The Kriti stock has run up more than 30% since this thread was initiated about two months ago. Perhaps the market is slowly beginning to appreciate its stupendous growth in the first 3 qtrs of the current year & a higher dividend suggestive of better days ahead.

The recent run up could also in part be attributable to the expected above normal monsoon this year, after two successive drought years as a major part of Kriti’s Sales come from agriculture.

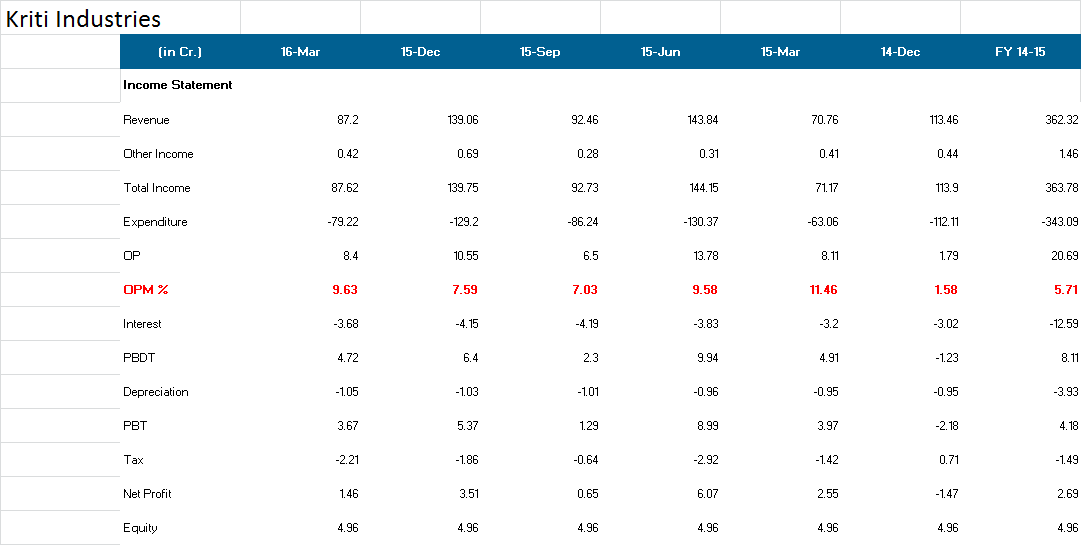

@drgsrk2006 : I actually think Q4 was not a bad qtr for the Co., despite reduced PBT. Here’s why:

Decent sales growth of 23.3% despite falling RM prices. Infact, Sales grew well in each qtr. Total Sales growth for 15-16 is about 27.6%.

OPM is the highest in Q4 & is showing a rising trend over the last 3 qtrs. Last year due to volatility in crude prices, the OPM’s went all over the place, with Q4 showing exceptionally high margin, while Q3 was equally bad which is clearly not the norm.

Even if only the current growth momentum with existing OPM’s are maintained in 16-17, does it not augur well?

As a share holder, I had written to the Co. asking for the break up of interest outgo between Fund based & Non Fund based limits, as it was creating a lot of doubts in the minds of investors.

The following is the clarification recd from the Co.

" The total finance cost of the company is Rs. 1585.06.The break up is as under.

Interest on fund based limits and term loan is Rs.529.23 lacs Interest on non fund lc/Bg bills discounting is Rs.766.21 lacs. Bank processing charges Rs.289.62 lacs. ** Corresponding Bills discounting payables shown in Balance Sheet as creditors.** Bank limits varies from month to month as per business volume in peak/lien season.

Effective average interest is in the range of 12 to 13%"

Hope it helps in getting a better understanding & insight into the Co.'s working.

Kotak Securities has come out with a research report on Finolex Industries Ltd. While there is no denying that Finolex is a much bigger & established player, the rationale behind the recommendation is largely similar to that of Kriti.

The Annual Report of Kriti Industries for 15-16 is out & the under tone is bullish. The mgt expects the current growth momentum to continue going forward. The Mgt. discussion & Analysis gives decent insights into the Co.'s working.

