KRBL is one of the companies featured in “India’s Emerging Global Companies” report by Ambit. As always, the report illustrates a good framework/checklist (deserves a dedicated thread for discussion). The following is excerpt of an interview (related to India’s EGC report) by Outlook Business with Nitin Bhasin, head of research at Ambit.

What innovation are we seeing in a commodity such as basmati rice?

Innovation doesn’t necessarily have to revolve around R&D, it could mean doing things differently. The kind of people the company hires, the kind of machinery the company uses, the branding strategy that it adopts and also what unique processes does it follow. In the case of KRBL, innovation can also be seen in its farmer engagement programme. KRBL maintains its own farms to identify the kind of seeds it should be developing for better yields even if there is not enough water. Although it has not entered into contract farming, working with farmers has helped create a strong ecosystem. On the distribution side, it has entered modern trade. It is building a portfolio of multiple brands of rice with different positioning. The KRBL story is not widely known with hardly any institutional investor presence. The whole sector was stereotyped as most rice players ran their businesses in a shoddy manner. KRBL changed the perception. Look at its return on capital employed versus the industry, it clearly stands out. Look at its branding practices versus the industry, it’s different. This is in spite of the fact that KRBL’s product may not be the most expensive compared with peers, but it is more profitable among its peers. KRBL has complete control on its production process — right from power, raw materials to the farmer. At the same time, it is focusing on making the balance-sheet better. The story for KRBL began when it developed a seed with better productivity — the rice that came out from the seed was of a superior quality and found wider acceptance. But the company did not just engage merely in product innovation, but innovated its processes as well.

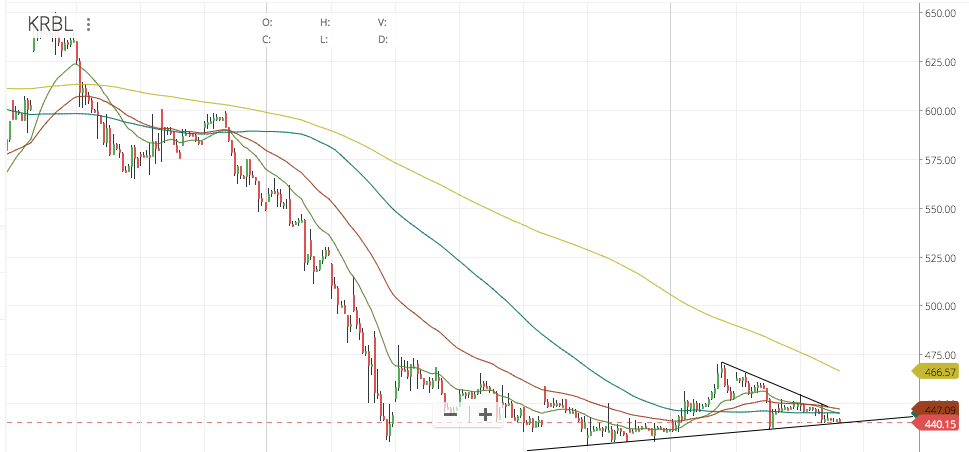

If you have read MPs book,the dhando investor…he is very much using DCF for ratifying his investment rationale. Also,he has a very strict time frame also…say about 18 months to get the most out of his investment.Since KRBL has fallen from 600 to 440 odd levels…do you think it will be able to get to 800 IN 18-24 months to get MP his desired result. YOU may be thinking I am too focused about the price,but all the hard work ultimately is for the price.

Aslo,one more thing which I don’t know is ok. In india in rice/.wheat or any sort of agricultural market there is a large amount of unorganized debt(hundi) as they call it…I think they use this thing a lot. NOt verified but heard from small people in the rice trade.This will no way reflect in the balance sheet but only pump up the value of the inventory having a positive impact on the share price.

i think MP will not be able to figure this thing out…unless he has gone to khari baoli in Delhi.

The way I see it is, ignoring the Price for a minute, Basmati is still seen as a luxury food item. So, it is not recession proof. Should there be a shock in the economy or some kind of local money crisis, the first thing people will drop is buying luxury. My investments are more aligned towards basic human needs in a specific industry. So as far as products in the rice industry goes, I might be more interested in tractors, seeds or basic farm equipment. In the rice exporting space, I might be more inclined towards basic rice variants and not Basmati.

The only exception is if the product is primarily targeted towards wealthy people. An example would be Eicher Motors. The affluent do not care about percentage point changes in inflation. They are buying the product for its aesthetic appeal or bragging rights. This makes the product partially recession proof.

