If you sell your RE, you will get the current price in the market but then you will lose your “rights entitlement”. In short, if you sell RE, you will not be able to apply for rights shares. If you don’t sell your REs, you can apply for more quantity. If so, you will surely get rights shares equal to your RE quantity, but will get more shares only if rights issue gets under subscribed.

1 Like

Similar situation as OP asked on rights shares in my demat; Got an email from linkentime to pay which I did @55 Rs/share and got an acknowledgement too for payment. Should I fill up the application form too? The form part confuses me as my DP ID and pancard should be enough for them. I wrote them an email 2 days back and havent received a response

If you made online payment on linkintime, your application is complete. No need for separate application

Brilliant; thank you very much.

For others who received rights issue email from linkintime, follow the link they sent in the email and first check your allotment. you will need your DP and pan card details. After that, on the same page confusingly they have a pay and download option. Choose pay and follow the 3 step part to verify, add bank details and finally pay by UPI. Use the same a/c that is linked to your demat/trading acct. So you need your acct nbr,IFSC code as usual.

The form doesnt seem to work for me in IE, so if you get strange or blank dropdown options switch to FFox.

HTH

what you have got is the rights issue entitlement. some people may sell it in the market to raise cash. It will disappear from your demat account next week. Rights issue gives you the right to apply for additional shares at a discounted price. Market price of L&T Finance Holdings is Rs 90 per share and you can get specified number of shares as per your entitlement at Rs 65. You can also apply for additional shares at the discounted price.

disclosure: holding and applied for rights

I have applied for right entitled shares. Now can I also apply for additional right issue shares? If I not get allotment how the money will be returned. I’m applying from link intime. Pls advise

1 Like

Hi All can anyone comment on the MF business sale to HSBC?

I am also interested in learning more about it. Why does the market took it so wrong crashing the share price by 7%?

Started building a thesis around L&T Finance since yesterday after I came across a Hindu Businessline article, sharing observation so far.

Source of information: Management Interviews, Q2/Q3 FY22 earnings calls, Mar 21 Annual report, Google Search (news articles, etc.)

Management

- Prudence - One could feel that based on Q3 FY 22 call. Listen to more calls

- [July 2021] Following analytics based collections approach and collection led disbursement strategy

- Back in Jan 2020 (Pre-Pandemic), Dinanath Dubashi: We are lending only to the best of the best in real estate now and it is a good opportunity to enter into the A plus plus category

- Walk the talk - Do they actually do as promised? Find out from past management interviews in news channel / Valuepickr.

- During Q3FY22, at several instances talks about feedbacks - feedbacks around:

- Length of explanation provided during the call

- more disclosure in investor presentation (for this particularly, he didn’t want to start a new trend durning Covid and wants to wait before new disclosures are started),

- real estate portfolio performance / asset quality, and its impact on valuation

- Management accepts mistakes (humility), e.g. mistake to lend to select instances of real estate loans

- Shareholder friendly (sounds so from the call)

- Talks a lot about digital journey, data analytics, data engine - dig deeper here.

-

Mar 2022 - Among the market leaders in farm equipment finance, two-wheeler finance, as well as micro loans and continues to be one of the leading players in financing infrastructure sectors like renewables and roads. Furthermore, it has taken strides in building a comprehensive home loans business and launched its first-ever digital native consumer loans business

- Shows that in some cases they have proven their ability to transform business (e.g. home loans business)

- Change of chairman - Mar 2022

- Shailesh Haribhakti being replaced by S N Subrahmanyan

- Documents show list of commitments for Shailesh, he’s too busy a man and has tons of directorships

- S N Subrahmanyan on the other hand is a hardcore L & T er, dedicated to business for much longer time and doesn’t have too many outside directorships

Sale of L&T Investment Management (LTIM) to HSBC

- 425 Million is the quoted price

- In addition, regulatory capital requirements in the business are in double digit crores (assume max of 99 crores) and the business has over 700 crores in cash & equiv.

- The cash is also accumulating at 50 crores per quarter.

- Assuming the sale goes through in 3rd quarter of CY22, 50 Cr x 3 = 150 crores

- And the additional cash (besides max of 99 crores) comes to 600 crores (at the least)

- So total extra cash = 150 + 600 = 750 Crores

- Add in 425 Million of quoted price = 31659.52 Millions = 3165.952 Crores

- Hence total consideration is around (in INR) 3165.952 + 750 = 3915 Crores

- This is roughly 25% of current valuation.

