Hitesh Sir, this was an excellent pick by you. Worth holding even after the recent run-up?

with green shots being visible in the company’s performance, any views on what will be the net impact of rupee depreciation on the company’s financials as it has lot of foreign currency loans.

Disc - Invested from 170 levels and scaling up investments

Company has definitely turned the corner on the margins front.What impressed me was the 30%+ kind of EBITDA they make in Pharma division.LSI business also showed a strong margin performance.Revenue growth should pick up in coming quarters.Moreover,JLS got 2 USFDA approvals in Q1,and expects some approvals every quarter.Radiopharma is another interesting segment.

Some news today: http://www.bseindia.com/xml-data/corpfiling/AttachLive/73E8CC0D_91C6_4FBF_8AAB_DF7FEB11ADC6_122247.pdf

Disc.: Invested.One of my top holdings

Jubilant has been showing some interesting price trends in the last couple of months - I tried looking at this company in detail: Here is my write-up:

Summary of the below write-up:

- Normalization of CMO (High positive impact)

- Growth and pricing in Radiopharma (Medium positive impact)

- New Generic molecule launches (Low positive impact)

- Life Sciences (Neutral – positive in Niacinamide is negated by Pyridine)

- Rupee depreciation – (Medium Negative impact)

Stock Story -

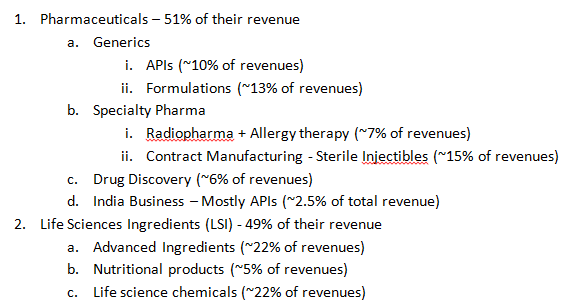

Jubilant is an integrated pharma company present in over 100 countries (incl Japan, China) covering a wide spectrum of the entire value chain in pharma industry – ranging from drug discovery to formulations business.

India business contributes ~27% of their topline. So the rest 73% is from their international operations.

Pharmaceuticals:

Generics(API + Formulations): Jubilant currently has 25 USFDA approved APIs/Formulations. Almost all of the molecules have very high competition. For instance 20/25 molecules have more than 12 players. In pharma whenever the competitive intensity is very high, generic companies usually don’t have pricing power. Even the recently approved molecule Zolmitriptan (Zomig) has 12 players. This molecule has a market size of ~ $100mn. Generics is NOT Jubilant’s forte. The attached spreadsheet has the complete list of their approved molecules.

Jubilant Life Sciences.xls (27 KB)

They have a total of 32 pending approvals from USFDA. – No Para IV filings – so even these filings may be competitive.

Speciality Pharma:

Radiopharma looks like the core strength of the company as it is a very complex field in medical chemistry and it has its own competitive advantages. The complexity of this business will create entry barriers. Jubilant has global leadership in the following products:

1. I-131 – Thyroid Cancer

2. MAA – Lung imaging

3. DTPA – Lung & Renal imaging

But this segment forms a very low % (~4-5%)of the overall revenues for the company. Hypothetically, even if this segment were to double in the next 1 year, Jubilant’s topline will grow only in low single digits. It is akin to having a lower allocation to a strong stock in a PF.

Contract Manufacturing:

Jubilant acquired Contract Manufacturing expertise through the acquisition of Holister and Draxis. They are one of the global leaders in Contract Manufacturing of Injectibles(among top 5 Contract Manufacturing injectibles in North America). Contracts in this business vertical are long term in nature and in some cases some of these contracts are multi-year contracts. Jubilant has 6 out of top 10 pharma majors as its customers. This is one of the stronger holds for Jubilant. But this segment suffered significantly due to USFDA warning letters for Spokane & Montreal facility. Management says Spokane operations have normalized now.

