Misled on Suzlon along with aammiitt2

I have sold the positions way back in 2018…Did not make any money…no loss/profit situation for me…You would not find me commenting here for over an year…I knew this cannot be revived unless 100% acquisition by PE…

Disc: Not holding > 1 year.

Bankers said Suzlon failed to come up with a debt recast plan by December-end deadline and is heading for bankruptcy courts by next week.

Dilip Shanghvi staring at huge loss as Suzlon Energy heads to bankruptcy

Dilip Shanghvi, the billionaire-promoter of Sun Pharmaceutical Industries, is staring at a huge loss having invested Rs 1,400 crore in picking up 23 per cent stake in Suzlon in 2014 in his personal capacity,

1 Like

Dear Forum Members,

Am posting this message on behalf of learning and comment/statement are from the old managing director/CEO of suzlon(JP Chalasani)

This is not an investment idea or opportunity to enter - the company is in huge debt with 9,759 crore debt.

Am not invested and i strongly urge the members to not invest unless there is some positive impact - My sincere request

My below comments are from the video - you can have a look

What are the existing problems that the renewable sectors are facing?

Trading Tariff - Bidding War is the problem wherein when you bid for a lower amount/cost the more its acceptable in the market and people intend to use

Wind tariff has gone from 4.5 - 2.85 (Now)

Renewable Energy Challenges

- Solar

- Wind

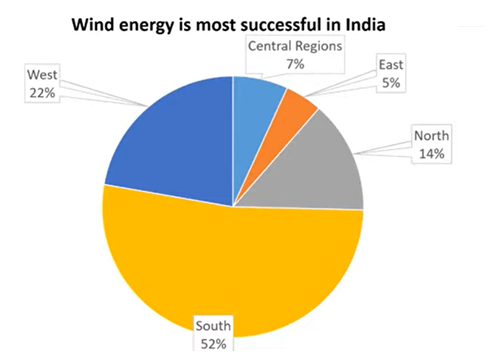

Both sectors are not in a fight against each other as you can see below chart :

South dominates in wind due to coastal lines

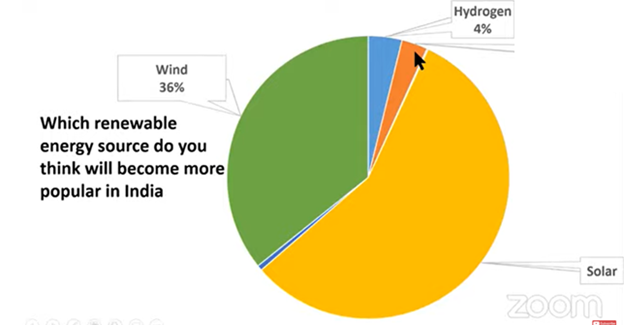

Which renewable sector is popular among all?

Solar

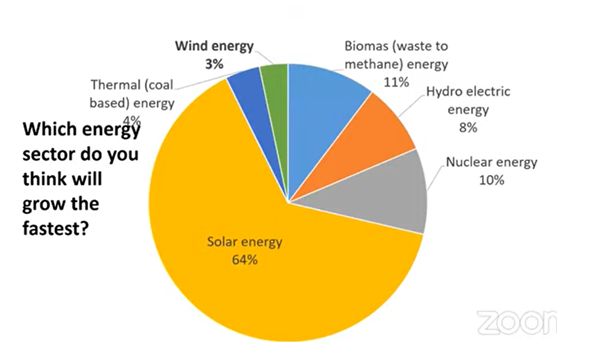

Which energy sector will be the fastest growing sector :

Solar

Then why in comparison with Wind when solar takes all advantage?

Solar alone cant/ will not be able to supply power to the entire nation - there are circumstances that wind has to play in.

India is not fond of power but they are more concerned about the pricing affordability rate/tariff - they wont be bothered about solar/wind when it comes to renewable sectors

Conclusion Hybrid is the solution to achieve target of renewable sector for 2022: Wind + Solar (Married together - it cant fight)

Wind is the significant renewable energy

What are the other problems?

