LIC HSG MD Siddhartha Mohanty on call with Moneycontrol categorically denied this piece of information.

1 Like

Management comments / concall takeaways

Collection efficiency: Collection efficiency for the month of Sep was 96%, around 3-

3.5% of loan book has enquired for restructuring. The restructuring enquiry in the

proportion of corporate and retail (by volume) is 2:1. Company expect this number to

trend down by Dec 2020.

Asset Quality: Stage 3 asset for individual non housing portfolio was 1.72% (1.74% in

June 2020), for Project loan stage 3 assets were 16.52%(vs 17.64% in June 2020)

Yield: Incremental yield is around 8.1%, for Individual loan incremental yield was

around 7.3%.

Refinancing: In 2HFY21 amount to be refinanced is c.165 bn average cost on these is

c.8.4-8.5%. Refinancing in FY22 will be Rs 250bn with a average cost of 8.1-8.2%

2 Likes

Today it touched 52 wk high, what is the event/noise around some merger being talked about?

LIC Housing Finance Q4FY21 Concall Update

()

Asset quality disappoints

Outlook: Neutral in near term; Positive in long term

• GNPA came at 4.1% vs QoQ 2.7%. Individual Housing GNPA is at 1.9%, LAP & Others 5.8% and Project 18% vs QoQ 16%.

• Absolute GNPAs were at 9559 Cr with Individual Housing at 3.5k cr, LAP & Others at 3k cr and Projects at 3k cr.

• Impact of second wave will be less than the first wave.

• NNPA came at 2.7% vs QoQ 1.3%. PCR was at 34% vs QoQ 50%. Historical average PCR has been at 50%.

• Stage 2+3 loans increased to 10.3% vs QoQ 9.6% & YoY 7.5%. We were expecting this to be stable but it has risen by 70 bps QoQ. (Historically Stage 2+3 was at 5.9% in FY19 and 4.6% in FY18)

• OTR 1 was given to 1.5% of loans and OTR 2 would be given to 1% of loans.

• Collection efficiency has remained at 98% in May as well.

• Co does not expect higher slippages going forward. However due to lower PCR, we expect credit cost to remain elevated in FY22.

• Loan Book came at Rs. 232003 Cr, +10% YoY.

• Individual loans +10% YoY, Project loans +12% YoY (Rs. 15956 Cr).

• Loan mix remained stable YoY with Retail Home Loans at 78% mix, Retail LAP & others at 15% mix and Project Loans at 7% mix.

• Disbursement came at Rs. 22362 Cr, +97% YoY.

• Individual disbursements +94% YoY at 21116 Cr, Project disbursements +190% YoY at Rs. 1197 Cr.

• Disbursal ticket size increased to Rs. 25.5 lacs vs YoY Rs. 24 lacs.

• Prepayment of loans was largely stable at 11% vs 10% YoY.

• Salaried mix continues to be at 87% and Self Employed at 13%.

• Co shall issue preferential allotment to parent LIC of 4.54 cr shares (~Rs 2300 cr at CMP)

2 Likes

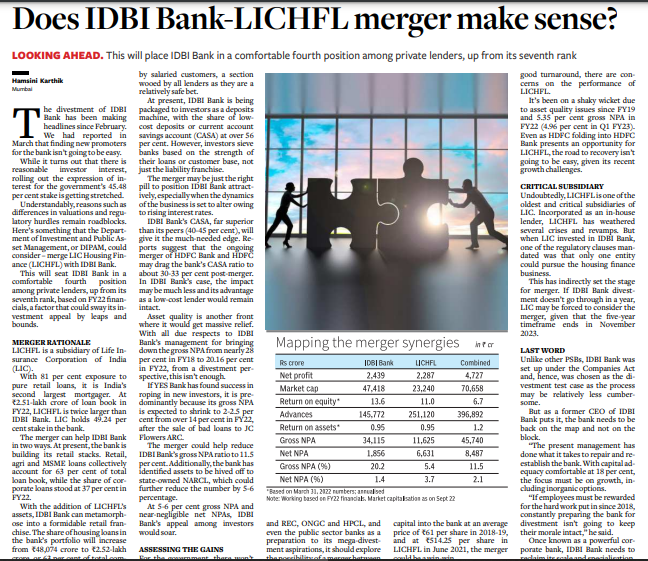

As far as I know, the government holds 45.48 percent in IDBI Bank while LIC holds 49.24 percent. LIC deciding to sell its stake in IDBI Bank was a coordinated move by the government.

