JB Chemicals & Pharmaceuticals Ltd has informed BSE that the Compensation Committee of the Board of Directors of the company has, on January 06, 2014, issued and allotted 19,825 equity shares of face value of Rs. 2 each (10,500 shares at a premium of Rs. 82 per share and 9,325 shares at a premium of Rs. 93 per share) to certain employees against the exercise of options granted to them pursuant to Employees Stock Option Scheme of the Company.

The issued and paid up capital has thus gone up from 8,47,11,800 equity shares of Rs. 2 each to 8,47,31,625 equity shares of Rs. 2 each.

JB CHEM has come out with encouraging results for q3 fy 14.

On first view there is loss because they have decided to take the hit of around 64 crores which was the settlement amount with cilag in relation to release of funds from escrow account.

Without the extraordinaries.. results according to details given in press release are as follows

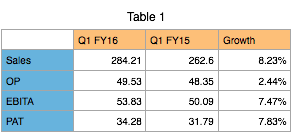

period

q3 fy 14

q3 fy 13

9M fy 14

9M fy 13

sales

234

200

710

596

PBT

48

31

116

85

PAT

30

21.9

83.7

65

eps

3.54

2.58

9.88

7.67

OS

8.47 cr

OS is outstanding shares.

Reported earnings shows a loss of 6.47 crores bcos of extraordinary item of 64 crores.

Overall its outstanding results if one neglects the one off item of 64 crores.

The theme of margin improvement is definitely playing out along with good sales growth.

The press release given seperately gives a lot of details.

I think if there is any sharp dip due to one time reported item, one can consider buying jb chem with a view of around 2-3 years.

JB chemical has posted loss of 6.47 crs due to settlement with Cilag. JB/ Cilag has agreed to settle this case by reducing the OTC sale amount by 64.5 crs.

If this exceptional item is excluded then results are quite good, Operating income up 17% YoY, PBT up by 54% YoY , PAT up 38. 18% yoY.

Seniors here, how do you see this results esp the case settlement thing?

Hitesh bhai,this settlement may also be a positive since such matters consume a lot of time of the management & now they would be able to focus better,possibly.Btw,have you checked the IndiaNivesh report on JBCPL? Their estimates were bang-on.

And…Always good to see you giving a thumbs-up.

Disc.: Recently invested.

Company has clearified on bse about the one time settlement of 64.5Cr to be reflected in the Dec 13 qtrly results instead of re-opening of earlier accounts.

This is what you mentioned while initiating the post…

“Looks like a low risk high return kind of scenario for the patient investor bcos once the company gets its act together post selling the Russian-CIS OTC business, there could be a strong appetite for the stock even as a growth stock.”

What a market insight you have!!..This can very well turn out to be true and company might be on growth trajectory now that the entire pharma ind. is slated to grow in double digit.

The company seems to be on right path of getting its act together.

The company is available at a forward PE of 12 with cash on books. The downside is limited while we can have an upside of more than 20-30 percent. the company has given guidance of increasing capacities which will drive growth.

Disclosure Planning to add

Hi all it seems very interesting company and value buy as per graham value buy criteria and also management is very conservative and very honest as per their guidelines.

in last AR they mentioned that there sales is equal to that of before selling of OTC business. and to make this happen only 3 years required.

No significant improvement seen from the CIS business being the main component of over 50% exports. The domestic sales are providing moderate growth driven mainly by Rantac and Metrogyl. Any further triggers seen? @hitesh2710

Nevertheless, one of the highest dividend paying company in my portfolio.

yup the dividend is fantastic.

the prob with the company is they do not communicate properly. no con call. even in the annual report the havent spelled out future plan in its entirety. unless the company talks more, the market will always be suspicious. lets see how the USFDA pans out.