- Integrating renewable energy & power sector

- Decentralize distribution for rural sectors

Integration team :

Minister of power - Power Grid

MNRE (Minister of renewable energy

What are the opportunity growth for renewable sectors?

-Repowering

-OEM

Long consolidation is happening in OEM : Next 8 years globally 3 OEM will have 90% market share

What if the new players will have to make an entry, why will they have a problem?

- Cost cutting

- Efficiency - They cant survive

What changes in government you think will happen?

-

Wind Sector makes the criteria of make in India concept (Atmanirbhar Bharat)

-

Atmanirbhar : Power sector will create huge employment opportunity in India government

can bring in more and more project. Since we are at the lowest point now in terms of

employment - there is only way that is going up -

We have 10 GW wind capacity in India

-

Current capacity utilization 15-20%

-

India can become hub for exports - even the component manufacturers

Do you think we have to depend on China?

Not for wind sector - as China are more into Solar so there might be chances that if there is less power generated then we may have to tap in other markets for power

Target by government : 2022 - 60 Giga Watt

Today we stand at : 37 GW

Last 3 years - we did less than 3.5 GW anybody’s for 2 more years

Your views on Suzlon?

Suzlon has huge potential - It’s pioneer in India and has a significant business model

FY 17 was the best year for Suzlon as it generated 1800 MW alone

There is no subsidy in wind - Interstate transmission charges are the benefit due to transmission cost

Land acquisition & roof top solar : Land acquisition are very costly

Commercial viability is problem for roof top : Distribution utility will be a problem

Am sorry if some statements may have interpreted wrongly - as i have noted down to my level of accuracy.

@ayushmit, @hitesh2710 : Sir as we are seeing there is underlying pattern in terms of IDBI / YES BANK/ BSNL / ADANI GREEN : Government is infusing capital to stop China export order.

Given a play of Atmanirbhar Bharat : Along with side of employment opportunity, 2022 renewable sector target & future of EV with current government electric buses to run on - needs power. - Can you give your thoughts in 1-2 statement?

Disclosure : Invested in Adani power ( Am not an SEBI analyst nor this is a stock recommendation, please consult your financial advisor before investing )

Adani - Since due to their presence of solar energy model & currently with tie of government to generate 8 GW. The beneficiary would be adani power - it has raised to delist itself however refrained and the next day it raised capital from shareholder) power sector will have a continuous set of growth however it depends on tariff prices/rates. Suzlon on other hand failed due to high land acquisition cost for wind which have taken them to bigger debt book

2 Likes

Has anyone still got interest in Suzlon? It has moved up quite nicely since the Q results. Breaking out at 6.38 will make this very exciting.

