Rishi…gov proposed further reduction in bt cotton prices from 800 to 740 for 450 gm packet. Revenue hit per packet will be 50 inr as 10 inr is reduction of royalty payments to Mosanto. JK’s bt business would be hit if this is implemented. Check below article.

Good that Ethiopia doesn’t have price caps yet.

Any insights on how they are planning to ramp up operation in India on veggie front? Their annual reports do not contain much info.

Vikrampati Singhania has been appointed Managing Director with a remuneration of ₹37 lakh per month, i.e. ₹4.5 crore a year. Over and above, various perquisites and commission of 2% of net profit.

Given JKAgri’s PAT was ₹12 crores in FY18, isn’t this too high? Also, this has been a new position created, so this is incremental expenses.

Another way to look at this is why would someone like Vikrampati Singhania resign from the directorship of JK Tyre and take up full time MD role in such a small company in the JK group.

He resigned from JK Tyres in January 2016 (he was a Deputy MD there), and was appointed MD of JKAgri in May 2018. Surely, resignation from JK Tyres wasn’t because he wanted to take up full time MD role in JK Agri, but it was for JK Fenner.

Moreover, he got INR 15 cr from JK Tyre for FY16 (however, INR 13.35 cr as commission). This sounds brilliant for such a profit making company. Fixed is low, commission is high.

For JK Fenner (in FY17), his fixed was INR 4 cr and a commission of INR 2.7 cr. JK Fenner had a PAT of INR 57 cr in FY17.

Coming to JK Agri, his fixed is INR 4.5 cr for a PAT in FY18 of INR 12 cr.

He directly holds very less number of shares in the company, but other members of Singhania family and indirect holding through Florence Investech, Bengal and Assam company, Hari Shankar Singhania Holding Pvt Limited is huge. In any case, I would be in favour of him taking higher commission based on profits and higher # shares, rather than such a high fixed component and various perquisites.

By the way, can someone please shed light on what Companies Act caps on the remuneration of MDs? I can see that it’s 5% of profits, hence not able to digest this news.

It is 5% of net profit and total director remuneration cannot be more than 11% in total. To go beyond this level, exceptional approval from the government is required. (I don’t know which authority provides the approval)

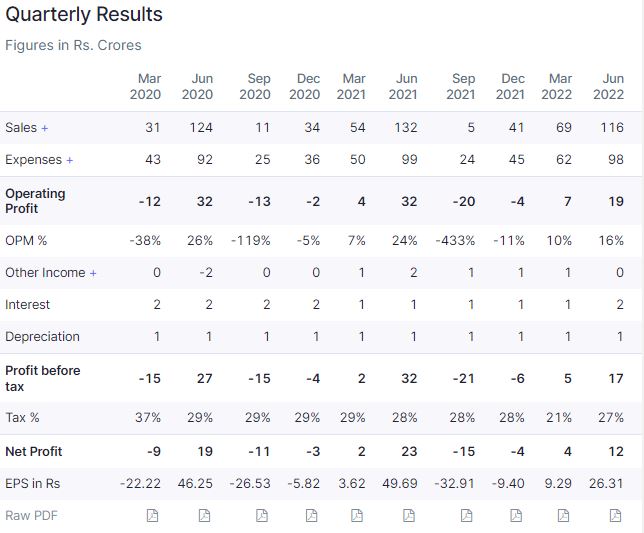

Is anyone still tracking this stock? Posted the worst results in years. Prima facie seems a hope story with bad working capital cycle and negative margins. Is there something to look forward to?

This stock is down by over 50% in the last 5-6 months. Major trigger for decline was poor Q1 results, much below what was expected. Q2 and Q3 are anyways bad quarters for this sector.

They had been foraying into vegetable seed segment to diversify their H2 earnings and entering into the African markets. Does anyone have any clue if the operations at Ethiopia started? By when will they start realizing revenues from that geography?

I believe this might go further down after Q3 results but should be good to pick up at lower levels post that.

Disclaimer: invested, forms 10% of my portfolio at current levels

Q3FY19 results:

Decent results I would say.

13% increase in sales YoY

Net loss at 5.2cr, compared with 6.3cr in Q3FY18

Inventory built up at 4cr this quarter compared with 18cr in Q3FY18

Pain point is the increasing Finance cost, but probably debt raised for expansion into African countries and vegetable seeds perhaps?

Guess Q4 will reflect vegetable seeds revenues and then Q1 will have Ethiopia numbers. Though stock is down 60%+ from its highs, these levels look attractive to add gradually.

Any opinion?

Disclaimer: invested, forms 7% of my portfolio at current levels, no new additions in last 6 months

Really wonder how long this company stock price can remain in over-hyped zone! Last 5 years , there’s no significant development. The numbers are not exciting.There’s no new technology coming, no management change (except the MD who does not know agriculture) ,R & D is not able to give any blockbuster hybrids!

Being in agri business for last many years, have never found anything great about this company.

Decent valuation should be around 12-15 PE if we take the past performance into account (it was trading between 12-15 PE for years before the 2017 bull run started. )

Seems few investors are stuck and are hoping against the hope,

In the best case scenario, even if the new MD wants to bring a change he would need to hire a talented agri -team and again that would be a hit on already thin bottom-line and revival may take years.

anyone tracking this stock?? Reported net loss of 3.78 cr against 5.20 cr in last quarter. The stock it trading at 420 right now dose it provide a good entry point considering the company is planning to raise funds through equity and convertible warrants. Considering the company has very low float and about 90% with promoter (including family members) looks like a logical move.

"The government has allowed the cultivation of two varieties of BT cotton in the country after passing the examination. Agriculture Minister Mr. Abdur Razzak hopes that when the cultivation of these cotton varieties begins, the country’s cotton production can be increased from the current two lakh bales to 15 lakh bales.

In 1996, BT cotton was first cultivated in the world, and neighboring India began cultivating BT cotton in 2002. In Bangladesh, following the guidelines of Biosafety, all senior correspondents have opened BT cotton for cultivation.

After completing the research work, the National Committee on Biosafety (NCB) approved the release of two varieties developed by the Indian company J.K. Agri-Genetics Limited for cultivation in Bangladesh. These are J.K.C. H 1947 BT and J.K.C. H 1950 BT."