- Hence we are getting the business at 11955 Crores, the business except for LTIM

- Now try to work out if the remaining business deserves 11955 Crores of valuation

- Investment management business, in Q3FY22 generated profits of 51 Crores, assuming annualised at (51x4) = 204 Crores, the valuation of 3200 crores indicates 16 times PAT or 3200/(65*4) = 12.3x PBT.

- The valuation could have been better. This shows that previously, they had failed to sell Mutual fund business and hence this time, they are not over pushing in valuation, instead accepting a lower valuation then what market is currently otherwise assigning to well managed AMCs (HDFC AMC)

- For reference, the ongoing IDFC MF sale is fetching upwards of 4000 crore for profits of 144 crores in FY20-21. That’s almost 28x earnings.

- Business has contingent liabilities of 1900 crores, so, from market cap:

- Subtract 3915.952 crores (expected value for selling LTIM)

- Add in 1900 Crores (Contingent Liabilities)

Infra Disbursements

Renewables

- Largest renewables financier in India - Search for economic times article on Google, had seen this sometime back in the past.

Problems

Disbursements

- Lot of disbursements are subjected to approvals (NHAI, etc.) as a result disbursements get postponed

- Number of disbursements that have postponed actually give hope that Q4 will be better than Q3 (This is just QSQT - focus on longer term trend)

- Number of projects where approval is in hand is actually quite robust, more than it ever was in last 6-7 quarters

- Again gives hope that following quarters will be much better

Prepayments

- Competition giving very low rates, assets moving out

- International markets for bonds, etc. being used and many companies running unhedged borrowings and believing cost of funds is much lower.

- Mgmt believes there is unsteadiness in the exchange rate - this has happened in the past too, has worked for 30 years in industry. People believe low cost dollar funds come for free and the cycle shows that it is never true.

- When exchange volatility hits, truth comes out.

- ⅓ rd of prepayments were due to bonds

- Now that the company is also getting cheaper funds, the company will also try to retain. Hence company believes rapid fall in infra portfolio will be arrested

Consumer Loans

- Launched 2 years back

- Used the existing database of home loan customers, two wheeler customers and asset management company investors to predict needs, credit behaviour of these people

- Average ticket size: 1.5 lacs completely to existing customers

- Now starting to enter external database, trying to look at lookalikes of our existing customers

- NO COLD CALLS at all. Useless / not cost effective.

- As a result of this approach, the portfolio is close to 2 years old with collection efficiency at 99%. Worked very well.

- Clearly this will have limitations

- As of now it’s only urban, not yet gone to rural / farmers. There are other products for farmers / rural customers. Won’t offer them personal loans on the phone - not yet at least.

- Urban products

- Home loans, consumer loans, two wheelers, more importantly: looking at extending this expertise of consumer loans to ecosystems, to lending to a customer but where money is paid to the final vendor - e.g. coaching class, physical as well as online.

- These are not the education loans for basic education, these are for value added education

- Its a great place, good opportunity exists. Done a detailed product / market, segmentation analysis. That product will be launched early next FY (Next FY starts April 2022)

- Healthcare / Hospitalisation

- Country is extremely underinsured as far as healthcare is concerned, people only try to reach the 80D deduction level.

- These loans are given to the relatives, not to the person who’s hospitalised or to students.

- These are not student loans, instead they are given to parents (for education loans - Akash Institute, Byju’s, etc.)

- These are two immediate offerings. There will be more offerings

- Home loans, consumer loans, two wheelers, more importantly: looking at extending this expertise of consumer loans to ecosystems, to lending to a customer but where money is paid to the final vendor - e.g. coaching class, physical as well as online.

- Rural products

- Right now looking at refinancing on the existing assets

- As we study farmers more and more, we will tie up with ecosystems in rural

- Fertiliser ecosystem

- Dairy ecosystem

- Seeds ecosystem

- Post harvest ecosystem

- Warehousing ecosystem

- These we will do for our farmers and their lookalikes around to increase customer care

- This is where the farmer finance as separate from tractor finance is going to grow.

- Consumer / Rural Products - Yields - 12% to 16%

- Median income of customers - To be explained by Anuj later during the call.

- We don’t do consumer loans to rural (tractor/mfi). At this point of point it’s a completely urban product (i.e. home loan, LAP, two wheelers)

Real Estate

- At this point of time, we are very concentrated on making portfolio performance good.

