True…here is the detailed article on it.

3 Likes

440 levels now. Something’s certainly up. P/E is now dropped to 23 and LT Foods is meanwhile nearing 20 P/E levels.

Disc: Not Invested

I doubt if Pabrai will sell off. Generally, he is in the company for a long-term (definitely not a short term).

He has recently said that whenever he buys a stock, it goes down (as in case of KRBL).

I am sure he must have a strong reason to buy into KRBL at the highest price and high PE. I think it would be interesting to know what his logic to get into the counter.

2 Likes

Mohnish Pabrai buying into KRBL ( at the price that he bought ) is another example of the human fallacy. A guy that for ever spoke about his liking for buying businesses cheap ( infact going to the extent to say that he should be able to explain his buying rationale to a kid ) has bought KRBL at peak valuations. Let alone kids - i am quite sure this investment of his has left experienced investors perplexed.

A lesson for all those who look up to celebrated investors - do listen to them, do study their behaviour/actions but you’ll only do well over a long period of time if you build your own philosophy and diligently stick to it.

6 Likes

At 433 i.e 22 P/E, the discount was too good to ignore so have taken the plunge after tracking this for months. Hopefully this is just LTCG related volatility and nothing fundamental to do with the business. Let’s see.

Disc: Invested

12 Likes

anyone reason why there is no substantial mutual fund holding? and highest public share holder is reliance commodities dmcc…dont know what it it

After holding for almost 3 years and making great returns on KRBL, I shifted to LT Foods in November, as the valuation gap between the two was huge. Now with KRBL falling and LT Foods holding up, the valuation gap has really narrowed. This has compelled me to rethink about going back to KRBL as in terms of performance and brand it commands a premium, compared to LT foods.

1 Like

I believe the China opportunity might be the primary reason behind Pabrai’s investment decision. The direct imports into china from India are allowed only since Sept 2016. Dont remember the source, but heard that the chinese people in western countries accepted Basmati rice well. So, there is good chance that the Chinese residing in China might also accept it and over the time the Basmati imports into China will grow. So, KRBL will be in good position to capture some of the Chinese Basmati market. As the per capita income in india grows, the Basmati consumption in India will grow too. KRBL has brown basmati rice product, which health conscious people can consume daily (as normal brown rice is not much palatable).

Disclosure: The opinion is personal. I don’t have much in depth knowledge in this subject.

Invested today & it is reasonable part of my Portfolio.

Fan of Pabrai, so the opinion might be biased.

2 Likes

Shifting portfolio from Chaman Lal to krbl due to valuation attractiveness based on quality. Coming to pabrai investment n deciding whether he purchased cheap or expensive ,only thing I can contribute is ,currently basmati rice is 2% of overall rice consumption , 60-70 % of rice market is still unorganised ( no from some of reports I read but I may go wrong on exact nos).as per capita income increases, people prefer improving rice quality intake, India gate is more than a national brand due to Indian population in various parts of world. All said and done , rice plays in a 2-3 year cycle (based on last 10 years of data ) and this counter will also give multiple opportunity in cycle play out ,however, the brand power looks strong to ve pricing power in adverse times which are common (yet doing pricing power analysis ). If anyone has gone through AR in detail ,please share if any major governance fallouts (have taken little bigger position without fallowing regular due diligence process based on overall story n yet to go through in detail ). Disc : transacted in krbl (buying) n Chaman Lal (selling ) in last 3 months

2 Likes

Hi,Would you be kind enough to share your rationale behind this Insight? Regards.

I have gone through last 6 years of AR and last 3 years of quarterly conf call transcripts. One big thing that I noticed was KRBL’s huge investments in energy segment. The main reason for them foraying into energy segment was to take advantage of MAT. Management for last 7-8 years was falling under MAT and the IRR for energy investments was coming to 22-23%. Lately, because of the current power pricing and output, the IRR is falling below 22-23% and hence KRBL is no more interested in power sector. I didn’t see anything that was shared by management as to how they were coming up to 22-23% IRR for energy investments. However, management’s recent assurance to not deploy any further money in energy sector was helpful.

On a separate note - below is what Buffett mentioned in his 1991 letter

an economic franchise arises from a product or service that:

_ 1) is needed or desired

2) is thought by its customers to have no close substitute

3) is not subject to price regulation

The existence of all three conditions will be demonstrated by a company’s ability to regularly price its products or service aggressively and thereby earn high rates of return on capital.