Life Sciences Ingredients(LSI):

Jubilant has global scale in producing the following:

- Acetyl

- Pyridine(raw material being Acetyl which is produced in-house)

- Pyridine derivatives

- Symtet (value added product) – 24,000 MT capacity

- Vitamin B3 – Niacinamide (value added product) – 10,000 MT capacity

Expenses as a % of total sales for this vertical has remained constant at approximately ~87%. So the cost advantage has not come from Jubilant Life Sciences vertical. This is a commoditized business with predictable business and as a result margins usually range around 15%.

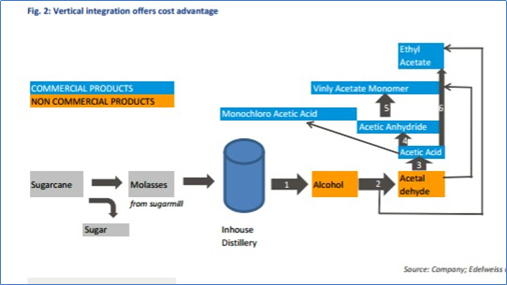

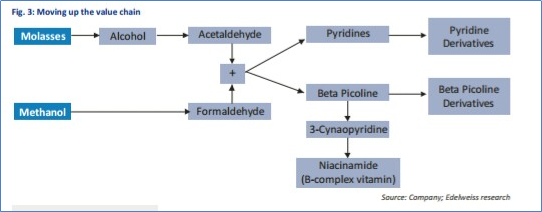

Company Produces Acetyl Inhouse:

Produced Acetyl is used to Manufacture Pyridines:

• In LSI vertical, the story is about operating leverage & Pricing Power as they have very large capacities in Pyridine & Niacinamide

• It is also about cost effectiveness – But Jubilant-LSI is already a cost effective player globally.

Methanol Prices have corrected significantly – lower oil being one of the culprits. Methanol is a key raw material for JLS.

http://www.platts.com/latest-news/petrochemicals/berlin/epca-european-methanol-to-stay-around-eur300mt-26229304