- Management wants to demonstrate that other than a few select instances, the real estate portfolio is good and management can deal with the portfolio.

- Show substantial reduction in real estate portfolio in next 12 months max and then re think the real estate strategy

- At this point in time, we are not putting forward with any amount of aggression over real estate portfolio

- While arithmetically growth will reduce because of this, we were talking about overhang in real estate (not about growth) not too long back. We will first concentrate on taking away this overhang and showing that we have good portfolio

- Almost 25% of the portfolio has been collected and reduced in last 1 year, will continue with the trend for a year more.

Overall growth

-

From 50%, retail will increase substantially. Why? Because we are quite clear that infra disbursement fees we would like to increase but how much we will give capital, will depend on other things

-

Target is retail growth, not overall book growth. (reminds of IDFC First? Keep book steady but move to retail upto a certain portion)

-

Infra business can be well run if we put underwriting, disbursement and profitability with fees as the metric rather than book as the metric.

-

In tractor / two wheeler - market share is already very high, here the growth will be largely in line with industry growth. The company will be marginally better in growth than the industry but not substantially better

- Currently, these industries growth potential is negative and may be will remain negative for a year or so, but rural fundamentals strong, hence quite confident, just from existing rural products, growth of mid teens to high teens is possible. - This is as far as existing products are concerned

-

Now, customers of existing products are used, to cross sell other products. (similar to what many other banks / nbfc including the likes of Bajaj Finance do)

-

New products: Consumer loans, SME, Farmer Finance, calculations are being done. When a number like 25% CAGR is being committed, management has done strong homework on this and is confident that this will be built - one on top of each other.

-

Overall growth approach: Existing product - Growth slightly better than industry > New markets for the existing products > Selling more to customers of existing products > New products altogether

March 2022 - Exiting Wholesale / Real Estate Lending

- Vision 2026

- Current retail portion is 50% of overall loan book of around 1 trillion (1 lakh crores)

- Looking it double it in next 4 years

- Portfolio will shrink first as it exists wholesale and real estate exposures and then scale up size

Total stock of provisions: 4600 crores (480 on standard, 24 on NPA, 1700 Macro + restructure + GS3)

Arbitrage Opportunity

Feels like a strong arbitrage opportunity at the very least. Why?

- At 15x trailing PE and 0.8x book, market has already priced it as a mediocre Infra / Real Estate NBFC while the business is clearly focused on transforming itself in data driven manner to be a retail focused NBFC with results on its side.

- Even if business doesn’t transform and is doomed to stay as it is, considering 5.5% GNPA at D/E of 4.4x, even if entire GNPA pool is poof / gone in dust, that’s a 24% hit to book value, company is already trading at 20% discount to book value.

- The consideration expected for LTIM seems to have been overlooked in details

- A recent article - L&T Finance’s retail-only strategy could be tricky, time-consuming - The Hindu BusinessLine shares outlook of Axis Capital, compares the attempted transformation by management with that of Chola or Baj Finance and calls it tricky / time consuming - so what? Brokerages might be interested in QSQT or YSYT (Year se year tak), but as individual investors, as long as management’s focus in at par, management is honest, and the growth trajectory is realistic (law of large numbers, etc.) we can wait it out and take benefit of this buying opportunity.

- This shows that Mr. Market hates uncertainty and often perceives uncertainty as risk.

- For valuation: I would have preferred it even cheaper, for better margin of safety.

- This is a bet on management. There is news about changing Chairman, S N Subrahmanyan, MD/CEO of L&T taking over as chairman. If you read history since he took over as CEO of L&T, largely the business (and its profitability) has remained on its past trajectory.

- However, if for some reason, Dinanath Dubhashi decides to move on, there’s probably time to move out until we know that the next management is as capable if not more, as the existing one - but that’s a key person risk, to be kept at the back of mind.

—

An Additional point on valuation

- THIS IS SHORT-TERMISM AT PLAY. DON’T PAY HEAVY ATTENTION TO THIS AS LONG AS REST OF THE THESIS IS SOLID.

- CITIGROUP GLOBAL MARKETS MAURITIUS PRIVATE LIMITED exited their huge holding (~2.5% of company’s total outstanding shares). That literally increased the free float in a huge manner. And this happened right on the day of Russia invading Ukraine when markets tumbled in a big way (hence macro driven).

- Stock tumbled 11% just with that one transaction

- Besides above, don’t see any major reason for sudden major downfall.