In my view, KRBL strikes well for all of the above criterion and is a superb Franchise. There is only limited quantity of Basmati rice that will be produced every year in GI region. No one except India & Pakistan can produce it. This precious commodity will be in limited supply and demand shall always outpace supply as more and more people migrate to consume it (value migration + unorganized to organized). And hopefully KRBL shall continue to dominate with its leadership position and pricing power contributing to high ROIC and ROEs along the way.

Disc: invested and accumulating heavily with recent fall.

11 Likes

Thanks for that. Its good to know that they have no further intentions of deploying money into the energy business.

In reference to my earlier comment though ( referring to the Pabrai investment ), I by no means implied that KRBL isn’t a good/great company. I was referring to a learning we have all had - a great company need not always be a great stock. The per capita consumption being low applies to a wide array of products and services in India but we know that doesnt mean all the companies catering to those products/services are great investment ideas.

The corner-stone of great investing is to buy good/great companies at a big/huge discount ( in other words with a big enough margin of safety ). In Pabrai’s own words, they need to be screaming buys and that is something that I could not understand in this case.

Coming back to my own view on KRBL, I believe it is fairly valued now but in my books, the margin of safety is still not good enough. While I hope they do not indulge in more experiments in sectors such as energy but Anil Mittal has spoken about diversifying into other agricultural products. That will most likely happen - how and when is unknown so that needs to be built into the margin of safety.

2 Likes

Thank you, @rupaniamit for sharing the information about annual reports and con calls. It has saved me few hours for sure.

I agree that Basmati rice, in general, has specific characteristics which are unique (can be produced in India or Pakistan). However, I am not sure if I can say safely that the product has a no substitute.

I agree the brand has a strong recall, good market shares in different part of the world. Being a commodity, Basmati rice is also subjected to pricing pressure. For example, if I want to purchase it, I would go for the basmati rice which is on offer. I also checked with my few friends and they more or less confirmed my understanding. I am sure some people would eat specific brands, but I find it difficult to tick the box “No close substitute”.

In addition to the point you have mentioned about buying the product, I would like to add one more point. It fits the criteria of companies “Buy commodities and sell brands”.

What could go wrong (things to watch out):

- The stock has given huge returns lately (last 3-4 years) due to valuation a multiple, where the stock PE has risen from single digits to around 30(recently). If the market corrects further, the stock may go down also.

- One of the reasons I bought into the stock is due to Monish Pabrai buying into it. I am yet to build up conviction on KRBL yet. If he sells his holding indicating that it was a mistake to buy into KRBL, the stock price can suffer.

- Any changes in the price of Basmati rice will have a detrimental effect on price.

Disc- Tracking position and adding more.

1 Like

I am relatively new to investing. I have a doubt here. Why do people think that for such a commodity like “Basmati Rice” which is being sold since 100s of years, any company deserves PE rerating from 3 to 36 ( 12 times ) just within 4 years? What is so great about Basmati Rice , discovered only 4-5 years back and why this PE cannot go down back to historic levels? Kindly help in understanding.

Earlier from Oct 2010 to Sep 2013, PE has gone down from 10 to 3.25 and Price from ~50 to less than 20. Source RateStar.

Discl : No position, no intent to buy.

7 Likes

Read your post later. Was making the same point. Anyways, I do not believe that Basmati Rice (or its usage) is a new invention that can sustain 12 times higher PE for a long duration. Yes, Markets can remain irrational for long times.

You may be right about 12 times PE and if you wait you may get it.

I think the valuation is a subjective matter and depends on how one look at the company (in a similar vein as Beauty is in the eyes of the beholder).

A month back, the market was offering 30+ PE to the company and today it is 22. So it depends on how one value a business.

Sir, Compounded Sales Growth, for such a great brand:

10 Years: 13.64%

5 Years: 14.06%

3 Years: 2.66%

TTM: 10.62%

Last 2 quarters, YoY growth is negative.

Source : screener

Sure enough but its highly unlikely that we will see historic low PEs returning to this counter simply because KRBL is a well-known story right now unlike what was the case 3-4 years back. It has also come on the radar of institutional investors - i remember even Ramdeo Agarwal spoke about it when KRBL made an entry into its list of wealth creators in its annual study.

It can only go down to those levels if the management does something stupid ( like an expensive de-worsification ) or if some black swan event hits the business.

