Latest reports appear reasonable but market giving thumb down. Why?

Weak results from company. Although sales increase from 474Cr to 504Cr (YoY), PBT dropped from 85 Cr to 71Cr. Looks like pain in FMCG sector is affecting most of the companies.

this is definitely not a piece of good news for the investment community …and its always a dilemma favoring own blood vs professionals in family-managed biz !..

Yes, that coupled with the current market sentiment against companies with pledged share. Jyothy Lab has ~24% shares pledged.

They pay heavy dividend instead of clearing debt.most of the dividend goes to them which indicates that they are not ethical.

Jyothy Labs Q1 FY2020 Performance

- Consolidated net profit rises 11.61% to ₹37.38 Cr for this quarter.

- Operating Revenue was up by 2.2% at ₹422.5cr for the reported quarter.

- Operating EBIDTA margin for the quarter stood at 15.5% as against 13.7% in Q1FY19.

M P Ramachandran, Chairman & Managing Director, Jyothy Labs Ltd said, “We have started this year with a positive outlook in spite of severe drought. The first quarter of this year has witnessed consumption slowdown however we do expect that the coming quarters will accelerate the growth of the business. We have been focusing on innovations and product differentiation and we believe that this will have a long term benefit for us.”

https://www.bseindia.com/xml-data/corpfiling/AttachLive/49242f65-e80d-435e-939d-3431132d877f.pdf

Note: The company has changed its brand identity from Jyothy Laboratory to Jyothy Labs w.e.f. 11 July, 2019. It has also adapted a fresh logo. Expenses related to these two is included as an one-time Exceptional Item.

1 Like

Jyothy Labs also plans a geographical expansion of its fabric-care sub-brand ‘Ujala Crisp & Shine’. The sub-brand in the post-wash category is popular in Kerala and Tamil Nadu. The plan now is to extend it to West Bengal, Andhra Pradesh and Karnataka.

“We will look to take ‘Ujala Crisp & Shine’ national once it becomes a ₹100-120 crore proposition, say by around 2021; it was around ₹80 crore in FY19,” Kamath said.

I am puzzled. They said in their Annual Report 2008-09, that they’d already launched ‘Ujala Stiff & Shine’ all over India in 2008. This same brand later renamed to ‘Ujala Crisp & Shine’. Now they are talking about taking it to national again?

Three-four new launches may happen this year. Immediately on the cards is an extension of its popular soap ‘Margo’ brand into face-washes.

According to their Annual Report 2011-12, they already had face-washes after Henkel acquisition. I also saw it once in Flipkart.

So, are they relaunching these?

They also had a very good product portfolio of

- Men’s grooming in Fa.

- Maxo insect killer spray.

- Soap brands in Niki & Jeeva.

- Detergent brands like Chek, More Light.

& many more.

I wonder why they need to do anymore acquisitions, when they can relaunch & promote the current & dormant portfolios. Also, they can repay the debt with the surplus.

Also, their promising Laundry chain revenues are falling every year after hitting a high on FY2015-16.

@ranvir any inputs?

2 Likes

They take hefty salaries and hefty dividends through debt…And simply tell that they will be debt free.they are not shareholder friendly

Hi…

Other things aside, I have gone through their Q2 results. They look exceptionally strong.

If we look at their their volume growth ( around 8 pc ), its nothing short of miraculous, specially in this sluggish demand environment.

Seeing this, I have started buying the stock in small quantities and I intend to buy more as and when there is some fund availability.

I ve gone through their investor presentation twice. Except for their Household Insecticide business, most others look rosy. ( or promising at least )

Anyone any counter views???

Am I missing something ???

Rehards,

Ranvir

@ranvir I agree with you. I heard their q2 conf call. Home insecticide (HI) business is down. The rest grew strongly. HI is around 30%of their total business and that is affected by the agarbattis being dipped in Chinese imported pesticide and sold as a cheaper repellant. Apparently it’s very harmful for health of humans also. The HI industry is lobbying against it but there is no government action as yet although the tide seems to be turning.

With base effect coming into play from next quarter even HI will grow from a lower base.

I think jyothy labs will grow steadily.

My main concern is their new product pipeline and succession planning.

One of the earlier posts talked about ujala crisp and shine. That story has been talked about for a long time as a national rollout but nothing on the ground yet.

They are working on Margo brand extensions which may not move the needle much overall.

Rest of the products are not announced or too early.

Regards

Manish

I am atleast happy that Mr. Kamath said something which I desired to listen, that they will concentrate on extending their existing portfolio rather than acquisition, unless they find something at cheap price. They will do much better if they do that and also do the needful to increase national availability of their existing portfolio.

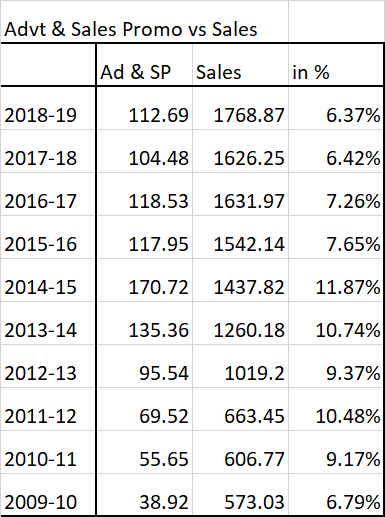

Also happy to see that Fabric Spa registered double digit growth YoY. This category although small has a huge market to cater, which is captured majorly by unorganized players, & has a tailwind owing to water shortage.