- Is there a Turnaround? –

-

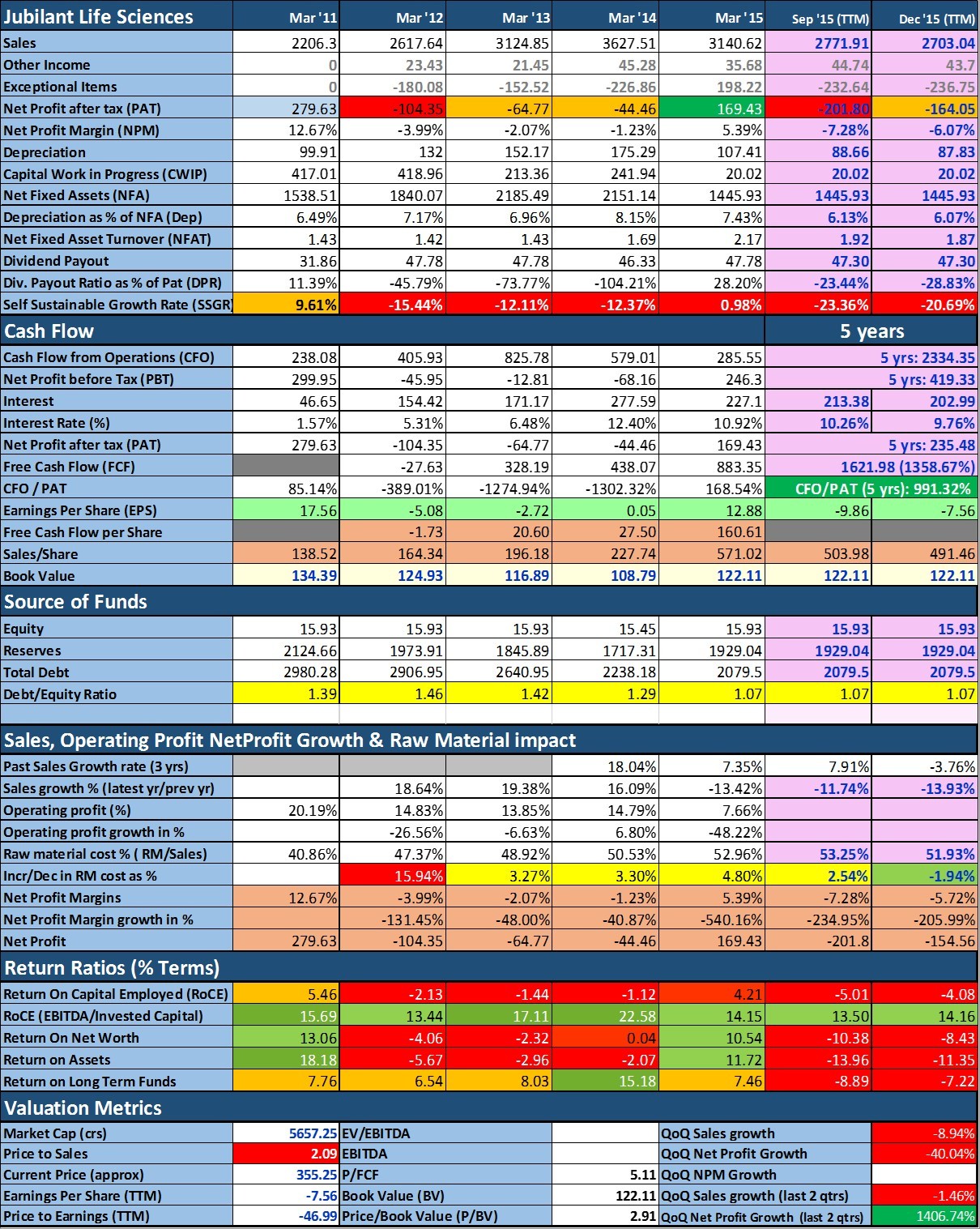

Lower Raw Material Prices: The top-line has remained flat, though the improvement has come mainly from higher EBITDA. This EBITDA improvement is only due to lower raw material costs + price increases. Wouldn’t all companies benefit from lower raw material costs? Positive

-

Would rupee depreciation benefit Jubilant? – Check the below #s:

Currently their dollar denominated debt stands at $445mn + Rupee denominated debt at 1951 crores. Expressed in rupee terms their total debt stands at Rs 4785 crores. Rupee has depreciated from 63.34(Q1 closing) to 65.53 on 30th September. Assuming that their debt levels remains constant they will have an MTM notional loss of ~ 84 crores. Will this be offset from increase in topline? ~73% of their revenues is dollar denominated, which is approximately $167.35mn. Assuming constant revenues as of Q1, their topline would improve by only 31 crores. negative

Note – I have assumed constant revenues because, Jubilant has not been a story of improving topline. Its actually about improving EBITDA & improving borrowing profile(dollar denominated debt to rupee loans). -

Management commentary on capacity utilization of the following facilities will be a key monitorable:

a. Niacinamide - Jubilant undertook a price increase of 10% for Niacinamide on June 16th for all its non-contract customers. positive

b. Pyridine – major market being china. There are lot of regulatory issues. So no meaningful improvement here. But the management says all the stress is already factored in. -

They have a reasonably big exposure towards Chinese markets. Slowdown + yuan depreciation negative

-

Montreal & Spokane operations have normalized(earlier they had a USFDA warning letter so this plant was operating sub-optimally) – big positive. Their contract manufacturing business suffered significantly due to this. Some of their customers walked out due to this. Management subtly says some new customers have come in.

Management Commentary on CMO Normalization:

“The production of the existing products goes on when the warning letter is there also.What stops is only the new product development. During that period,where the customers have alternate site,they would prefer to do in the alternate site, but they continue to remain customers.Only thing is,the additional orderflow was not getting generatedwhen the warning letter was there. So now that status has been changed.So customers know that the

site is okay for manufacturing, so the customers come back and that is why we say that normalization is underway.” -

Aripiprazole – I did not understand this part. Have they started supplying this API to Torrent/Alembic?

Jubilant is like a portfolio of 6-7 businesses. That is to me is a negative because gain from one business will be offset by under-performance in the other vertical(Positive Pharma versus Below par Life sciences).

It is like concentrated portfolio vs a diversified portfolio.