Reverse DCF

- Considering lowest CAGR in profit of last 10 years, the business has grown at at least 12% profits per annum

- This indicates, average PAT of 1900 crores and min PAT of 1090 crores in year ending Mar 2022 (Worked it out in a private doc - not for public access yet)

- At least multiple of 5x earnings

- At 1900 Crores, required growth at 15.20% for investment to grow at CAGR of 26% per year

- At 1090 crores in Mar 2022, required growth at 25.50% per annum for investment to grow at CAGR of 26%

- In either case, this doesn’t seem like a daunting task for a NBFC that has been moving towards fintech / data driven retaliation, being run prudently, had controlled cost of borrowing during the toughest of times (CoVid 1.0 / 2.0), and is committing towards 25% CAGR in its public statements.

- Ultimately, even if we miss by a few percentage points, a growth at 20% CAGR is not bad either.

Liability Profile

- Whether or not it is rich in NCDs and other low cost borrowings?

-

[Jan 2020 - Pre pandemic] On the debt side, there has always been highly rated companies with good parentage. This quarter, we are seeing that distinction becoming extremely pronounced and L&T Finance as well as some of our highly rated peers are getting money much more easily. Just to give you numbers, we have raised long-term funds from various sources – both private and public NCDs, ECBs etc – up to Rs 10,000 crore this quarter. Our total CP percentage has come down to single digits. That has happened while redu …

- YoY, back then, borrowing cost was reduced from 8.61 to 8.54

- Currently, March 2022, cost of borrowing 7.47% - See presentation for Q3FY22 page 5.

- Retail NCD / NCD Pvt - form 51% of overall borrowings, Bank Loans at 36% See presentation for Q3FY22 page 15.

Disclosure: tracking, not holding.

3 Likes

Q4 result. Appears average.

Source: Company Q4 presentation

Source: Company Q4 presentation

While going through FY 22 Q4 the following points are noted:

-

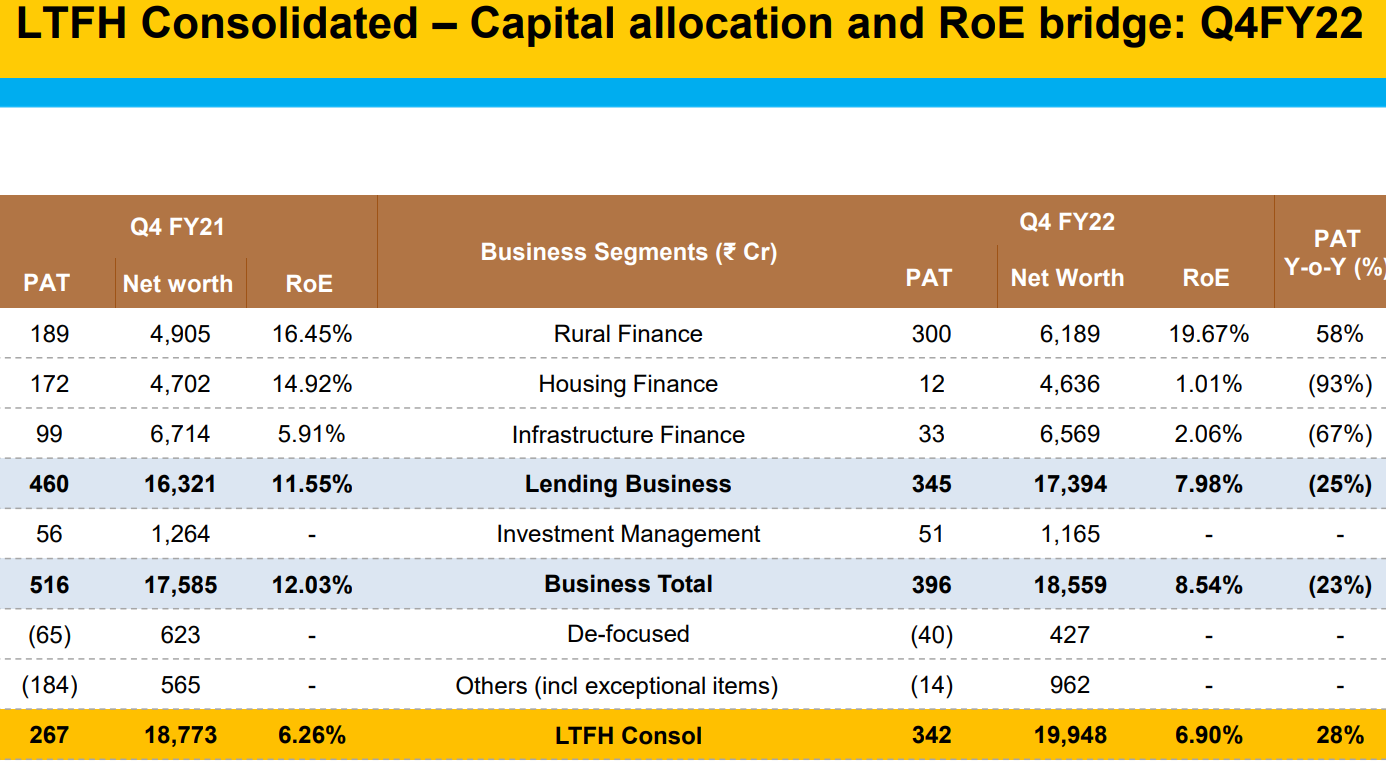

Reduction in overall GS3 from 5.91% in Q3 to 3.80% in Q4FY22, which is commendable. Total RoE is 6.90%.

-

Q4 FY 22 PAT is 342 Cr against Rs. 307 Cr of Q3 Fy 22.Interest income in Q4 FY 22 is Rs. 2918 Cr against Rs. 2875 Cr in Q3 FY22, while Rs. 3223 in Q3 FY21. Basically, PAT is optically high due to low provisions and low tax ( in comparisions to YoY Q4). The interest income which shows business growth remains stagnant.

-

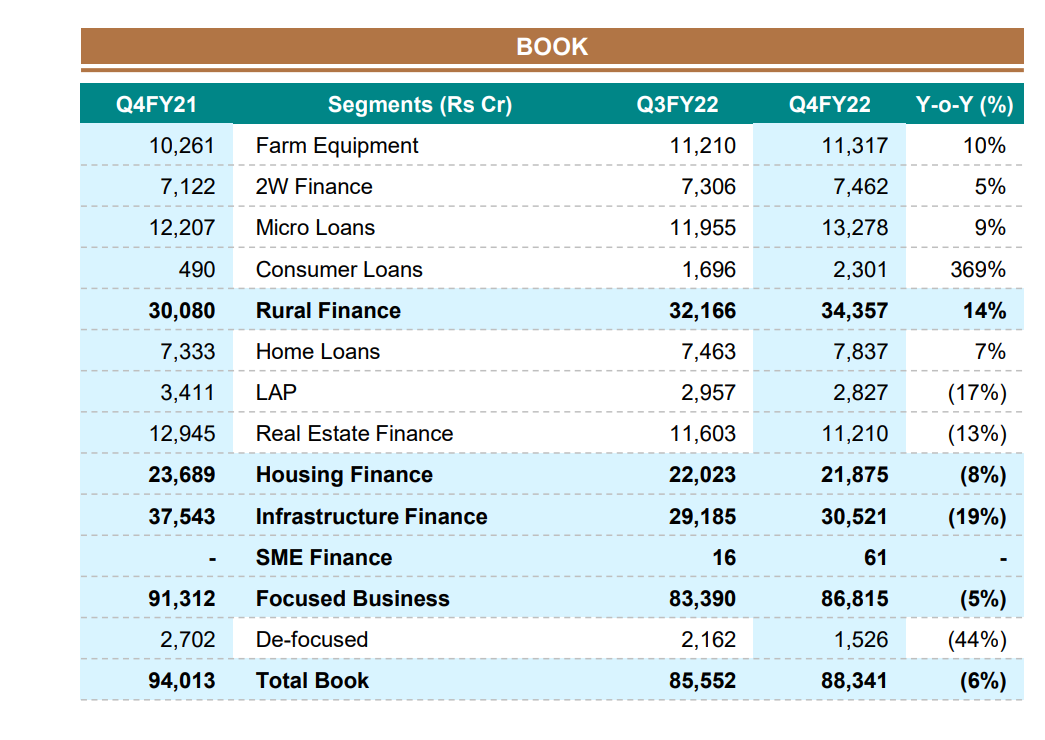

Rural Finance is their growth engine going forward. Overall NIM+ fee is 7.17 % in this quarter, but for rural finance NIM+ fee is in excess of 12%, while for housing it is 4.4%. So, out of 88342 Cr. total book, the high yield and high RoE book ( ROE for rural finance is 19.67%) is only 34357 Cr. ( increase 14% QoQ). Rural GS3 is 3.97%, which appears on higher side.

