Numbers are bad yet again +2% sales YoY. EBITDA down 17% YoY. PAT down 24% YoY. Stock look set to correct more!

Results are out for Q2…

Sales increase YoY for Q2 13.9 %…

PAT increase YoY for Q2 46.4%

EPS increase YoY for Q2 46.6%

Sales increase QoQ this year 28.6%

EPS increase QoQ this year 158 %

Thanks,

Vinaya

1 Like

company’s sales cross 100cr for the first time.

Jenburkt Pharmaceuticals has announced buyback of shares at a price of Rs. 576.

1 Like

As per exchange filing promoters are not going to participate in buyback.

Can someone workout probable acceptance ratio for retail investors(<2 Lac holding).

One observation to note is buyback declared after bad Q1 results.

1 Like

Kamlesh, I did some analysis (pradeepkanwar.wordpress.com/2017/10/02/jenburkht-pharma-buyback/). In short it looks like the payoff are better for non-retail customers.

Any one still track this ? June Q1 results are out , company has shown profit in Q1 vs loss in same quarter last year and a decent revenue growth.

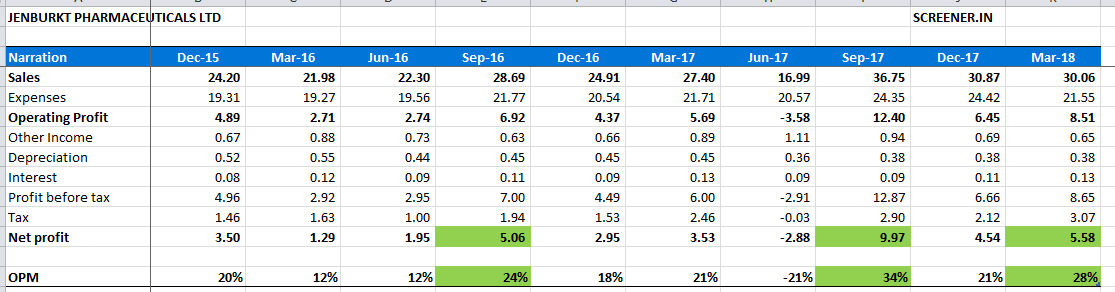

I was checking on screener and it seems that the Sep Q2 results are highest and forms more than 40% of total annual PAT. Any reason for this cyclicality in thier business ? why do they make more profit and margins in Sep quarter compared to other three quarters.

Hi,

I am tracking the company. See below my note on it.

Investment Thesis

- Jenburkt Pharma is an INR 240cr branded generic pharma company, with >85% revenues coming from domestic sales. It is effectively a play on domestic pharma, that over the past decade has grown at >10% CAGR and is likely to continue to do so backed by many tailwinds for the industry.

- While there are many different business models in the domestic pharma industry, Jenburkt in our view is best classified as an “Access Drivers” player (refer to later sections of the report for more information).

- Jenburkt’s key strengths - strong product portfolio, robust distribution and brand recognition – makes it a strong competitor among its “Access Drivers” peers.

- Jenburkt’s key moats are 1) brand’s quality perception (determined based on our channel checks with specialist doctors and pharmacists) 2) strong distribution channel spanning across tier I to tier IV cities and 3) new product launches on a regular basis to extend key popular brands (via new dosage forms and drug combinations) and strengthen its portfolio in fast growing therapies.

o As an example, current focus for Jenburkt is the dermatology segment where it has launched new products.

o Leading industry consultant, IQVIA (previously IMS Health), has further reaffirmed dermatology as a key growth area for Jenburkt. - With a strong track record of successfully launching new products and brand promotion, Jenburkt has consistently milked its distribution channel well, posting 12-15% revenue CAGR over the past decade.

- Its measured growth approach funded fully through internal accruals, coupled with 25%+ ROEs enables it to generate strong FCF that has been distributed consistently to shareholders through dividends and buyback.

- We think it is a hidden gem due to its low liquidity and BSE only listing.

- Its attractive valuation at 11x TTM PE (adjusted for cash), growth prospects and FCF yield, makes it an ideal candidate for compounding 15-20% IRR over the medium-term to long-term holding period.

Detailed report: Note on Jenburkt Pharma.pdf (321.9 KB)

Disclaimer: The above note is just for discussion purposes and is not meant to be a recommendation or an investment advice. Note that I have vested interest in the stock.

11 Likes

I am a doctor. To tell you the truth I have never heard of these brands… we will have to see if there is some regional brand recall. Hitesh sir is dermatologist. He can provide better perspective

1 Like

Thanks sta for your comment. If I may ask, which region are you from? I am from Dahod, Gujarat, which has become a big medical hub due to strong inflow of patients from the borders of MP and Rajasthan and my channel checks here have shown good recall for Jenburkt’s brands.