I have gone through the Balance sheet. Some observation on which if you can throw light would be very helpful:

what has been nature of advance receoverable in cash and kind worth Rs 16.56 Cr on Standalone financial as on March 31 2016? Which are parties and rationale for same as it is significantly higher in context of total current assets.

Refer to page 53. Some excise duty of Rs 75 Lakhs being paid (of which around 15 lakhs was for earlier years) on account of rate difference between fixed rate contract and dispatch value to depots/dealers due to observations made by DGCEI in its inspection to avoid any litigation on this account. Can you get more understanding about the transaction?

Page 53 and Page 36, the auditor report comment"

The Company has disclosed the impact of pending litigations on its financial position in its financial

statements- Refer Note 27.3 to the financial statements.

Note 27.3: Claims not acknowledge by the company on Commercial tax matters Rs 244.19 Lacs (Previous Year 255.89 Lacs).

Ant specific reason for auditor to highlight only 27.3 note when there are other two contingent liabilities also present? Whether any judgement has been passed on the mater due to which auditor has differentiated between 27.1 & 27.2 from 27.3 in contingent lialbity?

Page 32, any specific reason for not incurring mandatory CSR expenditure during FY16 and FY15?. Also on same page, note to account mentioned for gain from forex (included in other income) in P&L account but not mentioned where it has classify loss on forex in P&L? The amount are given in the balance sheet.

Any idea about plastic proccessing capacity after completion current projected capex of Rs 14 Cr? Also likely commission date of new project.

Your queries are relevant specially about the advances given. I am forwarding them to the Co. Hopefully they will be addressed. Will get back as & when I hear from the mgt.

Kriti came out with June qtr results that were flat. However, the interest outgo, which for many investors, is really the Achilles heel, showed a sharp decline of 27%. With cash profits of about 15 crores in 15-16, & more expected in the current year, the need to discount bills would reduce somewhat. We will know more as the story unfolds in the next few qtrs.

@atishay1 I am afraid this business does not have any moat as such. It’s a pretty commodity type business, though it sells under its own brand “Kasta”, which is a pretty respected in the markets that it operates in. What I do like about the Co. is that it is being run very efficiently, going by the RoCE. The Mgt is trying to go in for more value added products like fittings to get better margins. The investment thesis here is that even a slight improvement in margins could make this stock look attractive. With the tail winds of a good monsoon, I expect 16-17 to be a good year.

There is a school of thought that feels that since the interest outgo is high as compared to the debt in the books, it is perhaps not giving a fair view of the business. My view is that having debt on your balance sheet is not exactly a feather in your cap as it adds to the perceived risk. How I wish other companies laden with debt, too could get their bills discounted & de-leverage their balance sheets! It would make life so much easier for humble stock pickers like us!

I gather from reliable sources that the Co. has recently completed the modernization of its plant. This should lead to better margins in the second half of the year. It will be interesting to see how this story plays out going forward, but with a good monsoon & the plant modernization in place, the tail winds seem steady.

Kriti hit an all time high on the BSE on Monday with good volumes. As mentioned earlier, one of the problems with small cap stocks is a certain lack of information on current developments. It would be great if a few Indore based valuepickrs could do some scuttlebutt on the Co., about the market perception of it’s brands / promoters.

We need to find out whether the reduced interest outgo in Q1 was a new normal or just a one off? If so, then interest savings alone could add about a rupee to the EPS, in addition to the regular growth. It would also help if someone could check if the flat topline in Q1 was more due to the then ongoing plant modernization? I guess Q2 results would address some of these issues

The Co. has informed the BSE that it has commenced commercial production in the new plant for manufacturing Water tanks & CPVC pipes & fittings. As these are higher margin products, the operating margins should start showing an improvement from Q3 onwards on higher sales due to the commencement of Unit II. This should further improve the Co.'s already high return ratios.

With good monsoons behind us, the sector as a whole seems to be getting re-rated.

The Co. is seeing a lot of trading interest on the exchange & most of it is delivery based with increased volumes. Attaching the trading details. Perhaps a reflection of the increased interest in the sector.