Solar is an area with hardly any entry barriers. Most of the player just import panel and assemble it…same would be the case for Suzlon. If this hybrid model makes sense then even competitors like Inox etc will start doing…what stops them?

I agree that Suzlon might be the early one to adopt the hybrid model and that should give them benefit for sometime.

4 Likes

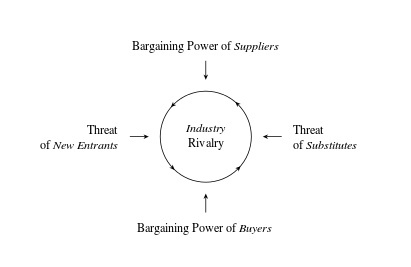

Mortar forces for Strategy

Does Suzlon has threat from new entrants? ----> Yes

Does there is a threat of substitutes ? —> Yes, Gas, Coal Gas, Biomass, Hydro and Fossils

Does Suppliers have bargaining powers? Suzlon make their own wind turbines. But this is less of an issue.

Does Buyer have bargaining power ? —> Yes. Buyer of power could pick and choose the lowest cost of power producer. They do not really care if it is coal or Hybrid renewables

The only competitive moat in this case could be the low cost of production or entry barriers or regulatory tailwinds? – This does not look to be the case for Suzlon.

They may get scale due to govt push for renewable but whether that could results in better margins and ROE is still not clear.

Cheers,

Amit

3 Likes

All the other WTG makers get their technology from European companies…europe has high wind speed and less solar energy. Whereas india has not so high wind speed and plenty of sunlight.

Among its compititors, only Suzlon has a focussed R&D program geared towards wind solar hybrid. And here Suzlon has an early mover advantage.

The second advantage that Suzlon has is very high installed capacity which enables it to ramp up its production to meet the increasing demand.

The third advantage that Suzlon has is the geographical spread of its manufacturing facilities. As the rotor diameter gets larger and larger, it is difficult to transport the blades to remote lications given the twisting and turning nature of roads.

The fourth advantage that Suzlin has in repowering its old sites and its relations with existing clients.

I am only talking about the advantages of suzlon…not about the moat. These advantages would benefit the company over the next 2-3 years. Its enough time for Suzlon company to aggresively deal with debt and more than enough time for suzlon stock to trade at a much higher level.

The next issue is coal vs renewable power. As Mr Tanti has been saying, renewable is no longer the alternate power but now its the mainstream thing. If the wind solar hybrid (which may show drastic improvement in next few years)…can become on par with coal, then i dont think thermal will be the preferred option anymore. Wind solar then becomes the next big thing in energy …and those invested in the biggest company in india and one which has good global presence and standing…would eventually stand to benefit quite a bit.

If investing is about making money, then suzlon @17.40 presents a good opportunity for investors. Its a story which has not yet started.

5 Likes

Mine is more of a sectoral call. Those who want to play it safe can opt for investing in Inox wind…which has low debt, low p/e…and its now started its uptrend.

Why do you need wind if solar is abundant in India.

Text taken from below article.

Tesla is building a $5 billion “Gigafactory” in the Nevada desert, which produces batteries than can be used to store solar energy.

It has acted to help solve an energy crisis at least once before. Last year, the company built an 80MWh battery farm in 90 days after a gas peaking plant near Los Angeles leaked tonnes of methane and had to be closed.

Now, the question is the cost of production would only come down if we have better storage capacity. Tesla is addressing this gap. The only thing we need to do is tap the solar energy. Wind Energy holds little promise due to inconsistent and low wind patterns in India. Hybrid could solve some of the issue with better PLF but the cost of production is still higher due to storage/tapping of the energy.

With better storage products like Tesla battery which will be large scale production, many solar players could dominate the renewable industry. There is no competitive strength so to speak from Suzlon. They can only clean there debt with consistent strong growth and with little return for minority shareholder with such large equity base. We still do not have a bull case for Suzlon although it is the largest player in India. Suzlon definitely continues to have better export market than domestic market as wind is abundant in many parts of the world with onshore and offshore wind farms gaining popularity. For ex: Australia. Too much wind all day and night long. For me, the big play in Suzlon is how much markets share they may gain in export markets but that may require some debt funding. From past experience, Tanti ji ran into debt woes.