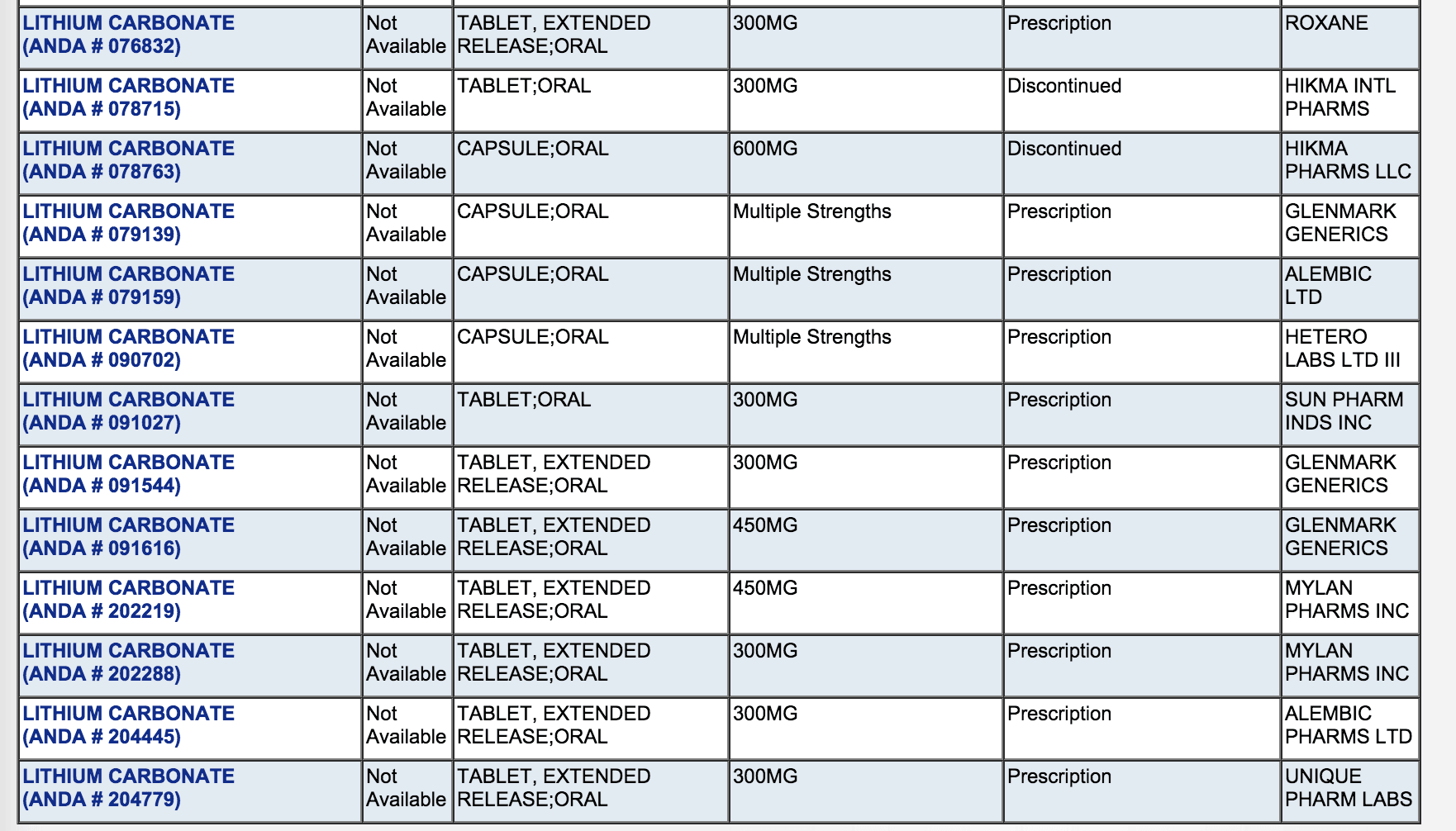

An further release to the BSE from the company reveals more information on the USFDA approval link

Recently, the US FDA approved ANDA for Lithium carbonate

extended-release tablets USP 300mg. The company plans to commercialize

this product in Q4 of this year. Sun Pharma seems to be the have the other share of pie here. Moreover, there are 4 other ANDA’s pending for approval. Does anyone have any indication on the market size of the Lithium carbonate USP 300 mg in the US? What is the potential that is behind?

Neverthless, the drag came from the exports to Russia-CIS market which declined to Rs.11.34 crore

If you study the Annual report, there are 2 red flags on this company. a) The number of related party transactions is simply mind boggling; b) The company is suffering from Russian Ruble depreciation but continues to invest in Russia in hope of longer term benefits (taking a call on oil prices??) c) The company hedges exposure through derivatives in USD (many a companies have been doomed in the past in this effort. Extreme discipline is required to refrain from speculation) and d) The management compensation is nearly 9% of PBT!!