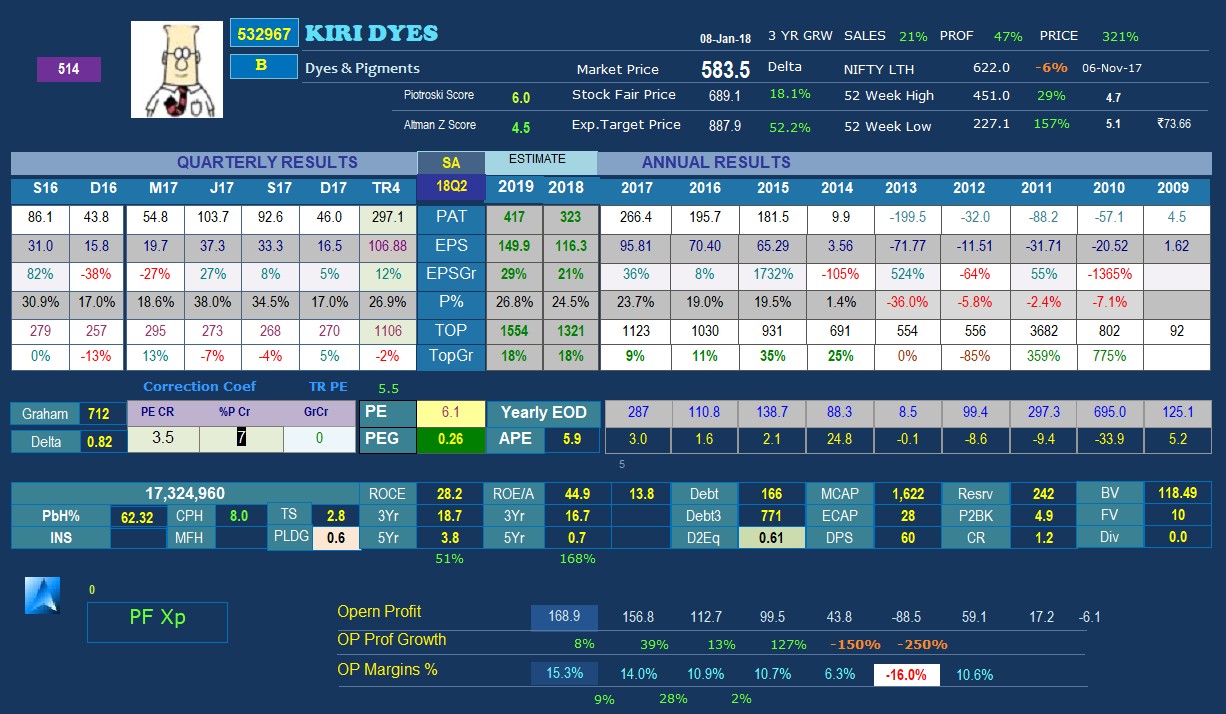

Kiri Industries: the latest shareholding at the end of Q3FY18.

Interesting to note that with recent conversion of warrants by the promoters , the promoter shareholding has increased from 37.68% to 42.62%.

However there are pending warrants issued to the public to the tune of 2,04,90,262 warrants which at the end of conversion will lead to the dilution of promoter holding to 26.99%.

As per Q2 FY18 shareholding pattern, the pending public warrants were 1,45,93,620. Why has the company issued around 60 lakh warrants to nonpromoters in the recent quarter when the company is doing well in a favourable sector scenario?

the pending covertibles are not warrants but FCCBs. Kiri’s FCCBs are partly paid bonds. As & when bond holders pay additional instalment on bonds, the number of shares to be issued on conversion goes up. This number has been going up every quarter. Three are still amount yet to be collected on bonds. The conversion price is a mere Rs.12 per share. Adjusting for Fx, it currently works out Rs.17. Don’t know why Kiri is doing this. It had the option to redeem these bonds this month (JAn-18) but it decided to extend the maturity period by a few years! May be the promoters hold the bonds via benami. Otherwise, why would promoters extend maturity of bonds and not redeem when stock price is 600 and conversion price is Rs.12 / Rs.17?

