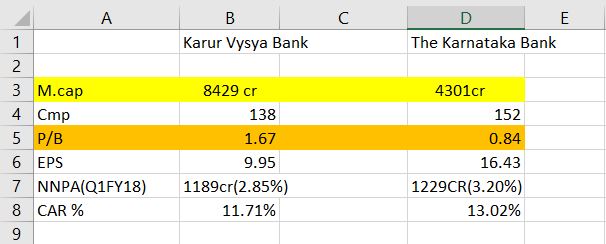

Karur Vysya Bank came out with its Q1 no.'s today…as far as financials are concerned it seems to be similar to that of Karnataka bank.

But as far as valuations are concerned the following table makes it quite clear…

7 Likes

In comparison of KTK bank with its peers, it looks to be performing better and still the performance doesnt show up in the stock price, can some one throw some light.

6 months ago, even KVB was trading at P/B of 1 and now reached fair value. Karnataka bank will also catch up.

In my view, the problem with KTK is that their current earnings power is a mirage given they are paying almost no tax. The normalised earnings will fall even if they grow the book once they have to pay 30-33% tax like other banks. The ROA is not “real” in that sense. Stick on a 30% tax rate and see what the real normalised eps is.

1 Like

I participated in the Karnataka Bank (KBL) Q2 Results investor’s call yesterday and briefly interacted with the management. My views on KBL below based on the interaction;

-

KBL has set an target of Rs 180000 crores business by 2020, As of September 2017 the total business is Rs 97000 crores. With 2 1/2 years to go, KBL needs to almost double their business. There past track record of growth is around 12 to 13% per annum in the last 10 years. This suggests that at a best case scenario KBL can achieve around Rs 135000 to Rs 140000 crores business by 2020. When queried about this, Mr Mahabaleshwara acknowledged that this will be a challenge but he mentioned that he will still stick with the target of Rs 180000 crores business by 2020

-

Profitability and efficiency is a major concern in my view. Though business per branch and employee has grown 6.5% CAGR over a 10-year period, profits per branch and employee is stagnant over the last 10 years. Any revenue / business growth is not adding to the bottom line

-

KBL is targeting a Cost to Income ratio of 45% by March 2018 down from 47.6%

-

NIM’s are around 3.1% which is a decent spread

-

KBL targeting 2% NNPA by March 2018

-

KBL looking at a consultant to drive their transformation initiatives. The bank is looking at the proposed / upcoming transformation initiatives for which it plans to engage a consultant to address growth, profitability, efficiency and future related issues. The consultant can propose changes, new growth ideas but how does one change a close to 100 year old culture. There is too much expectation and dependency on the proposed / upcoming transformation initiatives

-

I am also not sure how an old fashion bank like KBL can handle the digital & fintech disruptions and how well placed they are to capitalise on the digital & fintech disruptions. I have not seen any commentary from the management on this. They can potentially lose market share to new age banks and there could be a value erosion

Not convinced that KBL will be a multi-bagger. Happy for any contrary views on KBL

6 Likes

Dear Butun, Ref to this old post of yours, i just wanted to understand how the swap ratio are evaluated in the merger context being favourvale or otherwise… could you help me with a calc or link which explains ?

thanks alot, in adv.

Some good news after long time. Bank progressing but stock price consolidating.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/28a70070-3f22-4037-8a34-a497f088a8da.pdf

4 Likes

As per latest shareholding pattern, Kedia reduced his holding from 2 to 1.17% in previous quarter.

3 Likes

In a recent interview, he mentioned he would buy it back in the future. Please watch that interview on CNBC. The story still holds.

Don’t understand why he would want to do that. Is he looking to buy it at lower levels? Then that would mean there isnt enough margin of safety at current levels. Will search that interview.

We have to understand, his reduction in stake has nothing to do with the underlying fundamentals. Most marquee investors also play momentum to make quick bucks. Kedia is no different. Some of them will rebalance their portfolios by cutting their huge holdings and enter into new themes.

One thing that is clouding everybody in Karnataka bank is that it is not moving up. It requires tremendous amount of patience when we hold such stocks.

In my view, the whole banking is under pressure because of NPAs and regulatory revisions. Only time will tell how these turn up.

However, feel free to make your choice if you don’t find this bank attractive.

2 Likes

This stock is a long terms story. In my view, it will not play out in the next 6-12 months. Those who have long term horizon will benefit the most.

I am not worried because Karnataka stock price is not moving up. I am worried because I do not see considerable improvement in their fundamentals. In fact there is deterioration on some fronts.

If you look at 9 months result, you would notice that their CAR has come down to 12.2 from 13.2. if this continues then further equity dilution will follow. if they dilute equity faster than they grow the revenue then I, as an investor, am in loss.

Provisions have also gone up in the past 9 months (compared to same period in previous year). Does this mean more slippages are to follow? I had seen their stressed assets last year and noticed it was 6% of total assets. It came down from 7% in 2016 , but 6% is still high. if they dont manage this then expect more NPAs.

Another concern is that revenue from retail banking has come down. Retail is one of the strengths of this bank (for its size). CASA has also come down o 28% from 29% the previous year.

I mentioned Kedia because he reduced his holdings drastically, almost by half. This is huge. For a marquee investor who is hugely bullish on this bank it is surprising to see this kind of holding reduction.

I am in Karnataka for the long haul. I bought it with a time frame of >5 years. And I bought it an year ago. I am not in a hurry but I would be worried if bank does not show improvement in key parameters in the next 3-4 quarters.

1 Like

I understand your concern. I would recommend you to see the numbers of Gross NPA and Net NPA for FY18. It is coming down by .20 every quarter. As I mentioned earlier, the whole banking sector is reeling under pressure. I have looked into 38 banks. We would have to look at this bank for another year. Let us give the management some time. Now, BCG’s Saurabh Tripathi is running the transformation initiative for Karnataka Bank. We have to actually see what is changing in this year.

A few of the stressed accounts come from steel companies. These accounts will be cleared off in one year time. I find the first few outcomes of NCLT is very important for all the banks.

By March 2018, Karnataka Bank’s gross NPA will tend come below 3.85% and Net NPA to come around 2.65% - 2.70%. Let us wait for the March quarter on what they have to show us.

But other OPSB with similar fundamentals are trading at 2-3 times adjusted book value. So is it not this bank deserve at least 1.7 times ABV instead of 1.1 and hence trading at 50% discount?

Yes, you are right. This examples brings Grahamian learning to the forefront. A value pick remain idle for long time that you and I expect. We will have to watch how this bank is showing up in the subsequent quarters.

In my view, it is the investors’ conviction that matters. We do not have answers for all the questions about the bank. It is important for an investor to choose what is best for him after considering all the risks associated with his prospective investment.

3 Likes

With reference to their recent disclosure, the bank has opened close to 793 branches. I believe they have a strong potential to reach their target of 800 branches by March 2018.

1 Like

Hey. Could you throw some light on what attracted you to Karnataka bank amongst these 38 banks?

Other than price what, if any, factors do you feel signal that this is a good bet.

Thanks in advance.