Plans are afoot to initiate discussions with banks for financing trade channels. Under the arrangement, banks will provide finances to channel partners against a letter of comfort issued by the company. These discussions, however, are likely to happen in FY-21 (next fiscal). Working capital constraint in channel partners has been a major issue for FMCG companies. “Bank -financing can be looked at. There is some liquidity crisis in trade channels especially with non-banking finance companies holding back on lending,” Kamath added.

Jyothy Labs operates on a cash and carry model; unlike some other FMCG companies who might extend credit to the trade or have a longer credit cycle.

2 Likes

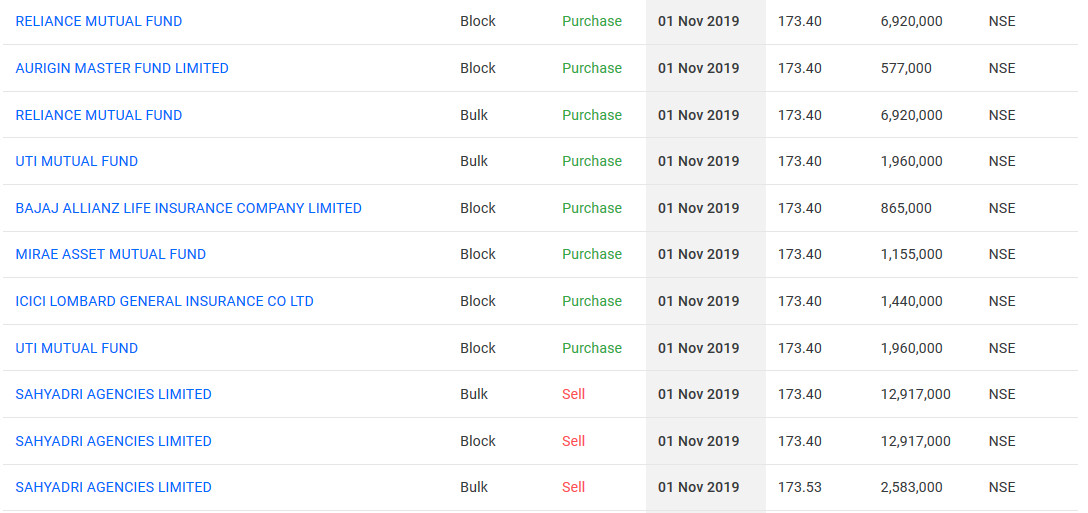

Looks like FT has started adding more to its kitty .

Promoters have sold more than 4 percent of shares.now the pledged shares have come down to 8.53% from around 25%.Debts have also reduced.deb to equity ratio around 0.2.by 2021 they will be debt free according to management.Reduction of debts and pledged shares should be good for the company and share holders.

1 Like

I was going through their past financials, and observed certain things which didn’t make sense to me:

- In 2015, they generated free cash of flow of 150 crs (10% of Sales) and they had this amazing opportunity to pay back the chunk of Long term debt but instead they issued 40 crs of NCD and paid only 1.89 crs of Debt.

- They paid dividends of 42.35 crs (including tax) and Invested 132 crs into mutual funds.

- In 2016, they generated free cash flow of 164.06. Currrent Investment value fell down to 83.44 crs from 192.01 crs though proceed from the sale of investment including profit is shown only as 21.36 crs. The dividend paid including tax was 174 crs (some amount from last year as well) thus leading to reduction in C & CE. They did pay the 116 crs premium on NCDs outstanding.

- Whatever happens, promoters make sure they get a good amount of dividend for themselves though I am not against it but better decisions can be made. Related Party company where promoter (MR Jyothy) holds a strong position, also receives a hefty dividend.

Would love to know more about the narrative here, how exactly they have been running the company in terms of handling the financials and can someone detail out the they way they are structuring their ESOPs ?

3 Likes

Its also interesting, that how in 2016 they have declared the premium + maturities of their NCDs of total 598 crs under other current liabilities so when you are going through the ratios on moneycontrol, at first glance you are highly impressed by the Debt/Equity ratio of 0.01 but in actual they have been operating on D/E of 0.7

This conforms from the fact that their ROA and ROE have a big difference, usually it doesn’t happen in low leverage companies.

Any veteran investor, can explain why their is a need to issue the NCD’s when capex is only in range of 14-15 % of the operating cash flow for year '14 to '16 (other than to generate dividends)

Cash Invested is in the range of 400 crs, which can serviced with a term loan.

Just trying to learn more.

2 Likes

Just a thought on Jyothy Labs…

Now that MHA has ordered opening up of shops without clearing the Malls to open up, also the paranoia of people in general to not visit AC shopping places for some time to come - this may end up being a big positive for JLL which was otherwise reeling under the pressure of Private labels from the likes of Reliance Retail, Big Bazar etc.

Great time for them to sell and solidify brands like - Pril, Exo, Henko etc.

Disc- Holding a small tracking position in JLL.

Regards,

Ranvir Dehal

3 Likes