Concall highlights

Key Q4FY21 Con-call Highlights:

-

As per the mgmt, majority of restructured a/c are performing and are in stage 1.

-

Collection efficiency improved to 98% in May. Mgmt has revalued the underlying stress for Covid impact and prudentially provided for it.

-

GNPA for developers loans rose to 18% in Q4 from 16% in Q3.

-

Break-up of GNPA includes:

-

Retail home loans: 1.89%

-

Retail non- core loans: 5.82%

-

Developers loans: 18%

-

Almost Rs14bn assets (5 big accounts) falling under Swami Fund seeking resolution. Swami Fund only a last mile funding option and doesn’t guarantee upgrades.

-

Stage 2 assets for retail loans stood at 4.9% as of Q4.

-

During Q4, 34% of individual home loan disbursement were towards affordable housing segment.

-

The company has repriced a large proportion of advances

-

Mgmt expects double digit credit growth in FY22

-

The company stated that the probability of further interest rate decline is less.

-

Rs250-280 bn of NCD will mature in FY22

-

The company raised Rs8 bn Tier 2 capital in Q4

-

The company’s board has approved fresh issue of 45.4mn equity shares to LIC (promoter) through preferential allotment. Post this, LIC’s stake shall increase to 45% from 40%.

1 Like

Some details about the Management, searched by me:

Executive Board Members of LIC Housing

(i) Mr. M. R. Kumar (Chairman)

Shri M.R. Kumar, took charge as Chairman LIC of India on 14th March, 2019. He joined LIC of India in 1983 as a Direct Recruit Officer. In a career spanning more than three and a half decades, he has the unique privilege of heading three Zones of LIC of India, viz, Southern Zone, North Central Zone and Northern Zone, headquartered at Chennai, Kanpur and Delhi respectively. He was also Regional Manager (Marketing) and Regional Manager (P&IR) at Kolkata and Chennai.

As an Executive Director, he headed the Personnel Department as well as the Pension and Group Insurance vertical of the Corporation. During his tenure, several initiatives were rolled out for the benefit of the employees.

His rich experience working pan-India, right from North to South and East to West including the heartland states of India while heading Kanpur Zone, has given him a deep insight into the demographics and insurance potential of the country. Moreover, working in different streams of life insurance management has given him the twin advantages of enriched knowledge and clarity on processes and procedures in the Life Insurance Industry.

(ii) Mr. Y Viswanatha Gowd (Managing Director and CEO)

Mr. Y. Viswanatha Gowd has assumed charge as Chief Executive Officer of LIC Housing Finance Limited with effect from 1st February 2021. He joined LIC of India as a direct recruit officer in 1988 and has risen through the ranks to this senior position. Prior to taking over as CEO of LIC Housing Finance, Mr. Gowd was appointed as Chief Operating Officer (COO) of LICHFL.

He also served as Regional Manager of LIC HFL’s South Eastern Region since 2017. Under his leadership South Eastern Region was the top performing Region of the Company and the loan book of the Region grew by 63%.

In a career spanning over three decades in LIC of India, Shri. Gowd has made his mark in the areas of Marketing, Finance, and Pension & Group schemes. He also holds the privilege of heading two divisions of LIC of India – Udipi and Dharwad as Senior Divisional Manager.

(iii) Mr. Vipin Anand (Non Executive Director & MD of LIC)

Vipin Anand assumed charge as Managing Director of LIC of India on 1 April, 2019. Prior to his appointment as Managing Director, he held the positions of Zonal Manager-In-Charge of LIC’s Western Zone, Mumbai and East Central Zone, Patna. Earlier, as Executive Director In-charge, he has been corporate head of LIC’s Direct Marketing, Corporate Communication and International Operations.

Mr. Anand joined the Life Insurance Corporation as Direct Recruit Officer of 12th Batch in 1983. During his service of more than 35 years with LIC, Shri Anand has handled with great success several important assignments in various capacities and departments, in operations as well as at the corporate level, ranging from Information Technology, Marketing and Personnel & Industrial Relations to Corporate Communications and International Operations, across different geographical locations of the country.