1 Like

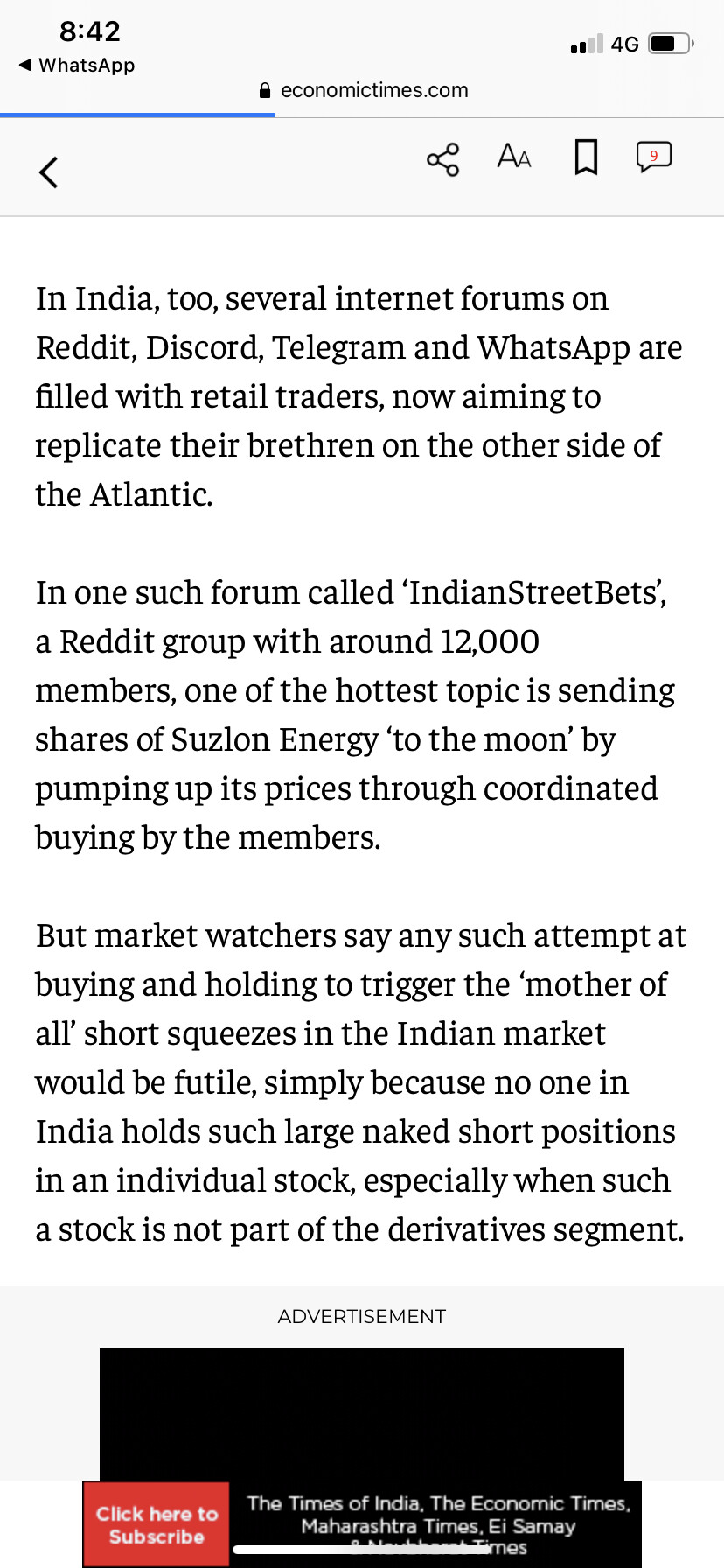

GameStop-like bid on in India. Worry not, it’s a hopeless case

via ET Markets App(Download Now):

http://ecoti.in/YIlC9Y

Suzlon is quoted in the above news

Any new views on Suzlon? Debt reduction and showing Net profit last year could be good triggers. What is holding back the stock?

steel prices are a concern on the margins . once commodity cycle stabilises, hopefully there’ll be enough cash flow to show breakeven after interest payment. It’s a penny stock because operating profit cannot pay the entire interest

24.05.2022: Allotments of securities issued in June 2020:

- 4.1 lakh OCDs of FV 100,00 converted to 57.14 crore new equity shares > On conversion of total o/s value being 4099 crore

- 49.85 crore warrants > cancelled

- 99.71 crore shares > Lock-in Requirements waived off

No impact on current debt levels.

offshore power not commercially viable

Hi guys,

I would like to discuss all the problems faced by RE(wind) and the new policy by GOI to tackle them.

Firstly I would like to discuss what all problems between 2017 - 2021 lead to a decline in this industry.

- Shifting for FIT(free in traffic) to e reverse bidding.

- DICOM not fulfilling their signed PPA

- Wind turbine manufacturing company loosing their PGB(performance bank guarantee) because of not meeting their project requirement on time.

- Poor GRID infrastructure discouraging OEM to participate in tenders.

- Poor land policies which became a huge barrier.

- Increasing GST form 5% to 12% which increased the LCOE (levelized cost of energy)

- DISCOM not doing payment on time because of their poor financial health.