-

As per company presentation although 51% book is retail book, but only 39% ( rural finance) is bread and butter and carrying load of low NIM + low RoE of other verticals. Even housing retail is having NIM 4.4%, which may be due to approx 10-11% home loan rate due to higher competition and 7.34% fund cost to the company.

-

Even infrastructure finance is very low NIM and low RoE business ( 3.31% NIM + fee, RoE 2.06%), while book size is approx. 35% of total book and increased in last quarter. Managment should be asked reason for increasing exposure in con-call , when margin in these businesses is even less than bank FD.

-

Liabilitiy Frenchise continue to be strong and adequate provision are there. Long term ratings are AAA.

Overall average set of numbers and key will be to expand rural portfolio and reducing other portfolios.

Disclosure: Invested and no transaction in last 30 days.

2 Likes

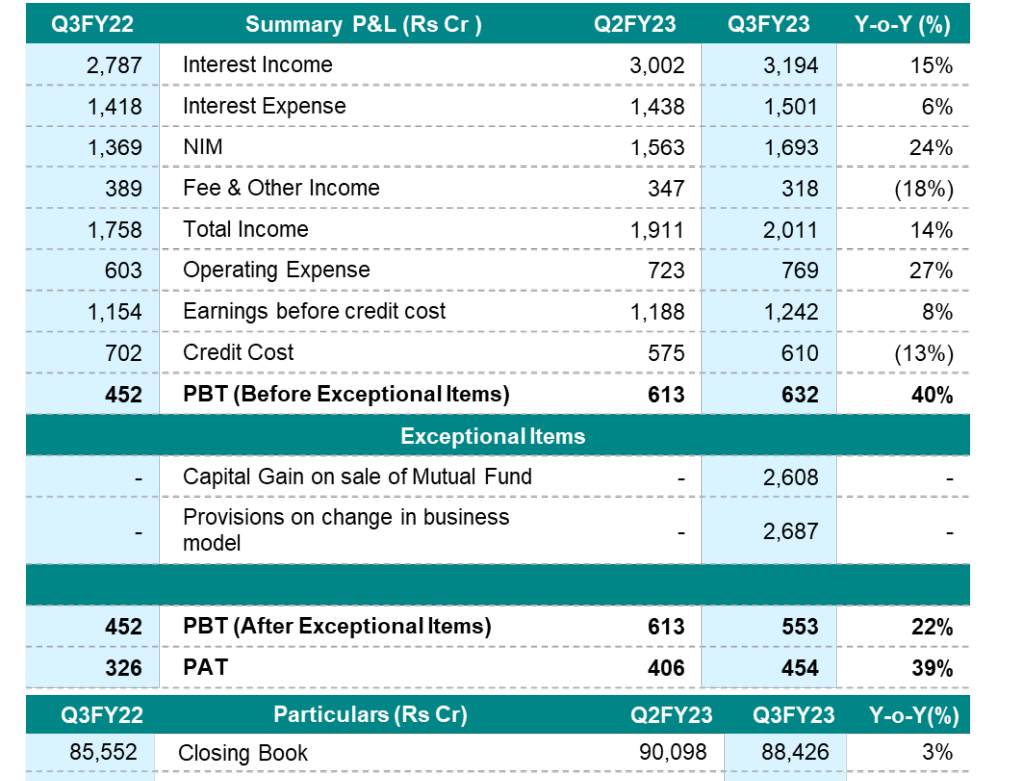

Q3 FY23 Result

Source : investor presentation

1.Management has mentioned that they have provisioned Rs. 2687 Cr. as one time provision for acclerated sale down of wholesale book and at the same time they have shown capital gain of Rs. 2608 Cr. from sale of Mutual Fund business to HSBC. Perhaps management is cleaning NPA mess in tax efficient manner. These provisions are substantial and management owes a detailed clarification to shareholders, how this mess was created and kept pending and whether any specific drive ( like Lakshya 26 etc.) is required to reflect the NPAs. Still wholesale book is Rs. 31010 Cr ( down from Rs. 37597 Cr. QoQ), so don’t know whether more provisions are left.