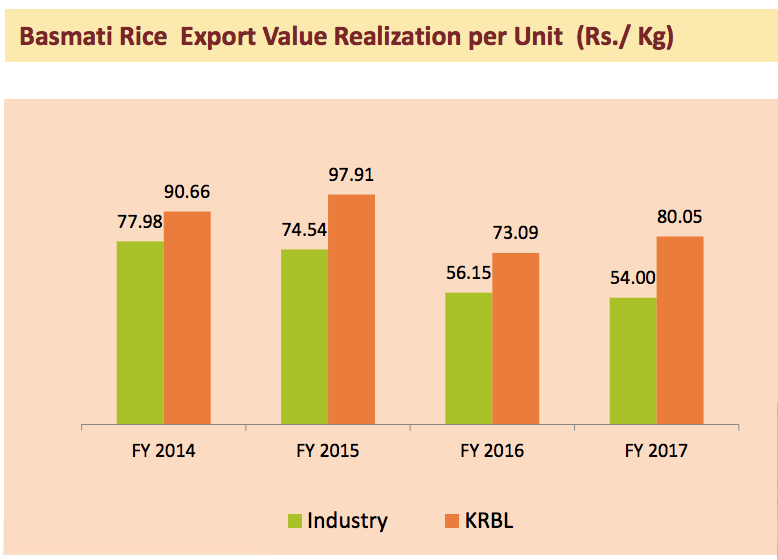

Now when you call basmati rice a commodity, do look at the following realisation per kg of exported basmati rice of KRBL vs Others and tell me why this is so. How can a company be able to price its “commodity” so much higher than others and still keep increasing market share?

Even in domestic, KRBL’s brands have the highest market share in Urban (32%), Rural (43%) and Class 1 Towns (35%).

Source: KRBL’s Recent Corporate Presentation and FY17 AR.

When market assigns a P/E - It looks at the following

- Size of opportunity - Can market size increase at a certain CAGR for the foreseeable future?

- Margins - Can realisation be maintained/increased with increase in volumes?

- Profit growth - Self-explanatory and this of course correlates with #1 and #2

On all 3 counts, KRBL’s basmati rice story is strong

-

According to reports (Basmati Rice Market Insight and Trends 2022), the market size should grow at a CAGR of 12.90% from 2017 to 2022.

-

Current year’s OPM is around 23% which is the highest the company has ever recorded. As Dhuri plant’s utilisation goes up, this will go up further by FY20. LT Foods in comparison has a OPM of 11%. But basmati rice is a commodity right?

-

5 Yr PAT growth - 34% CAGR.

Then there is the 2000 Cr inventory they are holding which was built at a low cost. If realisations go up in FY19, it could be a windfall profit in the near term.

This is a FMCG company with a strong aspirational brand and pricing power and not a pure commodity business. If you read Munger’s Practical Thought about Practical Thought, you can see the number of boxes KRBL ticks in building a strong product. Even the way they approach marketing is very 2017 - They use food bloggers to create the network effect. They use celebrity chefs to endorse and create recipes. See their quinoa campaign for example. You don’t see HPCL or a Hind Copper doing that do you?