- Increase in price of commodity ( steel a major component, nickel) and logistic cost during covid further added salt to the wound.

After 2020 the cost of conventional source of energy increased and government realized the need for RE energy.

Now I would like to present all government policies introduced to face the above issues.

-

Introduction of RPO (Renewable purchase obligation). The MOP (Ministry of power) has

now introduced RPO for non-solar which was earlier for entire RE.

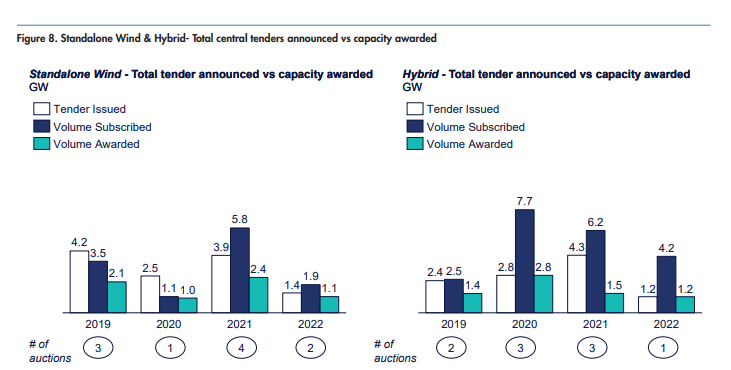

This specifies the power distribution companies to set up minimum capacity over the years.Central tender is expected to have 76% share which is going to decrease the state tender.

This will reduce the problems faced by developers earlier with DISCOM.As per new wind RPO requirement announced by MoP, ~57.5 GW of India’s power demand will be supplied through new wind projects from FY 2023 to FY 2030.This will lead to cumulative wind project installations of ~ 97.5 GW till FY 2030 against a target of ~140 GW set by government. Hybrid and Hybrid+ storage are expected to take this to 140GW target set by GOI.

-

Earlier the PBG were in the range of 8% to 12% which has been reduced to 3% in 2021 which will help in improving the liquidity of the company.

-

Renewed interest in tender auction because of the following evolution ’

**a)**Increasing the transparency to boost developer confidence

**b)**Specifying land and grid details of the delivery point in the tender document before auctions. Also, the projects are in the states of Madhya Pradesh, Maharashtra, and Karnataka to avoid congestion in Gujarat and Tamil Nadu

**c)**The removal of tariff caps had provided relief to developers as price increase from supply chain should be considered in future.Tender subscription volumes between 2017-2019 were 50%-80%. Between 2020 and 2022 we can see it being oversubscribed

. -

Waiver of ISTS(inter state transmission system) for PPA signed before 30june 2022 for 25yrs and thereafter increase of 25% per year till 2028. This creates an incentive for power distribution companies and developers to sign PPA before 2025.

Waivers to open access(OA) will incentivize third party to directly purchase form developers instead of dicom. Earlier OA was applicable for direct purchase. -

There has been major devolepement in repowering policies which are as follows

a)Repowering in central wind and hybrid auctions before 2021 was restricted to the allotted capacity. During 2021 capacity restrictions for repowering have been removed.

b) Earlier sale of excess generation on repowering of a plant could only be sold to SECI(solar Energy Corporation of India)at 75% of the rate prescribed in the PPA. Now it is allowes to sell to third party as well.

6.To develop an intrastate network**(GRID)**, the central government has announced two phases of Green Energy Corridors(GEC).The first phase is expected to be completed by 2022.It is estimated that ~44 GW of new RE power generation evacuation will be possible through GEC.

24GW from first phase which is due to be completed in 2022 and 20GW from second phase which is yet to be approved.

7.Land policies have been revised and the process is being streamlined in key windy states.Gujarat, Maharashtra, Rajasthan, and Madhya Pradesh have a dedicated land allocation policy for RE.

Karnataka has released a new RE LP in 2022.No land policy update is observed in Tamil Nadu region.

It takes 6-9 months for land allocation process in states where the process is stremlined and 18-24 where process is not streamlined.

