yes for a 40% roce biz, trading at 12x does look attractive…but question here is whether they can maintain this RoCe level in future given the restriction on selling price and contingency on cost structure regarding royalty?? i fear this year their ROCEs/ROEs will be sub 35% or less given decline in earnings and increase in capital base (higher payout has been ruled out). For next year, even if they go for credit market and go aggressive on sales, i fear quality of earnings will remain questionable while their base on capital employed will remain high…

one should closely look at royalty issue than only one can get a fair idea of how earnings pan out in fy17…paddy opportunity is huge and hv shown some traction this season also but to show meaningful contributer to p&l i think one has to wait añother 4-5 years atleast…plus dynamics in paddy (like v r seening in cotton recently) need to be understood…

Why is there no need to provide for contingent liability as per conservatism principle of accounts? Contingent liability has to be provided for when a claim arises and not based on outcome. If it’s based on outcome how come it is contingent liability? If it’s not provided as it is, it’s clearly a case of aggressive accounting. Isn’t it? Market is already discounting all this though a bit late.

Also could you please substantiate your claim that the cash is real. If there are book entries showing cash parked in MFs, does it make it real?

Also despite so many red flags, how come mgmt is ethical even without gold standard? Just because it looks statistically cheap?

pls check the AR to see the money parked across MF funds - tough to forge something like this.

I am far more worried about the ability to sustain the relationship with monsanto - they are a gate keeper and not paying adequate toll will ultimately economically dis incentivize the latter.

It’s only a book entry the way there is a book entry for cash in the banks. How come it’s different and tough to forge? It should be rather easy as you don’t receive any interest on it either. Could you please elaborate further?

As an aside, there is a big concern that kaveri has been losing market share to first class seeds by bayer.

can anyone pls do a check and get back to the forum pls ? were there kaveri specific issues that we need to worry about on sales or was it just a bad quarter for the entire industry

I believe the whole discussion is making information rich, however the situation is odd…a odd where you take a call and if it comes successful, it pays off. You know, what I mean. I am not sure yet, which side to take. Still…few points…would like to add.

In the concall, did u guys listen to the last question-from that discussion, I figured out that Kaveri seems to be a pass on player in the value chain as far as royalty is concerned. The fight is between gvt nd monsanto. However, if a extraordinary situation comes, where Kavri will pay high and cant pass on to customer (govt force)…seems unlikely to me. So, the ability of the company pass on the burden is there and hit on margin is less likely.

Now coming to other concerns like loosing market share/lower acreage/drought/cotton price and those things are more of cyclical…in my sense…these things may be there for 1/2/3 yrs…but is it a permanent downside ??? I don’t think so, guide me if there is a chance… A long term investor with 10 yrs horizon should be worried on this part ?

The revision of dividend, provision for 64 cr are all well taken,which the company should start addressing. However, I feel if some dividend is given (without raising further too) that is fine, especially when the company can deploy the money in the core business which is generating around 25-30% of return (RoCE/RoE). As some of you raised question on cash balance, weather that is real or not, that should be cross checked if possible, I agree on that part.

Last point, common guys !! now its available at 10-12x PE-even if RoE goes down to 25% and EPS decline by 10-15% in next 1/2 yrs, cant"s this be a ODD bet ? Not bad even in that case - Do u mean the company cant make a 10% CAGR in next 5/6 yrs - and what about the free cash it is generating - can it be around 600-700 crore by then (if it doesnt increase dividend and does any big capex)…above its current cash balance of 300 cr, taking 1000 cr cash balance.

I think odds are fairly in favour of kaveri and if there is no permanent damage to its brand/product/network…I am game. Educated comments are invited, if I have missed any long term negative which could damage the company.

After holding kaveri for around 2-3 years, what is coming out to me is that they need to diversify and be less dependent on 1 quarter results for them to get premium valuations. As of now IMHO market thinks it to be a one trick ( cotton) pony.

However, at this price there is an optionality being built in the price. u pay for cotton market share growth, with a kicker for new blockbuster seed.

Hi all

Please note that after Satyam episode no auditor will allow fudging of cash balance of mutual fund statements

For such large amount

I have no doubt that cash is for real and for a long term investor it is the best opportunity to invest in a cash generation business available at cheap valuation

My two cents (safe to assume that the thoughts below are completely biased as I am invested)

Scuttlebutt done in Jul reveals that 60-70% of purchase of cotton seeds were completed before price freeze was announced. So one could conclude that the impact of price freeze is minimal.

Business Impact: Short/medium term - negative - depends on the longevity of the price freeze order.

Lower sales due to deliberate choice of cash sales over credit is, to my mind, not a concern. In fact speaks of better receivables management. The product superiority should bring back farmers in future.

