Thanks and I read the footnotes however I wasn’t able to understand why a lender would take a haircut in case the business will remain as a going concern. In Q1 they made an EBIDTA of ~30 cr and in all likelihood they are going to make good money in entire FY23.

Because of 2 reasons broadly:

-

Standalone debt will be around 300 Cr and they are already defaulting on 250 Cr, given that the debt was structured couple of years back such that FY20 had bullet repayment of over 190 Cr. which obviously company was unable to service given its CFO and this bullet payment was postponed to FY22 which turned out to be a COVID hampered year. Now maybe even lenders have accepted that a sustainable solution will only be OTS because these debts have been outstanding over 7 years now and company will not be in a position to honor bullet repayment even in future.

-

Lenders are all ARC/NBFC even for standalone debt, they do take into consideration time value of money when structuring a deal. If they feel net net they will be well off doing a OTS where they either are expected to receive part payment upfront in cash and or part debt converting to equity as mentioned in notes.

I feel this is the only sustainable solution for standalone debt because these lenders are charging above 18% interest so on 300 Cr debt, interest payment comes out to be over 50 Cr annually, let alone the principle repayment component. Post OTS they can again enter banking channel with lower interest cost but all these will be possible if current lenders take some haircut, settles for longer repayment schedule, part conversion into equity etc.

2 Likes

Interesting announcement by the company- fund raising announced by the company yesterday wherein Rs.28.5 Cr each will be infused via warrants issued to promoters and alpha alternatives group @97/share- close to 22% of Market Cap.

Co. also proposed to issue NCD up to Rs.350 Cr in upcoming EGM.

This fund raising could be in line with earlier discussion around OTS/debt restructuring. More clarity will emerge only after getting further details of NCD investors and communication by the company.

4 Likes

Looks like the first ever credit report for the company, for the proposed NCD:

2 Likes

Kamat_Q3FY23_Result.pdf (4.9 MB)

Q3 result out. Excellent numbers.

Topline in Q3 is Rs.84 Cr vs Rs.62 Cr QoQ (36% growth) and Rs.51 Cr YoY (63% growth). The most recent best quarter in terms of sales was Q1FY23 (sales of Rs.69 Crores).

EBITDA in Q3 is Rs.33 Cr vs Rs.19 Cr QoQ and Rs.17 Cr YoY. The most recent best quarter in terms of EBITDA was Q1FY23 (EBITDA of Rs.29 Cr).

Interest cost reduced from Rs.13 Cr (Q2FY23) to Rs.6 Cr in this quarter because of various debt settlements done by the company.

1 Like

The notes to accounts in this results gives detailed insights on the long due balance sheet clean up. Some interesting points being:

-

In Q3, KHIL settled dues of two ARCs and 1 bank, difference between dues on books and settlement amount is 10 Cr accounted as exceptional items for this quarter

-

After Q3, KHIL settled dues of two remaining ARCs for 123 Cr (book value of debt 220 Cr). Impact of 97 Cr to reflect this will be reflected in Q4

-

Proposed sale of immovable property at Nagpur, 10 Cr gain on the books will be reflected in Q4

-

NCDs were used for settling debt of KHIL, a subsidiary co. and a JV co. and providing loan to a co. belonging to promoter

-

Co. signed term sheet for selling a hotel property (likely VITS Andheri), expecting completion in 12 months

-

OHPPL: Debt of IARC was 188 Cr on books, co. has settled the same at an amount of 142 Cr subsequent to the quarter, it will be reflected in Q4.

In summary, lenders took haircut of Rs.143 Cr (97 Cr on Standalone & 46 Cr on subsidiary) which is 50% of the market cap!

Remaining debt on the books will be only around 300 Cr NCD and proceeds of around 130 Cr expected from VITS, Andheri will go towards reducing that as per credit reports. Remaining 170 Cr debt looks sustainable at around 70 Cr EBIDA/CFO from remaining property.

7 Likes

The company has been able to raise around INR 297 crore through NCDs …growth on cards and last quarter was good …looks like a multibagger in making

2 Likes

Kamat hotel EPS 113 Rs (exceptional item and on way to deleverage fully) growing too, future looks bright as management is following up on actions promised, much undervalued still because of past and ongoing resoutions. Extract from notes - considering the revival of hospitality business, positive net worth as on 31st March, 2023, positive earnings before interest, taxes and depreciation (EBITDA) for the year ended 31st March, 2023 and year ended 31st March, 2022, increase in operations and profit during the current year, settlement of secured debts due to AR Cs, settlement of loan given to Subsidiary Company which was fully provided in earlier year, reversal of provision for diminution in value of investment in Subsidiary Company (OH PPL), signing of term sheet for proposed sale of one of the hotel properties, issue of NCDs and further developments as stated in note 3 to 8 of the statement, considering the future business prospects and the fair value of the assets of the Company being significantly higher than the borrowings I debts, these standalone results have been prepared on a going concern basis which contemplates realisation of

assets and settlement of liabilities in the normal course of Company’s business. https://www.bseindia.com/xml-data/corpfiling/AttachLive/96e25f85-8318-4f81-a626-00e5e38d7f9e.pdf

1 Like

Kamat reported decent operating performance:

- Q4FY23 consolidated topline of 80 Cr in vs 84 Cr QoQ and 46 Cr YoY- 74% growth ; EBITDA of 27 Cr vs 33 Cr QoQ and 13 Cr YoY ; OPM of 34% vs 40% QoQ and 29% YoY