8.Government is aggressively promoting WSH (hybrid) and WSH +storage( round the clock).

DISCOM need 24/7 power supply due to variability in RE they re dependent on conventional source. The cost of storage/battery is expected to fall and increase the demand of WSH+ storage which solves the problem of DISCOM.

WSH increases the efficiency and reduces the cost of power. The HYBRID category is also expected to drive the demand in future.

All the above information has been taken for a detailed industry report below(58pages). I would recommend everybody to go thought as it explains much more than what I have done above.

The report is free and not purchased by me

Click on download report and enter your name, email ,phone no and download

Please read this report if interested in this sector. It is information overload free of cost.

In my next post I would love to present my view on Suzlon and how I feel it has a good opportunity in future.

Government has realized the need of RE between 2020 and 2022 and is aggressively trying to revive this industary from its policies.

Suzlon is a call option on government policy and this industry which I will sell once I see government not showing further interest in it( at least till 2030 I don’t see this happening unless central government changes, their intent is very strong and the future of this industry looks bright.

It is 4% of my portfolio with average price of 8.25.

7 Likes

Hi Guys,

Today I would like to discuss about the demand side of this industry

Let me start with the board level targets thereafter we will go in detail.

-

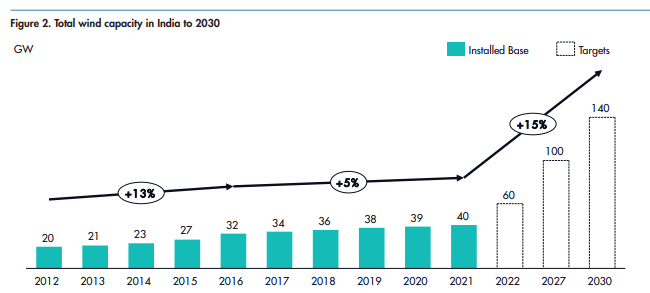

GOI have a target of 140GW of wind capacity by 2030 with 40.4GW of capacity from FY23 beginning.( Please note this 140GW of target includes standalone, hybrid and round the clock wind energy)

-

By 2026 government has a target of 60GW of capacity from a base of 40GW at 2022 January.

-

Our power demand is expected to be at 817GW by 2030 and government has set a target of 50% of this to be catered by renewable energy(all category).

-

With every 7% growth in our GDP our power demand grows at 6%. The co relation between GDP and power demand is high.

-

India has huge potential in wind energy. 127GW in offshore and 695GW in onshore at 120m hub height.

6.Good amount of repowering opportunity especially for suzlon because suzlon was in an expansion phase between 2000 and 2006. Since most of the wind turbine have a life span of 20yrs this creates good amount of repowering opportunity between 2020-2026(Will try to quantify this). Favorable repurchase policy further incentivize developer’s

How realistic are these targets?

Most of the targets revision and policy making was done between 2020-2022 and these two years wind energy has not been able to achieve those targets set by government for the particular year majorly because of covid. So as on today wind energy is lagging against the target set.

These targets being met is completely in the hands of government becasue they are the only customer especially wind (commercial and Industrial share is extremely low). The urgency this government is showing as on date and the policy they are introducing makes me belive that they are achievable. BIASED

One of the big factor for this industry to achieve their targets is BJP coming in to power post 2024.

Current pipeline and 2026 target of 60GW(standalone)

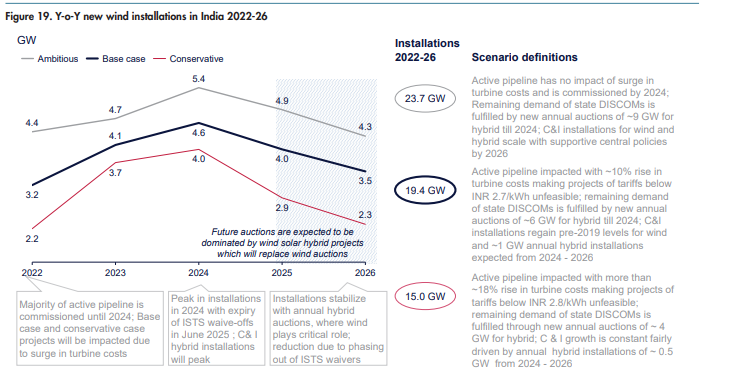

This forecast does not include tender from PSU, Round the clock tender and repowering. RTC is expected to dominate post 2025.