3 Likes

In all the pre budget expectations from the govt, Mr Tanti asked for various subsidies. When the industry is too competitive and the whole business model is around subsidy then investment begs a question.

http://www.suzlon.com/blog/budget_expectations

Wish list from Suzlon boss from Govt

- Continuation of Accelerated Depreciation & Section 80 IA for WOEGs

- Incentive mechanism for State DISCOMs to procure wind energy

- “Zero” rate GST for Wind Operated Electricity Generators (WOEGs)

- Concessional finance/interest subvention for manufacturing sector that invests in wind energy for captive utilisation

- Export subsidy (logistics support) for wind energy sector

- Exempt raw materials from customs duties and implement higher tariff for import of finished goods.

At the moment, renewable energy products are exempted from excise. Electricity duty is not included in the proposed GST framework which can lead to increased cost of production of wind energy.

2 Likes

Thanks aammiitt2 for posting balanced views among flood of bullish messages.

1 Like

I am just curious, When it comes to solar power, what about the land availability. If anyone can give more details on this, it will be very useful.

The one data I had seen earlier was you will need close 4~5 acres for 3MW of solar power.

If we are talking about 20GW of solar power, what will be the land requirement?

For a country like India, where land for agriculture itself is less, can we afford to allocate so much and for solar? A thermal or gas based power plants can produce double the power at 1/10 the land requirement.

1 Like

Prasth,

I don’t think land is a constraint. Agriculture requires cultivable land

hence it’s scare … there is no specific requirement for solar pp …

comparing power plants based on land requirement should never be the

criteria

What is important is radiation levels of the region which determine the

amount of the energy that can be produced

Not so fast. Significant investment in Smart grids & storage technology is needed to solve grid integration problems (assuming all the grid integration problems can be addressed).

Disclosure: Invested in Inox Wind.

1 Like

I am again reproducing excerpts from the interview of Mr Tulsi Tanti…

What’s your outlook on the sector globally and in India?

I think globally this sector has been growing very positively in the last 2-3 years. In 2016, the world has seen an investment of $500 billion in the power sector. Out of that, $330 billion investment has come exclusively in renewable energy– 50 percent wind and 50 percent solar. So this means 62 percent new investment in the global market, including India, is flowing through the renewable energy space. So that shows that now it’s mainstream and not just an alternate energy source. The total investment in the power sector will be almost $10 trillion by 2035. Out of that, the current forecast is that $6 trillion will come into solar - that’s 60 percent. It’s achievable because 2015 has delivered and this momentum will continue in the global market. Now coming to India, our prime minister has announced initiatives for renewable energy and a target of 175 gigawatts by 2022. In 2014, $2.5 billion investment has come into the renewable space in India. And in 2015, that number stood at $5 billion, that’s 100 percent growth. In 2016, $10 billion worth of investment has flowed in. So again 100 percent growth. So in the last two years, we have seen 100 percent growth. So it’s moving well and the (renewable) sector is taking a very strong position in the power sector.

In the next five years India is set to add around 32000 mw of wind energy …as per the policy of Govt.

I think there are two ways of looking at the wind energy invedtment scenario.

- CYCLICAL STORY…in the next 5 years, there will be very good orders for WTG manufacturers, as the Govt target of 32000mw is implemented. Since suzlon has highest manufacturing in india and good R&D leading to high plf wind turbines…Suzlon too would get very good order flow…maybe to the extent of 11000mw as envisaged by Mr Tanti …or may be a bit less… Nevertheless, the topline will have a good year on year compounded growth. That makes, Suzlon a very good cyclical play for next 3 years…by that time the price will be fully factoring the future growth too and that would be the time to exit.

2)SECULAR GROWTH STORY… in the second scenario, as the Plf of wind + solar hybrid further improves due to technological advancement along with the improvement in storage technology, then on a global scale( including india) more and more power capacity would be added in renewable space and less and less in the thermal power space. In such a scenario, renewable energy would become mainstream…and WTG manufacturers will have a very strong and continuing growth for a number of years or maybe next two decades. In such a scenario, Suzlon can even surpass its historically high price as it embarks on a multiyear bull run…

As of now I do not know which scenario will play out, because its difficulty for to predict the rate of technological development in renewables. Therefore, at this point of time my investment in Suzlon / Inox wind is only as a cyclical play for next 3 years.