20 Likes

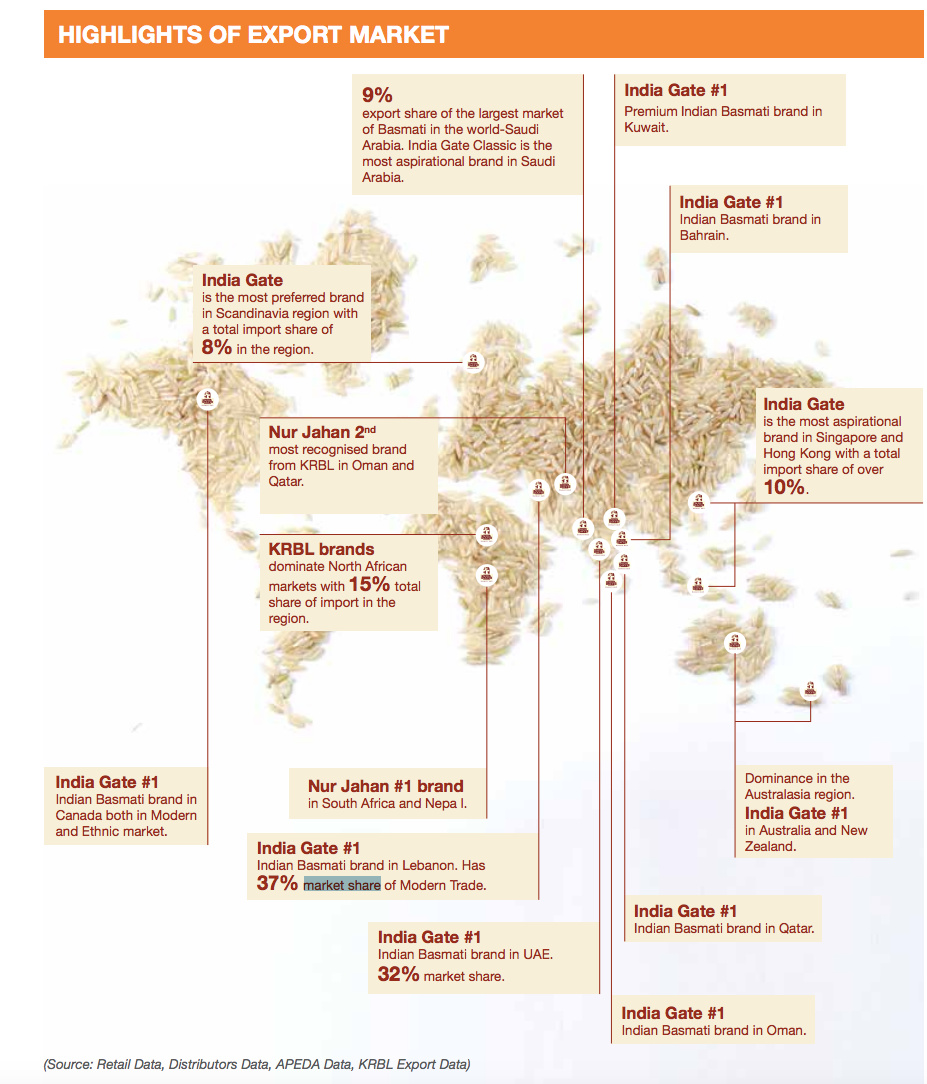

It’s Middle East and not India the biggest market of basmati rice. In FY 2015-16, Saudi Arabia, Iran, United Arab Emirates and Iraq accounted for a majority of India’s Basmati Rice exports with 23%, 17%, 15% and 10% share respectively. India Gate Classic SKU market in India is only 10,000 MT whereas its market is 40,000 MT overseas (most of it in Middle East). Management is very sure that price fluctuation in their flagship brand is going to be almost negligible even with falling underlying paddy prices.

I completely respect your opinion on Basmati being easily substituted. But IMHO - below points on why I feel that basmati is a unique and rare commodity with no close substitutes:

- Middle East folks are not going to eat anything other than basmati rice. They have been eating only basmati for generations and will continue to do that. They are basmati rice lovers and will not compromise on the type of rice they eat.

- You pick India Gate Classic rice packet and you will get same excellent quality all the time regardless of the time of the year. This is why its commands premium pricing for the excellent quality it provides. Such consistent quality builds “brand loyalty” and “customer stickiness” who will pay-up for the quality. KRBL has been very successful in doing this.

- Personally, I come from a Sindhi family. Our family has not consumed anything other than basmati rice for decades. My dad and uncles are very picky about their basmati rice. They are discerning when it comes to taste, flavor, and aroma of the rice they consume. We still buy basmati rice in bulk (from unorganized retailers -

) and age it for years before we consume it. I can correlate such discerning behavior by Middle East consumers as well other Indian consumers.

) and age it for years before we consume it. I can correlate such discerning behavior by Middle East consumers as well other Indian consumers.

) and age it for years before we consume it. I can correlate such discerning behavior by Middle East consumers as well other Indian consumers.

) and age it for years before we consume it. I can correlate such discerning behavior by Middle East consumers as well other Indian consumers.I recommend you to hear quarterly earnings call (if you have not don’e already) and you will realize the value promoters bring to the table. To me - they are street-smart and doing amazing job. They know when to pile up on paddy and when to put brake on it. These are astute businessmen doing this job for more than 4 decades and in rice (or any commodity) business - trust me experience counts more than anything. They are where they are (worth almost $1 billion per today’s market cap) because of the “right” business decisions that they have taken so far.

8 Likes