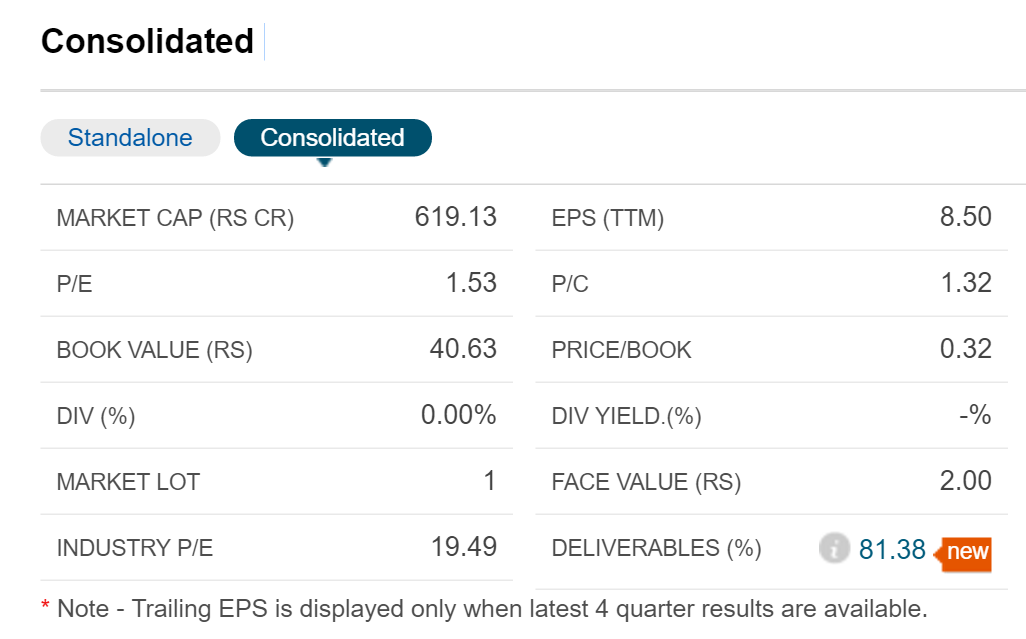

Of course Utkarsh, Lycos is not earning from its core business but its subsidiaries are doing great work. You can see the difference between its standalone and consolidated metrics.

In the above image from moneycontrol has PE equal to 1,300 and in the following image, it has a PE of 1.5. Price to book value is also showing a great difference.

The difference lies with standalone and consolidated values. Lycos have many subsidiaries so its income from its subsidiaries is very high. It has very less income from its core operation.

I get what you are saying about PE. But look at the decisions company has been taking all along. Take example of recent acquisition of mysms. At the time deal was announced, Lycos was paying 2.848 crore shares at around Rs. 30 (price on Feb 8th when deal was announced) that amounts to 70 Crore. Now go to Google play and install mysms. See if you are willing to use it even for a day. What mysms does is that enables you to reply to text messages on desktop. There is another app called Pushbullet. Not only it enables you to reply to text messages but you can also check notifications, whatsapp messages, share link, send file on your PC. Mysms doesn’t stand in front of it. But still this company goes and pays 70 Crores for it.

Also if you read this thread you’ll realize how reluctant management is in sharing financial statements of foreign subsidiaries. Good luck in geeting reply from their investor relations officer in any other matter whatsoever.

CEO talks about listing on NYSE. Short sellers there are going to have a good time ripping off balance sheet of this Co. Eros Media had to meet the same fate about a year ago when a single short seller brought down it’s stock price from 40 dollars to 6 dollars and thereby crashing price in Indian Market as well. Turn out he was right and EROS media was indeed overstating it’s income.

Another thing is that CEO doesn’t take any remuneration and says he is from a humble background on Concalls. How come he is buying shares worth Lacs from open market.

Company think Internet of things (IOT) is the next big thing. Guess what it’s not. Check out this article that days IOT is just a hype. http://m.huffpost.com/us/entry/9541326

The company is introducing a gamut of connected products aimed specifically at the living room. How good does it sound. If they are running out of areas to invest and pretty well established in their core area, why don’t they start distributing dividends a bit more generously.

CEO has never been short on making promises but when it comes to actually deliver, he has always fell short.

The trading volumes on NSE have jumped up since 27 July 2016. I do not find any information on bulk deals after 15 Sep 2015. Any body knows who are the big buyers and sellers ? Is there an operator who has become very

active?

Think smartly about lycos. Promoter are searching investor to facilitate exit of existing investor. Operator will not keep the price depressed for long time otherwise nobody will come to invest.

See the value of lycos.

Software division is valued at 800cr.

Patent are valuable and we don’t know the price - it may be 100 cr to 500cr also.

3)Business producing profit of 400cr per year.

IOT –developing business. Invested about 100cr or so. Loss of its does not produce much harm.

Now promoter has to convince the new investor about the value of company.

He will have to declare the asset of company also. New investor also confirm every thing about business including balance-sheet and other receivable.

Example see suzlon- When sanghavi enter price goes from 15 to 30. Company has huge debt.

Here lycos has only 85cr of debt that will paid in this year.

Looking this facts I invested in this company.

Dear Niraj…if u hv not already aware, then please check the RTA disclosure regulation 7 in nse shareholding information section…u will find that suresh reddy has been selling continuously since last few days along with some other promotors…it also states that he has also sold in june16…and he submitted to exchanges the shp with no decrease in promotors holding…

I am really shocked to see it happening…i believed the management is really genuine, but i was wrong…skr has to understand that he is not running a pvt company anymore…its public now…if this thing is true…then its a crime…why the wrong shp was submitted to exchanges??? And why promotors are selling??? They need to come in front and answer…

can you provide link for this matter. what i see is only one investor is selling . promoter is not sold any shares. see bse -disclosure sast and others.

It is mentioned as disposal…i suppose it means selling…though the performance of the company remains impressive…even today a news came out stating that they have entered into a partnership with Forensiq and Geoedge…