Sharing Credit rating agency report on Kriti Industries! It gives very good insights about the company and its Q1 Fy 18 performance. Kriti Industries (India) Limited-10-05-2017.pdf (396.0 KB)

2 Likes

@rathiraunak71 A very useful report indeed. More so because there is otherwise a dearth of info on the developments in the Co. The report gives the reasons for the pressure on margins in the June qtr. In fact, 17-18 should show substantial growth over 15-16 as well, assuming that 16-17 was a one off bad year, but we will know better when the results for Q2 are declared.

1 Like

What happened here… company reporting loss.

The loss is on account of reduction in loan burden by early repayment of Loan. However there are pressures on margin as well. One thing which i cannot understand is that the receivable are on 45 crores as against payable which are Rs 98 crores. It might be due to Inventory accumulation and lack of Demand pressure on company leading to compiling of stock. If the same situation continues they cannot even meet out there guidance of crossing 464 crore mark. As of now i have exited my position from stock booked a loss of Rs 6 per share and shifted my position to new company Medicamen Biotech.

I also exited my position fully today with no profit or loss.

WE MUST STICK ON BASIC FORMULA OF INVESTING i.e QUALITY OF BUSINESS, LONGEVITY, GROWTH AND REASONABLE PRICE. THE COMPANY HAS FAILED ON GRWTH ASPECT CONSISTENTLY EITHER DUE TO DEMONETISATION OR ON ACCOUNT OF GST OR IN Q2 NUMBERS.

FROM QUALITY, LONGEVITY AND REASONABLE PRICE ASPECT THE COMPANY IS HIGHLY UNDER VALUED. BUT MARKET IS SUPREME AND IS ALWAYS RIGHT AS PER RULES OF MARKET.

Result Announcement -

revenue growth was encouraging but why has the cost of materials consumed gone up by around 43%.

any insights would be helpful

Madhya Pradesh govt. is providing huge subsidy (around 35-40%) on farm pipeline and on sprinkler set.

Kasta Brand is very known, famous and reliable among farmers in Malwa region of madhya pradesh.

Kasta HDPE pipe and other kasta products are in huge demand and preferable.

Other competitor in that region is Texmo pipe.

Farmers demands Kasta products though they are costlier than Texmo.

2 Likes

Interestingly, there has been no post for the last 2 years. I recently started evaluating this company and see a few indicators of the company trying to scale up to higher levels. From the publicly available information-

- They have engaged a consultancy (levers4change) about 2 years back to look at sales growth strategy, Operational tracking , corporate communication etc. and seem to be diligently implementing their plans

- For a company of their size, their annual report is quite impressive and highlights the marketing strategies, entry plans into new states, focus on financials etc.

- They have just announced their first ever investor conference

- They have been steadily improving sales, margins, RoE figures over the last few years

There are no obvious alarms in terms of debt, pledge, low promoter stake etc.

Considering that it is the cheapest available pipes company and seems to be at the right size and in the process of transformation, this may be a value investment right when the economy appears to be turning around.

Discl: Invested at around 60 recently

2 Likes

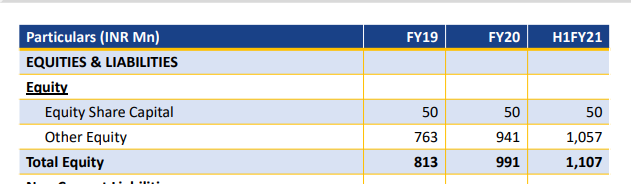

Other equity is increasing every year. Should the investor be worried about the other equity?

This is Reserves. It is natural and healthy for it to increase year on year. It is a cash generating , dividend paying co which has reduced debt recently

hi, does anyone hv an update on the co? am thinking of investing a little

Since it is a low profile regional player, information is a little difficult to come by. But you can listen to their Q4 concall (first time they have organized one) to get a feel of their strategy and management. They are targeting doubling of revenues to 1200 Cr by 2023. While this sounds aggressive, the tone of management in the call overall sounded conservative and grounded wrt to capital/funds deployment.

2 Likes

Q3FY22 - Concall Notes

65% market share in MP, 45% in RJ, 10% in MH

Retail sales 75% of revenues

9MYTD - Revenue 385cr (18% down yoy), EBITDA 35.7cr (33% down yoy), Margin 9% (11% yoy)

Q3 - Revenue 119cr (46% down yoy), EBITDA 9.8cr (66% down yoy), Margin 8.2% (13% yoy)

PVC prices came down from Rs160/kg to Rs130/kg within the qtr

Revenues dented by volatility in PVC prices and rains in MP and RJ - Building, microirrigation and industrial solutions have shown marginal improvement

Capex - 30cr for new capacities and new product range - commercialize in Q1FY23 - for building and submersible - 18months full utilisation - 150cr sales with value add margins up