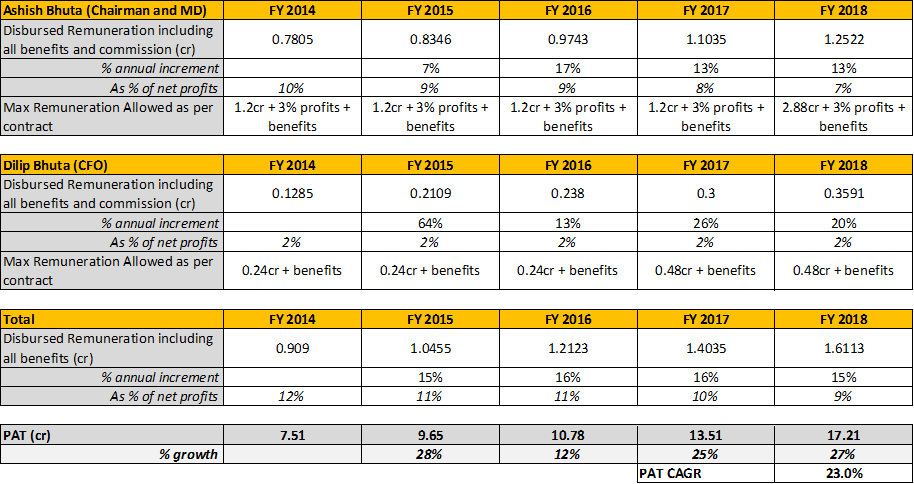

Thanks for the note. What about high managerial remuneration… Have you checked that?

Hi cabunny,

Thank you for your comment.

- While the promoter remuneration is high, over time it has been coming down in terms of % of net profits as the increment in remuneration has been in 15-16% range vs PAT growth of about 23% during FY15-FY18.

- Also, in case you are referring to the approved salary, note that the actual disbursed salary has been lower than the approved salary as per the service contract.

2 Likes

That probably explains it. My checks show that Jenburkt’s distribution network is skewed towards Western and Central regions so the likes of Gujarat, Maharashtra, MP…

I read some of Hitesh sir’s earlier comments on this topic. He seems to know Jenburkt. His earlier posts as per my understanding say that he preferred Ajanta over Jenburkt due to higher growth prospects of the former but is tempted to consider Jenburkt as well. It would be great to hear his current views.

1 Like

Jenburkt does have presence in the products mentioned in the report prepared by you and I can vouch for their products in dermatology segment which is my speciality. But I think more of their focus is to address the general practitioners and promote their products to them and thus they get a wider audience instead of catering only to dermatologists. Plus this promotion can be bundled with other GP products by the same MR.

I do get ocassional visits from them to promote their products like some antifungals some time back but there is no regular follow up from their MRs. But the reason as I said before could be higher focus on GPs.

The company has been very consistent in reporting slow but steady growth and seems interesting in view of the recent correction. What is amazing in the consistent improvement in margins since past many years and every year without fail they increase their margins. Hence even if topline growth is a tepid 10-12%, bottomline keeps growing at much higher rates.

At some point of time they will reach peak margins and post that profit growth will mirror sales growth and that can be a concern.

6 Likes

Thank you @hitesh2710 for your comprehensive response. Very helpful. As an “Access Player”, Jenburkt does rely on strong distribution across GPs and specialists. My checks with ENT, Ortho and Neuro specialists, in particular, show good response for Jenburkt’s brands. Within Derma specialists, you are right, I have not seen strong enthusiasm but management seems to be increasingly focus on Derma recently with new product launches which hopefully will be accompanied by sales force aggression.

In terms of return expectations, given Expected IRRs are a function of Probability of Upside/Downside and Magnitude of Upside/Downside, Jenburkt is one of those ideas where one is relying more on the high conviction/probability component than the magnitude. For me, if Jenburkt can do 10-12% topline growth which then could translate into 12% earnings growth with some scale benefits, add to it 3-4% FCFE yield, I am looking to compound 15% and above returns over the long-term. Current valuations suggest some further upside potential from multiple re-rating but not relying on it. When I think of portfolio construction, I think of two buckets: 1) High Conviction Steady Growth Compounders 2) High Risk High Return Plays. Jenburkt seems to be a good fit for the first bucket.

2 Likes

@anki.cool

Thanks for the detailed report.

My concerns are a bit similar to Hiteshbhai.

While you expect sales growth to be in the 10-12% citing industry growth,

- Can you elaborate why you think it will continue to maintain a 25%+ ROE?