I have not done market research or anything to see if customers of Basmati rice have started looking at it as a necessity rather than a luxury. If that is the case, that makes KRBL a better investment. Of course, these are ultra-safe checks to ensure you stay out of cyclical stocks. It may or may not apply to market leaders like KRBL. But I’d still be cautious if I ever were to invest in it.

Coming to the question of Price, you can download my DCF template from here and tell your own story:

The most important thing in Valuation is to tell your own story and then try to match the numbers to fit that story. If you want to tell a wonderful story with KRBL taking over the Basmati Exports market, go ahead and tell it with appropriate numbers. This will get reflected in the Value, but then you will have to live with your story.

Nobody can say when the Price will revert to Value. MP himself suggests holding a stock for 3 years to see if it reverts to Value or sell it. So, you may want to follow that. Warren Buffet on the other hand, has held on to under-performers for as much as 7 years (IBM). Of course, if it does revert to Value, then selling the stock will depend on availability of better investment opportunities. If a company, even after reverting to Value, produces extraordinary CROIC, it makes sense to hold on to it. Again, of course, provided you don’t find another company with a higher CROIC and which is also a better investment opportunity.

Hence US missile attack in Syria followed by rhetoric from Trump about Russia and Iran is bringing back possibility of US sanctions on Iran. In that case, India’s Basmati export can come under pressure. I believe this is the reason for softness of stock prices of all rice exporters like KRBL (although LT foods and Chamanlal Setia are up today)

Found this product on Costco shelf in the U.S. Please notice how it says ‘Grown in the U.S’ on top right corner. Isn’t that non compliance to the GI tagging that Basmati enjoys ? How / which body ensure the Basmati tag is not used by any other regional grown rice ? Next to this was Royal Basmati, royally claiming itself as the nos one Basmati rice in USA.

If you see the shareholding, the only major change is the Balsharaf’s have reduced stake to about 3% (from 6.38%). This is about 73 lakh shares sold. Pabrai Funds have bought about 64 lakh shares. Although, Pabrai Funds is not listed in Shareholding, you can see that there is Clearing house (INDIAN CLEARING CORPORATION LIMITED) which is holding about 65 lakh shares. I think this could be shares of Pabrai Funds which were yet to be transferred as of 31st March, There is hardly any change in retail holding and Anil Kumar Goel’s holding is completely intact.

But then this brings the question of who did the selling in March. Did one of the Goels sell and then buyback before end of quarter because of LTCG? Or did Pabrai have buyer’s remorse and so dumped the shares after a month of buying? I don’t how clearing houses work and if they can hold a client’s shares for nearly 2 months. Can someone shed some light? It could also be the other 9 lakh shares (73 - 64) of the Balsharafs ended up in the open market in March.

Clearing houses are intermediaries between buyers and sellers. They become the buyer to every seller and the seller to every buyer. This reduces risk for the concerned parties and enhances confidence.

It increases the faith of the concerned parties by assuring every buyer that shares will be delivered and assuring every seller that money will be credited to their account.

If either party(buyer or seller) doesn’t keep their end of the bargain the clearing house will intervene and facilitate the deal.

For example-

a) If a buyer refuses refuses to pay cash the clearing house will pay the seller.

b) If a seller refuses to deliver shares the clearing house will deliver shares.

The clearing house reduces risk by demanding margin.

In most cases deals are concluded in 3-4 working days.

In this case I’m speculating so please excuse me if I err-

Is it possible that Mr. Pabrai’s fund didn’t buy the shares and lost the margin deposited. The clearing house stepped in and acquired shares of the seller and they’ve held on to it.

Second possiblity: Mr. Pabrai sold shares a few days before 31st March and in the meanwhile the clearing house was in possession of shares.

Third possibility: There’s a dispute and in the process of resolution shares are in the custody of the clearing house.

Found this in Walmart Canada, if you look closely, these are imported and packed in Canada. I am sure it must be the case with Della also. It would be interesting to know who the suppliers are!

That was my initial thought too. But look closely at the top right corener of the pic I posted. It says “ Grown in the USA “ . I did check at the back and dint find any supplier info.

Can u please give me the source with page number.In 2010 their milling production was 324734 MT (i.e 3.25 lac MT) ,source annual report 2010 .On the other hand you are saying it is 594 lac MT in 2017.Something is amiss.

Corrected the typo above as 594k not lac. Apologies.

And i don’t hv call transcript…these are from my notes from listening to their calls. Usually, these figures are given in the beginning of the call.