Demand has been projected taking 3 scenario because the cost of manufacturing has a big impact on the demand and supply especially wind because the manufactures cannot pass the cost to buyers.(Buyers have bargaining power)

Up to 2026 19.4GW of capacity has to be installed(base case) out of which 14.9GW from central,3.1GW from state and 1.4GW from C&I. (center having 75% share and state having just 16%)

State auction= All previous problems and Central auction= favorable business.

The average power purchasing cost (APPC) across 19 states procuring power from central auctions is reported to be 30-35% higher as compared to standalone wind prices in central auctions. Also, these states have APPC ~50% higher in comparison with hybrid wind projects of central auctions.

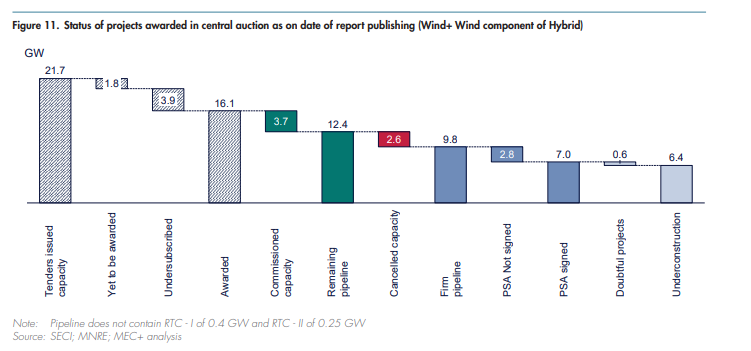

This is one of my favorite charts because this shows how much you start with and what you end with.

1. As of now there is 9.8GW of firm pipeline and further tender of 5.1GW will be issued to meet 14.9GW.(For center)

2. 1.4GW pipeline for state and further tender of 1.7GW will be issued to meet 3.1GW (For state).

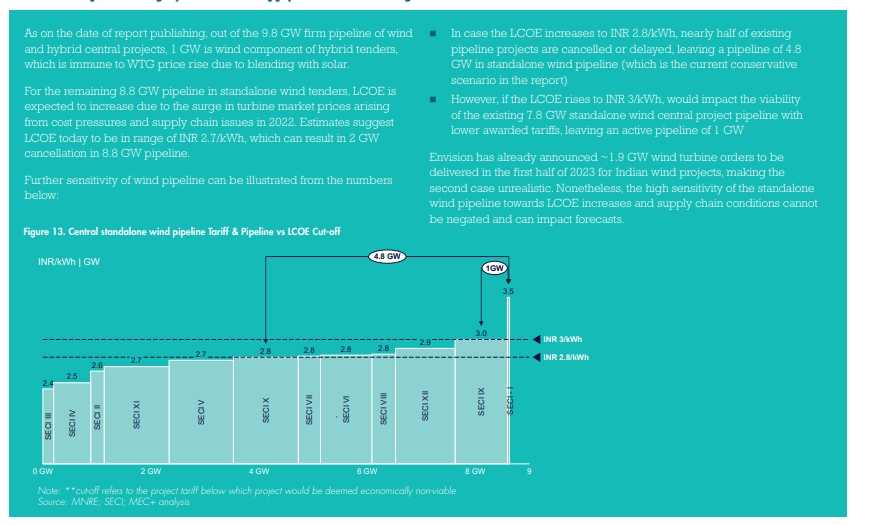

This is the sensitivity analysis for central wind projects.

Future cancelation can be determined form traffic.

With Suzlon having close to 2000cr debt and 500cr of cash and 1GW of order book it looks strong as of now.