Full range of product in Building and column pipes - intent to grow due to noncyclicality of demand

Expand sales in new entrant markets

Agricultural products - Volume 75% share, 5.7kT (2% up qoq, -56% down yoy) - Revenue 75%share, 89.3cr (12%up qoq, 52% down yoy) - 76% EBITDA share -Margin 8.3% (11.4% qoq, 13% yoy) - rainfall destroyed market for pipes - also high PV price deterrent - one of the worst qtrs in terms of demand - green shoots showing up

Industrial Solutions - Volume 16% share, 1.2kT (-14% down qoq, -56% down yoy) - Revenue 14% share, 16.5cr (-9%down qoq, -40% down yoy) - 16% EBITDA share 16% - Margin 10% (9.5% qoq, 13.8% yoy) - maintain guarded approach because of working capital cycles and no interest to match low prices of unorganized sector

Building products - Volume 9% share, 563T (-30% up qoq, -2% down yoy) - Revenue 10% share, 11.6cr (-16%up qoq, 35% up yoy) - EBITDA share 10% - Margin 6.4% (12% qoq, 11.7% yoy) - Full equipments and moulds will be commissioned from Q1FY23 - will pickup following that - good response generally - readying distribution network by time of commission - hired sales people - incomplete set of products was hampering growth

Inventory came down significantly - still scope of lowering

Sales is southern states didn’t fall much because of rainfall distribution - appointed 25-30 dealers in KA, GJ, TL but continuos demand for 2-3 months makes dealers active - more dealers by March - 400 dealers earlier in legacy states

Agriculture margins suffer because Q1 and Q3 are good and rest less demand - bring down margins - market share improved in legacy states

Augmenting CPVC moulding and extrusion capacities - as part of building product initiative - sorting out RM supply side

Cost of debt - working capital 7.5% and letter of credit 4.5%

Guidance - 1200cr by FY24 - mgt will qualify statement in next qtr

2 Likes

Any updates on this company, how is the performance expected to be in the coming quarters.

Few interesting pointers on the business:

-

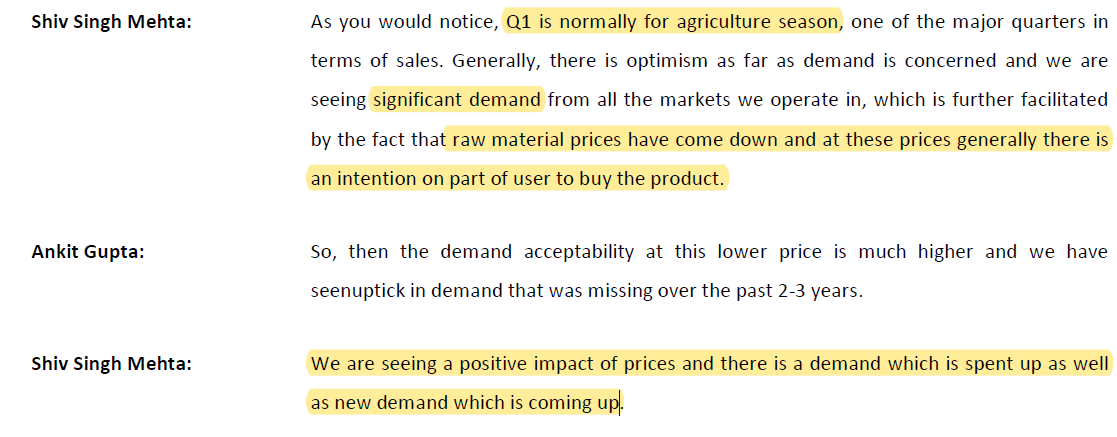

PVC cycles seems to be bottomed out: Guiding of better margins than previous quarter (around 10%) but as they are expanding there can be some pressure too. Hence, no major upside surprises.

-

Next quarter Agriculture season (of their best): 70% business is from agri and they are capping the industrial product line (low margin business) hence, margins should be fine.

-

Charts have started to improve.

But management is going slow for some time and waiting to stabilize and guiding for 10%+ growth only:

Chart:

2 Likes

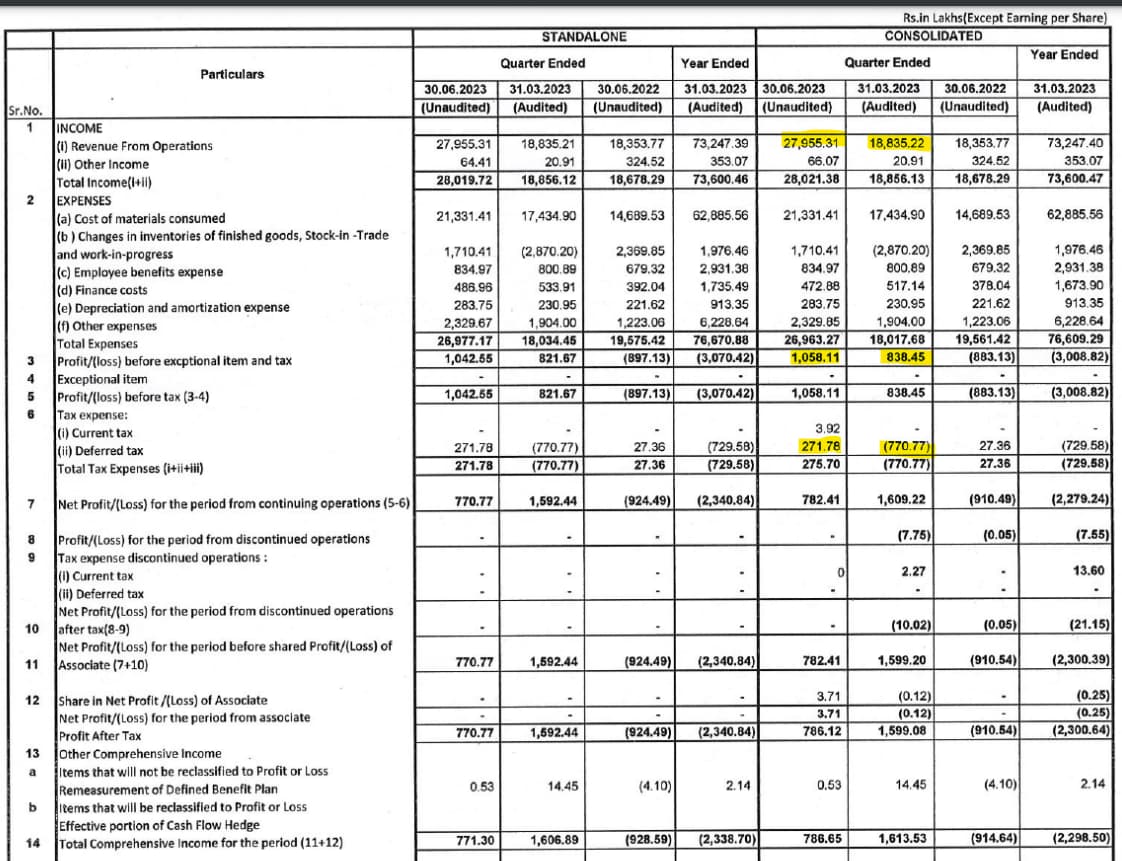

Results for Kriti Industries are out and as we see the stock is down by 17% during Monday opening.

But I think the business has actually performed well, it is the tax liability which is providing us negative view.

Revenues have grown at 48% QoQ

Profits grown at 26% QoQ

But as there was some deferred tax liability in last quarter the numbers were high. The same was not true for this quarter which brought down the number.

Tomorrow 3pm is the concall (invite), let’s see what the management has to say about the same.

If someone is tracking this business for longer timeframe could you please share some details on this tax framework?

Disclosure: Not Invested.

3 Likes

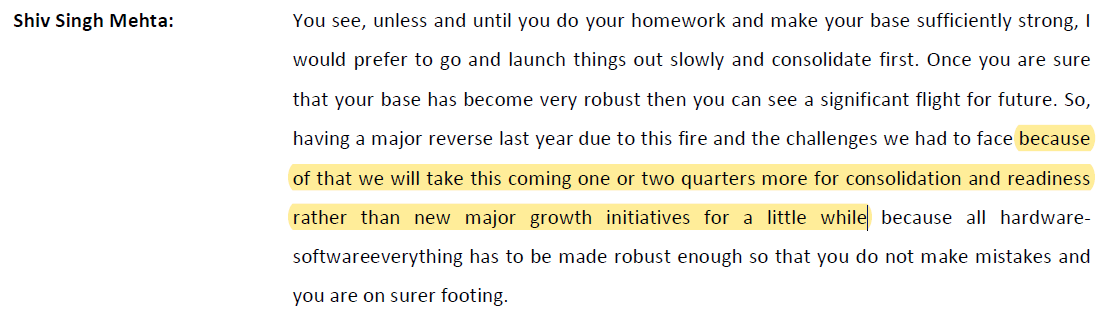

I think the sharp fall is a mix of multiple factors. EBIDTA margins are only at 6% in spite of raw material prices correcting sharply over the past 1 year. To be fair, the management in the last qtr call had guided that the blended margins will be soft in the near term due to low pricing power in the industrial segment and currently they are seeing higher sales in this segment. The management has also guided for only 10+% growth in the topline for the entire year.

I think this story may take a little while to unfold.

Disclosure: Invested from lower levels

1 Like