-

One thing is clear that management is aggressively taking steps towards retailization of loan book ( retail book from 52040 Cr to 57000Cr QoQ) and NIM+Fee +other income is 11.38% for retail, compared to 8.88% of total book. It is only 3.74% for whole sale book. It means whole sale book is a big drag on over all profitability.

-

Performance of this quarter in term of disbursement, NIM, RoE is better in comparisopn to YoY and QoQ.

-

Consolidated GS3 is 4.21% ( NS3 1.72%, PCR-60%), while retail GS3 is 3.47% ( NS3- 0.73%, PCR- 79%). Still a lot more room for asset quality to improve. since, cost of fund is 7.54%(in comparison with 3-5% of banks), and NIM is 8.8% ( 11.38% for retail), it means their interest cost is quite high, so borrower profile may be risky. Management in their Lakshya 26 target also envisages GS3 <3 %.

-

Overall forward looking results with clear direction.

Disclosure: Invested and no transaction in last 90 days

7 Likes

What does the community think about the company results?

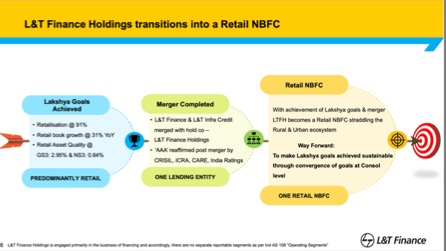

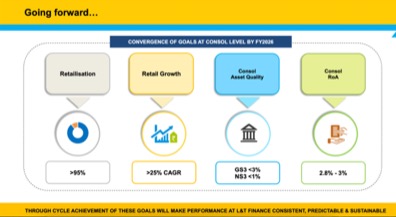

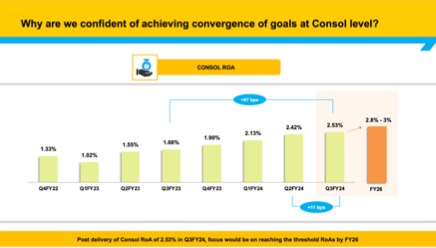

What I like - Company is doing what they are saying. Very good ramp up of retail loans, now at 91%. They consolidated the subsidiaries and will report at consol level going forward. They have proven the retail model, achieved all their 2026 goals, 2 year in advance. They will easily achieve consolidated ROA of 2.8-3, now at 2.53.

CEO change was very well managed.

What I am worried about - Unsecured loans form 45-50%, they are managing risk well but credit cost hovers around 2.5%.

I don’t fully mathematically understand the high credit cost but low NS3. Restructured book plays a part.

I am trying to calculate their book value and estimate the future book balue. Net worth is given but with ramp down of wholesale book, restructured loans still underway, I am wondering how to do it. Appreciate any thoughts.

P.s. Invested and biased.

3 Likes

L&T FH delivered another great set of numbers this quarter, whilst Lakshya 2026 goals have been met 2 years in advance.

-

Consol ROA is now at 2.53% vs 1.66% Q3 last year, consol ROE is now 11.35%

-

Consol PAT is up 41% YOY at ~640 Cr for Q3

-

Merger is completed with L&T AMC sold off and L&T Infra and L&T Finance now merged into this company

-

Retail book grew at 31% YOY and is now > 90% of the business. I think this is now largely a retail NBFC and with only a small part of the wholesale book to sell post bringing it down so sharply, do not understand with these growth/ROA metrics why is it still valued at under 2 PB when the likes of Chola, FiveStar are trading much higher (>4 PB).

-

Even in pre covid times (Jan 2020) when things were terrible for NBFCs after 2018 and this was not a retail NBFC this has traded at 2x book. Whilst in great times in 2018 with the credit cycle, valuations were much higher than that as well when it traded at 5x book

-

Management has addressed doubts on personal loans/contracting NIMs well in the concall and have mentioned not much impact, but this remains to be seen in future results

-

CEO transition handled quite well and old/new CEO were both on the last concall with lots of positivity. Current CEO Mr Sudipta Roy is ex ICICI/Citi/Deutsche bank and ex CEO Mr Dubhashi superannuates from the company in April’24

-

Below snapshots from Q3 investor presentation sum up last years progress quite well

- Charts also look good in my opinion with clear respect for 50 DMA on the way up and comfortably having broken through a couple of key resistances and upward trendlines

Disclosure : I am invested in self and family accounts for the last 1 year odd and am biased. Have further buy transactions in family accounts in last 90 days. I am not a SEBI registered advisor and this is not investment advice.

4 Likes