Having said that, even from the current levels Jubilant looks interesting(due to falling raw material prices, stronger Radiopharma & normalizing CMO) even after factoring in around Rs 50-60 crore MTM losses. Their debt levels is a cause of concern.

Thanks,

Ravi S

Disc - No position as of now.

10 Likes

Another decent quarter for company…

Though sales growth was missing, company did well to maintain the profitability momentum of previous quarter…

With half yearly EPS of 15 rupees & facilities back in compliance & 5 USFDA approvals in last three months which will eventually bring sales growth gives more power to its current rally.

At current price of Rs 400 & MCAP of 6400 Crores Jubilant looks undervalued.

A minimum PE of 20 ( though i believe even 25 is possible) with an expected yearly EPS of 30-32 gives a nice upside potential for 600-700 with limited downside…

1 Like

Jubilant plans to raise capital for about INR 1300 Crore.

Looking at how the stock had a massive fall on 18th Jan 2016 trading session, I was wondering:

-

What could be the possible reason that this particular one in the pharma sector has taken so much beating. As such there is no bad news ( like lincoln pharma’s ban in Tanzania)

-

If they are going to raise Rs 1300 cr, then they would also have to pay it back to the investors eventually.

-

As per the good write up from @ravimba31, they aren’t really competitive as most of the formulations and API’s are being done by other Pharma companies also.

Then in that case would Parnax labs be a better bet in selecting a pharma sector stock or jubilant is still better.

Cheers

It is hard to ascribe reasons for corrections in this market. Recent Yuan devaluation is a -ve for the company as China has a huge capacity in Pyridines. Will this -ve be offset by the following positives?

- Spokane hangover no more

- Better pharma performance

- Better Nicinamide performance

We will know more when the results are out. After the recent correction the stock’s risk reward looks interesting.

Thanks,

Ravi S

Disc: I have a 5% allocation here in my PF. Added in the recent correction. My views may be biased, please do your due-diligence.

1 Like

I think this is very positive news…

For Self Sustainable Growth rate see: Calculate Self Sustainable Growth Rate (SSGR) of a company - Dr Vijay Malik

Thanks for sharing. This was very helpful.

There is above 45% increase in EPS y-o-y March 2017 .

Q 4 is satisfactory along with Positive news that Motilal Oswal Mutual funds are invested in it

IDirect_JubilantLife_Q4FY17.pdf (459.6 KB)

http://www.bseindia.com/xml-data/corpfiling/AttachLive/7bf56b5c-97bb-4656-a5fb-3315efd7c8e0.pdf

excellent set of numbers… also Rakesh Jhunjhunwalal is holding this …

1 Like

Rakesh Jhunjhunwala exited as per latedt shareholding pattern

Management has mentioned about listing the co on Singapore Exchange in the 1st quarter of 2018. The funds raised will be used primarily for deleveraging. Does anyone know of any developments in this regard? Thx in advance. Disc-Invested.

From recent disclosures it appears that IPO process has started. Management clarified during Q1FY18 concall that Jubilant Pharma passed resolution on 23Jul2018 to raise capital by way of an IPO only and max.equity dilution will be 20%.Also, Julilant Life will offer 5% equity of JPL for sale.

My querry to senior members is weather there will be reserved quota for minority shareholders of Jubilant Life in proposed IPO of Jubilant Pharma?

Jubilant Pharma is in niche category of high margin Radiopharmaceuticals that are used in Nuclear Medicine, for the diagnosis, treatment and monitoring of disease and prospects looks promising.

1 Like

This was my first post and sorry for not disclosing…I’m Invested with 10% holding in Jubilant Life.

Government raises ethanol price for blending in petrol by 25%…

Jubilant is fourth largest supplier of ethanol to OMCs…any rough calculation how much it’ll add to bottomline ?

Disc: Invested.

@ORION, according to capitaline, Jubilant consumes a lot of Alcohol (Ethanol). As per the 2015 data, they consumed 456 crores of Alcohol and 101 crores of molasses. Are you sure that Ethanol Blending will really benefit them significantly.

PS - this is just a cursory post. I haven’t studied the company in detail.