Business impact: none for long term as superior product should hold the company in good stead.

Lower sales due to loss of market share to Bayer (as pointed out by Varada) is of greater significance - impacts the long term story of the company. The company would have to come out with equally competitive product in future - time lines and probability of success is of relevance (opportunity cost?). Note that cotton makes up majority of the revenue and boasts of blockbuster products.

No doubt there is potential in non-cotton seeds. The company has exhibited ability to come out with differentiated and superior products. However not sure whether I have seen/come across a mention of a blockbuster product in non-cotton product portfolio (I could be wrong and being blind). If I am not wrong/blind then the company has to come out with a “Jadoo” or “ATM” equivalent in non-cotton portfolio to ensure that the long term story remains intact.

The promoters have been diluting their stakes - not very comforting especially when they have indicated that diversification have been put on hold. Not sure how to interpret this creeping dilution. Why would one want to dilute away from a cash generating high growth potential business?

Points 3 to 5 are of greater significance for long term investor I would presume.

A lot has been discussed after the results. My two cents;

Contingent liability is a provision made in the books so that if the things don’t pan out favourably for the company, there is money set aside to fulfil the demand. We as investors can always provide for this liability in our calculations and check if an adverse impact will debilitate the company. The answer is a clear no.

Royalty payment can eventually help the company. As has been pointed out earlier, the royalty per packet has come down from Rs 1600 per packet to around Rs 183.What is the litigation record from Monsanto and how successful have they been? Will Monsanto challenge this in court? Surely. Will they be successful, remains to be seen.

Let us invert. Let us assume that the Govt and the seed companies are successful and the courts decide against Monsanto. Kaveri paid Rs 64 crs less as royalty in Q1 based on the revised calculation. Let us take the management at face value and assume that next year they will sell 90 lac packets. By simple extrapolation, the impact of the reduced royalty cost itself will add Rs90-100 crs to the bottom line. Not something to sniff at.

What will Monsanto do? Monsanto will be very peeved that India doesn’t honour contractual obligations and the Govt has taken a decision to slash royalty without any consultations. It will surely go to the courts and try to remedy the situation. If the courts agree with Monsanto then it is back to business as usual. If for some reason the courts don’t agree, Monsanto can can also rescind their part of the bargain and stop supplying the technology to the seed players. They can also take the decision to not bring any new technology into India given the poor record of the country in honouring contracts. If Monsanto stops working in India, the second largest cotton growing country in the world, how will it monetise the huge outlays it has made in R&D. In my opinion, it will be very difficult for Monsanto to ignore India.

This is a classic case where the investor has to work out the odds of various scenarios playing out and placing odds on a variety of outcomes. This is what makes investing so much fun.