Question which I have in my mind for suzloz. Will find asnwer for them.

- What is the brake up of thier oderbook (how much is standlone,hybrid,round the clock).

- Are they just planning to do the wind component of WSH and WSH + storage in future.

- The benefit of debt is completely going to be visible by next quater so how is the company further going to increase efficency.

- What will they do with that cash

- At what quantity fixed cost gets covered and operating leverage kicks in.

The demand and policy looks favourable. I am still understanding suzlon as a company.

In October 2021, Adani Green Energy Ltd. (AGEL) acquired SB Energy India for US$ 3.5 billion to strengthen its position in the renewable energy sector in India.

Suzlon promoter having extremely low stake also open an opportunity for it being acquired in future as the acquisition trend in this industry is extremely strong as of date.

All the numbers and charts have been taken from GWEC(global wind energy council)

report which is free.

thankyou

8 Likes

Hi guys,

After discussing all the policies and little bit on demand today I would like to talk on Suzlon and where I see this company in coming years.

Please note that I like to go extremely mathematical and then support those numbers with qualitative aspects.

About Suzlon

- Suzlon is an OEM and they make wind turbine generators. They are the 3rd largest player with 33% market share.

- They have cumulative installed capacity of 19.5GW in 17 countries with almost 14.5GW in Asia.

- They are a 25yrs old company and an end to end service provider

What is end to end ?

I think this is one of the major strength of Suzlon

- Last year Suzlon did 807GW of business. Their current year first half is 15% higher than FY22 H1.

- They have a ready capacity, workforce and ability to diliver 3.1GW per year.( this capacity is almost 4 times their FY22 output, this means sales can go 4x without addidional capex)

- We have a target of 140GW by 2030 and here is what management has to say on it.

- Suzlon had a debt of 2200cr and there is another 600cr of rights issue due, close to 200cr of cash, 2 assets which is non core to the business which they are planning to sell.

a) 11 acre of land in pune

b) SE Forge 100% subsidary of suzlon

NOTE- (Suzlon has the ability to take their debt level to 1000cr and interest cost to 100cr per year)

Demand analysis.

140GW is a pretty big target and has a lot of time to be achieved. Let us be conservative and try to predict the demand which Suzlon will have.( Please note will take reference from my previous post)

- A total for 8GW of tender will be issued by central and state till 2026. Suzlon can get 2.5GW form this

- As per MNRE there is a repowering need of 25.4GW up to 2030. Suzlon has a possability of 7.5GW from here. Let us take only 2GW up to 2026

- Suzlon as on date has 1GW of order book. Out of this 284MW is from retail/PSU(please see next point)

- PSU and C&I segment is not included in the above prediction where as because of ISTS wavier up 2025 they are aggressively setting up wind farms. 30% of Suzlon current order book is from this segment. This is further going to add to their demand.

As of today we have a 5.5GW of predictable order book this does not include the PSU and C&I which is a big segment.

So for the next 3.5yrs we have 5.5GW of visible demand. Since this is the base case assumption and does not include some big segments I think this is not optimistic at all.

My expectation for Suzlon is 1.5GW of business in FY25 or FY26. This is 85% higher than FY22.

This cost of debt might come to 100cr. I am expecting 1.5 EPS from them(this is extremely conservative because their incremental margin on new sales keeps increasing)

I am expecting 25rs to 30rs by FY25 or FY26.

ADD ON

- They have their AMC business which has been flat form many years because of no new big capacity being set up post 2017.

( If somebody can please quantify this by taking last year AMC revenue divide by their asset under management which is 12GW and multiply this to 5.5GW) - Suzlon is also planning to do AMC business for other turbines which has not been developed by them. This segment has 40% as EBITA margin and is pretty big

Their new prototype is also a big add on which can produce 3.1GW

With favorable policy and huge demand I feel there is a good opportunity for suzlon in the coming years.

I would love to double my qty in this stock below 10rs.

This is 3.5% of portfolio on CMV of my portfolio with 8.25rs as avg price.

6 Likes