Those investing now, would be getting on just at the beginning of the upcycle and will see their investments grow from eps growth and p/e expansion.

Whether or not renewables become a growth story will be known during the second edition of Modi Sarkar. For most investors, returns from the cyclical play should be more than adequate.

PostScript…My intention is not to tout wind energy or to defend it at any cost or against each and every objection / contrary opinion. Henceforth, i will refrain from saying on the renewable / thermal energy debate. Investors may decide the issue as the wish. My investment thesis is based on the cyclical play.

2 Likes

My disclosure and source of my bullish bias vis a vis Suzlon is already on record.

Now coming back to the micro analysis of Suzlon…pl read the excerpt from Tulsi Tanti interview to Business line newspaper…wherein, he talks about the impact of the competition…

The market seems to have attracted many new players. Vestas is back, Senvion is entering India with Kenersys, Acciona is bringing in Nordex machines and there are talks about Ming Yang getting serious about India. How does Suzlon see this competition?

First of all, the fact that many players are coming goes to show that our market is open to competition. Our Prime Minister is visiting many countries and communicating the 175 MW target. Now, 175 MW is a high number, and many players are attracted.

I am not worried about the competition. After all, I am picking up business in their countries, what can they do here? Siemens, GE, Vestas have all been here. India is a very complex market. Their products are not very competitive in India. Kenersys is even more expensive. It is an Indian company, part of the Baba Kalyani group, if they couldn’t succeed, what will a foreign company do?

We will keep increasing the size of the cake and keep taking larger share of it, the rest of it will be divided among the other players. See, we were absent from the market for three years (due to financial difficulties) and that is when some others came in. (Gamesa was the market leader last year.) But last year, our installations grew 100 per cent. This year, the market will grow 30 per cent and we will capture most of the growth.

6 Likes

Positive for Suzlon

1 Like

Hi all,

I have worked to prepare a report on Renewables and energy situation in India. It gives an objective view based on facts, management commentary from Inox, Gamesa and Suzlon.

RE future is indeed bright as India is the 4th largest RE market in the world. Coal is in decline, economy of scale, better technological innovations and productivity work in favour of RE. I like to state the fact that leveling cost is stacked against wind as solar cost of generation is cheap. Govt has placed duty on imports which augurs well for Suzlon. Suzlon is looking for no of incentives from govt such as export benefits and zero GST.

Sector Tailwinds and better PLF is in favour of wind. Increased competition and innovations in solar could threat the wind power landscape. Wind is available in 8 states only. It’s govt subsidies which worries me and cost of capital will go up which could affect IRR. Solar is much cheaper to produce and cost of funding is realtively easier. IRR remains subdued in solar due to auction price competition. I don’t see good ROE for now due to competitiveness of RE industry. There is a reason why stock price is not going up Inspite of sector Tailwinds. Debt and low ROE in near to medium term. Foreign investors would still be comfortable with low IRR due to global low return outlook. But domestic retail investors can enjoy better IRR from other industries in India.

Please conduct your due diligence before making further investment.

10 Likes

A very good and detailed report…the more appropriate word would be GREAT…presents a very positive picture about prospects of renewable energy…

BUT I don’t get one thing…your posts are not so bullish…infact quite cautious…but your research paper almost makes a compelling case for investment in Suzlon / Inox wind…