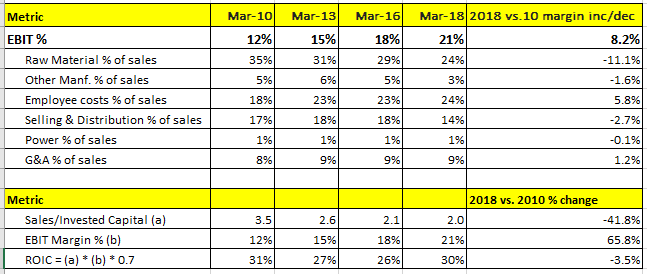

- Their EBIT margins went from ~10% in 2010 to 15% in 2014-15 and currently trend at ~20%. Are these sustainable? As seen in the table below, almost all of margin expansion was lead by decrease in % raw material. Can you help me understand why it happened and your view on margins in future?

Good questions @shahyash7.

Please see my responses below:

1. Can you elaborate why you think it will continue to maintain a 25%+ ROE?

Jenburkt has an asset light business model with 60-80% (varies year by year) of its product manufacturing outsourced. If you look at its gross fixed assets they have stayed almost constant over the past few years and net fixed assets have only declined with depreciation. While the Working Capital has been somewhat volatile, it has been pretty rangebound (as % of sales) over the longer term. Recently, working capital has stretched a bit and a reversion to the mean would further help. So, going by the capital employed in operations (Fixed assets + WC), one could expect the sales turnover to improve. Assuming profit margins stay constant (more on this in my answer to the 2nd part of your question), core operational ROE should only improve. Of course, the caveat here is Jenburkt throws lot of CF which accumulates on the balance sheet, increasing total assets and equity and with ROA and ROE > growth, overall ROA and ROE over time could decline. Hopefully, with healthy dividend payout and intermittent buybacks, balance sheet size and cash accumulation should remain in check and not dilute overall ROE.

2. Their EBIT margins went from ~10% in 2010 to 15% in 2014-15 and currently trend at ~20%. Are these sustainable? As seen in the table below, almost all of margin expansion was lead by decrease in % raw material. Can you help me understand why it happened and your view on margins in future?

According to me, current margin levels are sustainable as the margin expansion has been driven by 3 key structural factors:

- Pricing Power: Jenburkt’s brands have a strong quality perception which coupled with its robust distribution, ensures good pricing power with customers. On the other hand, highly commoditized nature of its raw materials/finished goods and highly competitive supplier network ensures that Jenburkt’s bargaining power is favorable with the suppliers.

- Improving Product Mix: Jenburkt has been good at launching new products around its existing brands with introduction of higher margin new dosage forms and new formulations. Refer to the new product launches table in my report.

- Scale Benefits: With steady sales growth, some scale benefits further help the margins.

Going forward, I think it is reasonable to say that Jenburkt can at least sustain current margin levels and hopefully improve with above structural trends still intact, although the pace of margin improvement would likely be slower given the higher base now.

3 Likes

@anki.cool Why do u think Q1has been weak for jenburkt historically. And regards of the pan India presence I don’t see any of their reps visiting us down south and the brands are not well known as well.

Jenburkt’s domestic is predominantly acute heavy portfolio. This kind of portfolio will have seasonal variations unlike chronic heavy portfolio which most other companies have and those who dont have aspire to have.

Traditionally March to June is usually healthy season with very few throat etc infections. At most there will be the diarrhoea/vomitting cases some of which might be due to gastroenteritis.

As a rule of thumb in Western India, the season of marriage i.e months around May and December are considered to be healthy seasons. People have a good time enjoying marriages and nobody is bothered about getting sick.

4 Likes

@hitesh2710 - Thank you for your insights on seasonality.

@Prasadkumaresan - Thank you for your comment.

In regards to distribution, since this comment has been raised earlier too, I have put together a list of possible reasons below on why people may not have come across Jenburkt’s brand.

-

Jenburkt has no substantial OTC or consumer products. Accordingly, they rarely do any mass marketing. Their marketing is targeted towards select doctors and chemists. Unless someone is either of the two or has done targeted channel checks with these people, it is unlikely they would know about Jenburkt’s brand. Also, Jenburkt does not have any mega-brands such as the likes of Glycomet where one brand alone does sales of 600cr+ and pretty much be found on any diabetic patient’s prescription. As an “Access Player”, Jenburkt rather relies on a diversified portfolio of a few decent brands and is a small company with just 120cr TTM sales.

-

Even if one is a doctor or chemist, there are over 10 lakh registered doctors as per Medical Council of India and over 9 lakh chemists in India. Jenburkt claims that its distribution reaches 75,000 doctors and 50,000 chemists, suggesting <10% probability of anyone from these community knowing about Jenburkt.

-

Jenburkt’s distribution is skewed towards Western and Central regions, as mentioned in my report as well as in an earlier post.

1 Like