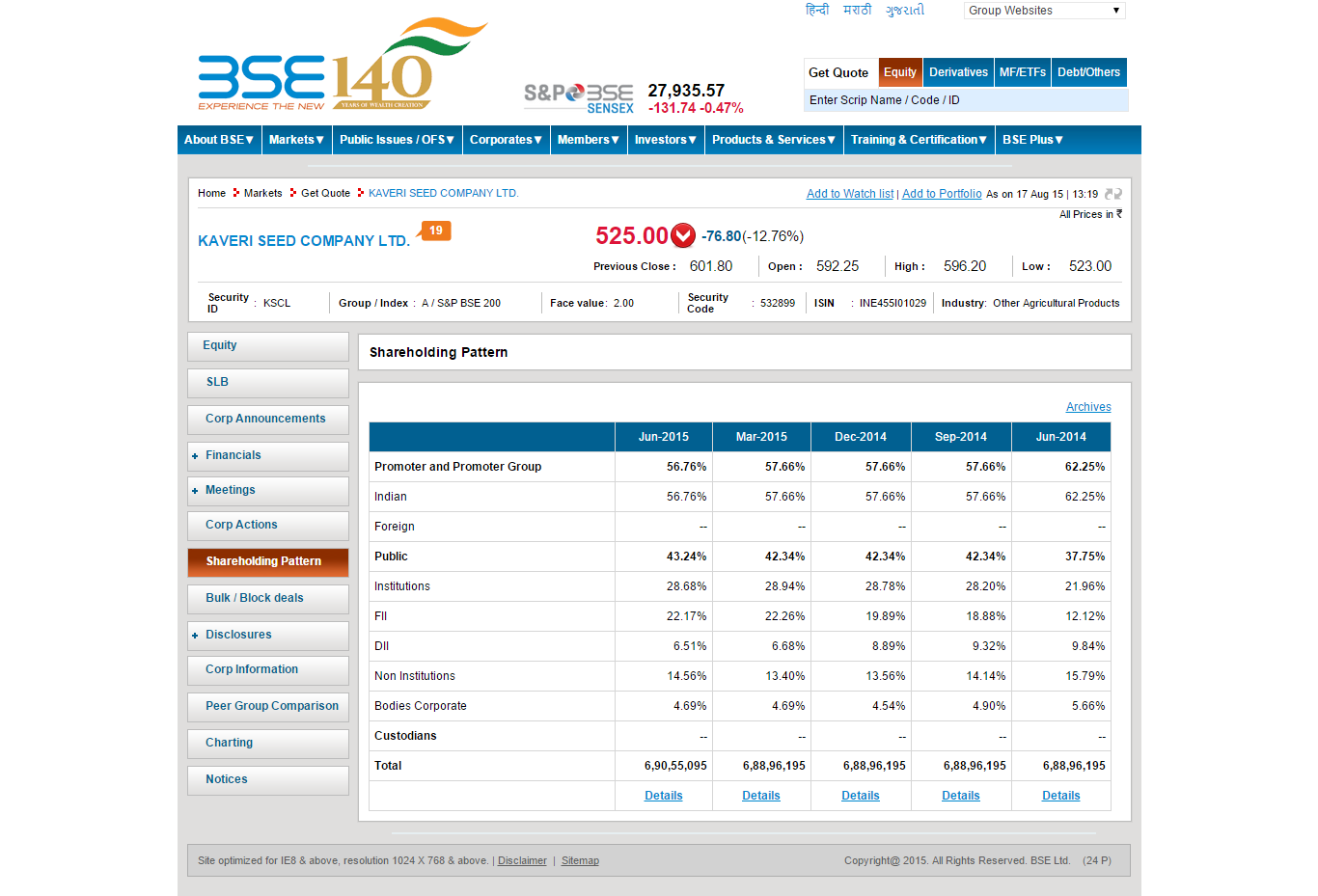

Kaveri Seeds - Promoters have reduced their holding from 65% to 57% in last couple of qtrs. IDFC premier has reduced holding to 3% from 7% in last 1/2 qtrs. Invert, why some body like IDFC premier who normally does not churn is selling ? that to reducing stake like anything. Does this mean there is a long haul of disappointment ahead ? Can this be a Value Trap ?

@Sanjeev_Panda - Please post your source of information. Below is Moneycontrol which shows a positive trend:-

Both Promoters and FII with increasing holdings.

Also - There can be a thousand reasons for a MF institution to reduce their holding in any company. That’s mere noise according to me. Kaveri posted below par earnings numbers, however the current stock price decline seems to factor in much more than meets the eye. Irrational mindset of herd or they’re actually onto something?

took DCM Shriram call earlier today…they have accounted royalty of Rs 180/pac…and not contesting with monsanto to reduce royalty…

as i mentioned…high roce this year wont sustain and next year also that risk of royalty will remain putting pressure on margins…(even dcm mgmt said flatly that it will impact margins if royalty is to be paid)

mrkt taking all of these issues negatively currently - promoter selling, no bonus/higher dividend, aggerasive accounting so on and so forth - stock down to 500

Assume they have to make full payment to Monsanto, not only for this year but also in the future.

Assume there will be no increase in cotton volumes or realisations for next year, while maize & paddy continue to grow as before.

In my estimate, based on these assumptions, the PAT would fall to roughly Rs.140-150cr. vs the current M cap of Rs.3,500 crores.

Pros

Good upside if the co does better than these worse case scenarios.

Cons

It will not stop falling until market is convinced that the co is following proper accounting practices and giving a true picture of its liabilities, both normal & contingent

Disclosure: This has been a long term holding in my portfolio. Bought some more today. Praying hard

@Rokrdude Aman - Sorry but completely disagree. I’m still not sure if you actually meant this or the other way around.

Peter Lynch - " If you can follow only one bit of data, follow the earnings – assuming the company in question has earnings. I subscribe to the crusty notion that sooner or later earnings make or break an investment in equities. What the stock price does today, tomorrow, or next week is only a distraction."

Can quote so many other Guru’s on markets being inefficient in the short-term. IMHO, markets value companies inefficiently during both bull (overvalued) and bear (undervalued) phases.

If you remove short term inefficiencies, Margin of Safety / Asset Plays / Cash Bargains - all these opportunities go out of the window.

In fact, I’d go so far as to say if markets were not inefficient in the short term, even that fraction of the people who currently make money from stock markets would not make money anymore.

PS: On Kaveri’s current earnings alone, it seems under-valued at this price. However I don’t have a great understanding of it’s business model.

Aman - Thanks for editing your post and reaching out!