2 Likes

It’s a bullish RE sector report but not a bullish report on retail investment in wind and solar space. I have given reasons before. If you are comfortable with low IRR then you may add RE as investment in your portfolio. I still feel that solar and battery would cause bring down competitiveness even further where wind has to bring their cost down which further draws down the IRR. This is a disruption industry so good investment now could become bad investment later. Watch out for solar auction and wind auction prices. The lower they go the more competitive it becomes. There is no doubt RE targets would exceed what is set by govt for 2020, 2030. Growth will be huge without any doubt. Operational efficiency, productivity, better technological innovations need to be looked at here. One of the things Mr Tanti mentioned that he would not let margins erode away and has a margins guidance of 16-17% for next year. His immediate priority is to clean the books and strengthen the balance sheet. I have mentioned key risk in Suzlon investment and they are in the report. I am painting a balanced picture. Promoter has lot of experience, bank facilities of Rs 1300 crores guaranteed by Rs 1800 crores assets (mentioned in the report). The downside is v limited from here and you only see upside. BTW one fact about investments, the greatest investments are in turnarounds. Suzlon has been at the inflection point and can turn negative EPS to positive EPS at any time in few quarters. So, you can make money here but long term sustainability due to low IRR could be an issue. But still your investment would not turn sour. I am not over optimistic or too bullish as some of the other people but optimistic that things will be better from here. One thing is sure that crude may not see it’s golden days again and infrastructure has huge tailwinds due to better govt fiscal position. I have mentioned in the latest report that lowest solar auction at Abu Dhabi power could compare to crude at USD 10$/barrel. Even the crude mining is now happening using solar power in Middle East. Wind has an advantage that it may not occupy too much space and a better PLF than Solar. But this may change once we have better storage batteries. The whole business looks to be commoditised.

I have tracking investment in Suzlon since 2015. I am closely watching this space, infact the whole electrical generation sector.

6 Likes

What I understand is that while there will be volumes - there will not be any moat to make good money by wind/ solar power generators.

Like the airline business- passenger volumes are increasing but the fares are moving southward - thus impacting their profitability

Let us look for a business where volumes could be increasing for years to come - but without impacting the profitability.

4 Likes

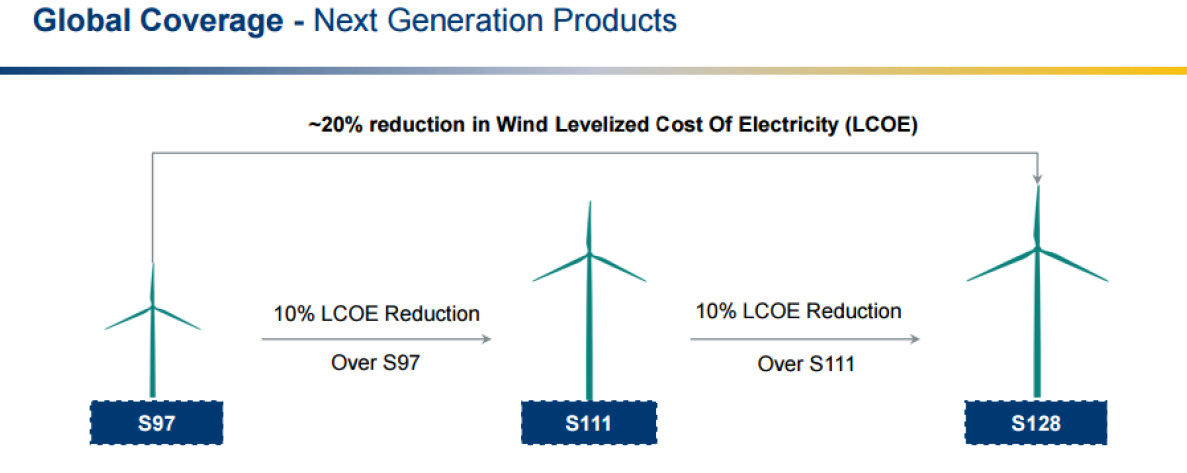

Once Suzlon starts selling S128 in export markets, there would be immediate 20% reduction in LCOE. This would be a big trigger if they build up a decent export order book on S128.

Don’t write off Suzlon yet but industry remains competitive. Suzlon moat lies in the fact that they keep on producing these turbines which reduces the LCOE and make the margins improving in a competitive industry. Plus, the hybrid projects give a less PLF than pure Wind project but reduces the LCOE further. RE is like a good cumulative yield over a long term. It is an annuity like business with good cash flow. Expect higher volumes in Q4 with margin around 18-19%. this business is non-cyclic in nature.

Suzlon this year growth rate ~ 30%

Next year Industry growth would be atleast 15%. Suzlon will much exceed this growth rate.

By Tulsi tanti

Source: Taken from my report.

I have painted a balance outlook. You decide if you deemed it as a sound investment.

Cheers,

Amit

3 Likes

How Solar Energy being the most reliable way can overtake other forms of RE sources over years (may be 5 to 10 ?) can be seen in this article from Bill Gates. https://www.linkedin.com/pulse/beating-nature-its-own-game-bill-gates