He was also a member of the IRDAI committee for framing Regulations on Digital Marketing and was a member of the CII Committee on Insurance and Pensions.

From high multiples in low mortgage penetration narrative(2014-2018) in hey days of trailing 2.5-3.3x P/B, over the years rising competitive intensity by banks & own asset quality issues have hit a good track record of delivering consistent profits/roe. While the arg of betting on banks reducing their competitive intensity is less uncertain, the tailwinds of better overall RE sales over next few years – growth in the end market via both volume & price, asset quality issues subsiding, better profitability (rising rates albeit a short term factor) when viewed vs current trailing vals makes this an attractive cyclical bet. Keeping aside vol growth, even mid single digit price rise in RE can help the growth no, prices have been broadly flat for past many years in general in tier 1 cities. In 2010-2014 era of very strong loan book growth, price rise too was a factor.

Housing finance has less profitability/roes given the yields, in general has merits in terms of being less risky, long duration, less cyclical.

Outcome is a little less uncertain, allocations accordingly, the payoffs can be really good if nos come through in next 2 years. Hfcs are very negatively viewed in recent times given banks have gone all out in capturing mortgage growth, raising the possibility that growth being shown now by hfcs is on account of more riskier customers than in the past. That could be the case in hindsight. Why bother then? trailing vals discount a lot of negatives & tailwinds help.

1QFY23: “Strength lies in reach. Will have share in the market. Then recently, we have also what you call equipped our the other line of officers. We call that the processing centers at some important centers for what happen now. Our digital operations, what we now engaged into there, also giving good results. So going forward, I think we’ll have a very good edge in the market as for the new disbursements are concerned. And growth for the current year, we are almost aiming at 12% to 15% in our disbursements. That’s one thing. Then as – given our existing book, the total portfolio also will be more or less moving in the same range of 12% to 15% by end of the year.”

1 negative is asset quality issues can further pop up spoiling nos for next 1-2 quarters. Not necessarily, management does not expect it, but it can be the case. Still unless it’s very material, given the growth outlook vs baked in valuations today, it’s worth a buy.

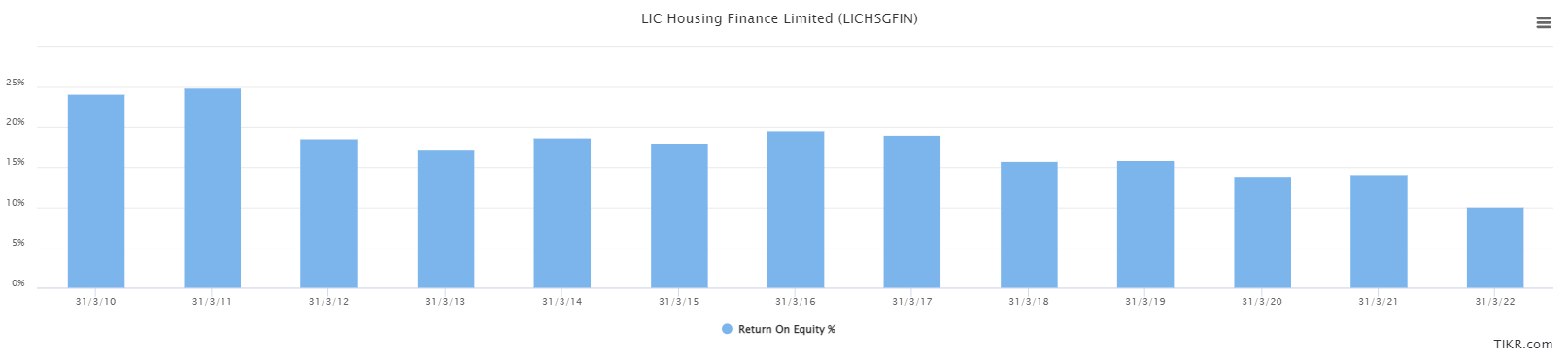

Over the past decade, roes have come off first from above 20%+ to 15%+ to about 10% in FY22. Better not to expect too much in terms of improvement, not going back to 16-18-20%, if we get double digit loan book growth, and roes head back to 13-14%, earnings growth & val rerating to say 1.5x can give 60-70% upside.

Disclosure: invested

3 Likes

After the 10% post earnings fall the stock is trading consistently below book value.