- FY23 Consolidated topline of 295 Cr vs 145 Cr YoY ; EBITDA of 108 Cr vs 36 Cr YoY ; OPM of 37% vs 25% YoY ; CFO of 116 Cr vs 31 Cr

The notes to accounts & BS of FY23 gives detailed insights on the long due balance sheet clean up:

-

OHPPL settled book debt of Rs.188 Cr at Rs.142 Cr- No Due Certificate received

-

Consolidated Gross Debt now stands at Rs.328 Cr vs Rs.531 Cr YoY

-

Consolidated Cash Flow from Financing: Outflow of Rs.350 Cr long-term borrowing and Rs.62 Cr of interest(including other borrowings). Net repayment of Rs.350 Cr + 62 Cr – 302 Cr (NCD) – 12 Cr (Warrants) – 11 (Warrant conversion) – 11 Cr (Nagpur land) = 76 Cr from internal accruals.

-

Rs.1 Cr received as advance for sale of VITS, Andheri at around Rs.125 Cr.

Company also signed EY as their IR and released first press release:

6 Likes

The shareholding pattern for Kamat shows plegded shares at nearly 88 percent of promoters shares. Is this a normal occurrence for a business undergoing turnaround. Can we know how far back this pledge goes and what was the need for it. Also, does management has any plans to reduce the same going forward.

3 Likes

Management has delivered on growth promise by opening many properties, also have plan to reduce debt by half by q1 ,with this ESP for 24- 25 can cross 30 , will head to 4 digit in a year, hodling since lower levels and will continue to hold.

1 Like

@Rajesh_Singh how much of your portfolio is allocated here and whats average price of stock in your DMAT? This company came to my radar but promoter’s pledging is something that is off putting me for taking counter bet on this stock

It’s small allication 140 Rs average 3500 shares, pls go through previous posts, can go through mgt interview too clear plan of growth and debt reduction.

News of new hotel approval in Ayoddha is causing upper circuits.

But 98% pledging is not letting me enter at this level. It has already ran a lot. I feel all the news and earning expectation are already accounted in the current price.

Will wait for this quarters result.

1 Like

One of the main reason very few individual make money is that they make mechanical checklist like pledge share, debt equity and forget the narrative and future ahead. By the time everything will be fine it will have crossed 4 digit then mutual funds and mature investors ![]() will enter for 20% return. Investing is about foresight about what is going to unfold in future.

will enter for 20% return. Investing is about foresight about what is going to unfold in future.

5 Likes

Promoters have exercised their warrants @ Rs. 72.75 for 12.53 Lac shares (Rs. 24.25 was already paid in the past). So effectively promoters have received shares at Rs. 97 whereas the CMP is approx. 280.

The down side of the warrant conversion is that the EPS will come down and that some people may feel that the promoters have received a fantastic deal. On the upside the debt to equity ratio will improve and promoter’s stake has increased by ~4%, which may give confidence to other investors, so long as these shares are not off loaded in the open market.

Overall, this move is neutral as of now. Important to see how the company uses this equity infusion - to retire old debt or to expand capacity.

Disc: Invested since more than 1 year and presently holding.

2 Likes

Hi , any idea what terms will be modified in the board meeting addendum for the debentures? The refinancing was anyway planned for July’24 basis net cash position as mentioned in the con calls earlier

Thanks everyone for the wonderful insights, just took a small position in this, lets see how this works out, real kicker will come with NCD repayment in July 24

1 Like

The opportunity looks interesting with the management aiming to achieve INR 130Cr EBITDA in FY '25. With 190 Cr of Debt and INR 720 Cr Market Cap, that makes the valuation reasonably attractive at ~7.5x FY '25 EBITDA. However, there are a few questions I had, if anyone has had a chance to look at these :

-

Is the Orchid Hotel, Mumbai owned by the promoter entity Plaza Hotels Pvt Ltd (PHPL)? The company presentation says it is an ‘owned’ hotel but Plaza Hotels’ annual report says that it has been given for management and operation to KHIL and is owned by PHPL.

-

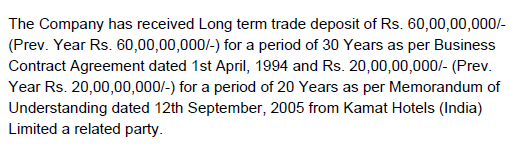

INR 80Cr of long-term trade deposits have been given by KHIL to PHPL interest-free. INR 60Cr was given for a period of 30 years in 1994 and INR 20 Cr was given for a period of 20 years in 2005. They should be up for renewal in 2024-25, if there has been any update on this.

-

KHIL paid INR 3.6 Cr of royalty expense to Plaza Hotels Pvt Ltd in FY '23, for the leasehold land. How are these payments determined? Are they based on a % of revenue or are these fixed payments each year?

-

22 Cr loan (from the NCDs raised in Jan '23) was given to Plaza Hotels Pvt Ltd by KHIL. KHIL received an interest of INR 80L on this in FY '23. It is unclear why the loan was given and what is the rate of interest being paid to KHIL by promoter entity (PHPL).

- Contingent liabilities: As per clause 45.3 of FY '23 AR, there are INR 60 Cr of contingent liabilities relating to a tax demand which have not been provided for. Couldn’t find much details about the tax demand.

I’ve also posed these questions to the IR. Awaiting their response, but it will be helpful if anyone has already spent time on this diligence.

5 Likes