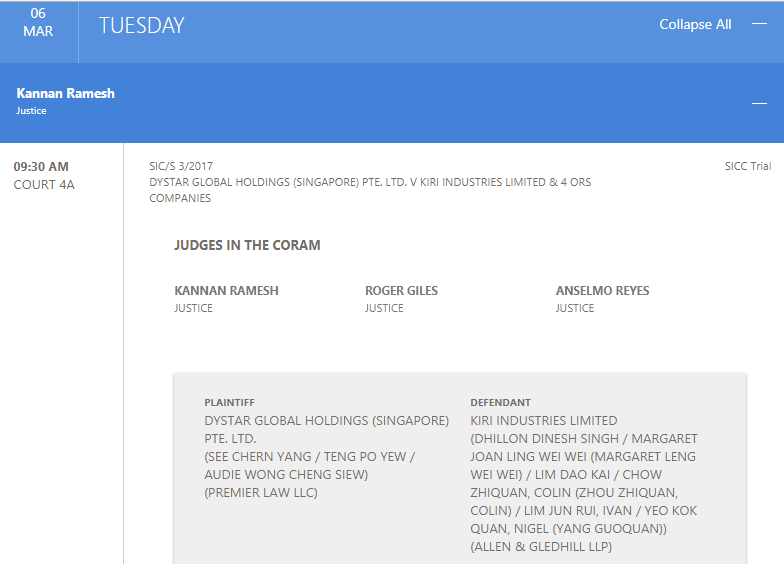

The hearing of the case is until 16th of Jan, as per the Singapore Supreme court hearing list. I guess any meaningful outcome will only be known once the hearing is complete.

If at the end of the last hearing date ie. 16th Jan , the hearing is complete; the case will be shifted to the verdict list and the verdict will come out soon. If further hearing is required, then the Singapore supreme court may announce further dates of hearing.

Any idea where one can find earnings call transcripts for Kiri - I could not locate these on researchbytes.

Feel that apart from the operational/ financial aspects, need to get more clarity on the shareholding related aspects - the AR does not provide full clarity regarding outstanding convertible instruments and the terms associated.

Agree but the warrant exercise price being lower than market price (at the time of conversion) would imply dilution of existing equity shareholders. In the absence of full clarity on this, I feel its difficult to picture EPS trajectory.

Kiri moving well with expectations of good Q3. H acid and vinyl sulphone prices are high and China shutdown gathering pace. Kiri should get a GST refund as well reflected in Q3. I feel on a standalone basis price should be minimum 670 assuming a PE of 18 which is reasonable compared to peers. So with Q 3 earnings this should move higher. Also, if case is won in Singapore then consolidated EPS must be considered and stock can surge past a 1000 in short term. Dilution is not a concern, fccb dilution is in 2022. I am also waiting for this sector to be re rated and trade at higher multiples. Pls read the blogs dedicated to Kiri. They are very high quality.

Disc-have a significant chunk of my portfolio in Kiri. Views are biased.

While searching for a transcript of the hearing, I came across a Singapore court order 19 December 2017.

This appeal was filed by Amitava Mukherjee, Kiri’s director on DyeStar board, when he wasn’t given access to certain documents and information. The case was ruled against the said Kiri. Here’s the judgment summary:

“I have dismissed the plaintiff’s application. In my view, the plaintiff’s

primary or dominant purpose in bringing this application is an ulterior

purpose,4 which is to advance the interests of a minority shareholder of the

company in a minority oppression suit against the company and its majority

shareholder. Given that that finding goes to the root of the plaintiff’s

application, reframing or narrowing the categories of documents which the

plaintiff has specified in his application cannot salvage it. For the same reason,

the plaintiff’s offer of an undertaking to the court to maintain the

confidentiality of any documents which he inspects pursuant to a court order

granted on this application cannot salvage the application.”

In light of this, do you think Kiri has a chance to win minority oppression case against DyeStar/ Longsheng? And if they lose the case, what worth is their 38% stake?

It was observed that the matter was listed for hearing yesterday in Singapore Court . If anyone has any update about the hearing request you to share the same…

Two cases are going on simultaneously: 1.kiri has accused Chinese company( Lonseng) of oppression of the minority stake holder by the majority stake holder. 2. Dystar/Lonseng has accused Kiri of hijacking dystar clients and is supplying dye/ intermediary to these clients from Kiri’s standalone factories which the Kiri has outrightly rejected.