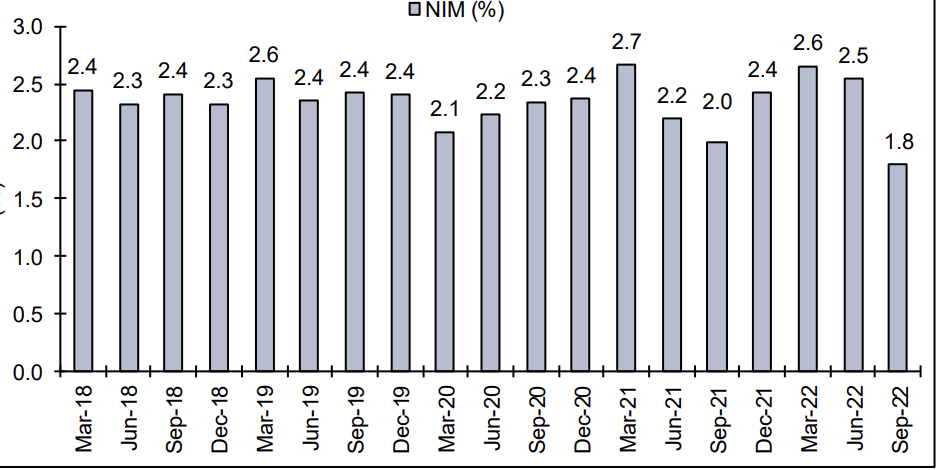

After going through a few brokerage reports (icici sec, hdfc sec, nirmalbhang ) the main concern is NIM volatility.

It is true that an nbfc will fair badly in a rising rate scenerio as the liabilities get repriced faster than the assets but that is more than factored into the prices, the company has seen high interest rate periods before has maintained its NIMs around the 2.2%

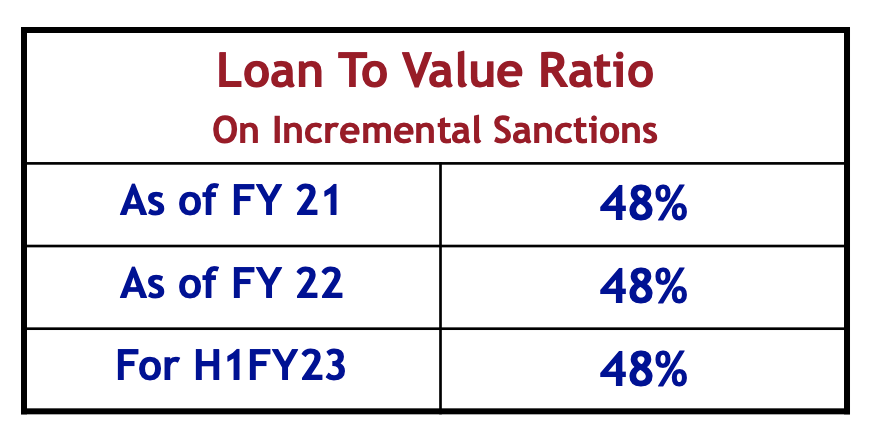

There is a risk that the 3500cr loans in OTR specific the project loans can slip in the next quater and that will keep credit costs high for the next two quarters but given that PCR is 44% and the LTV is 48% i feel they will be adequately covered from next FY with the possibility of lumpy recoveries at some point

Investment thesis is they will go back to 12% RoE in the next FY, and if you concider we are getting the equity at a 20% discount (0.8 PB) it is effectively 15%.

Assuming a 20% payout it is an attractive 3% dividend yield

the 80% that is reinvested if levered at 10x translates to a 10% profit growth

Seems reasonable

Disc: accumulating

3 Likes

Lic housing finance declared 1st qtr result today. A good set of numbers after long time. Figure should be compared YOY and not QOQ, as 4th qtr always distorts the picture. YoY income gone up by 30% and PAT gone up by 45%. EPS comes to 24, which would have been 30 but for impairment of financial instrument amounting to 360 cr. Management should come clean on this in tomorrow’s analyst meet. Last year this amount was 1900 cr. Imagine this on a equity of 110 cr. If this is sorted out, the share may fly and achieve its past glory.

NB- I am invested in this stock, so my view may be treated as biased.

4 Likes