All but gone with the wind: The unfolding sad story of Indias wind sector

Wind power, which along with solar power was expected to make India a renewable energy powerhouse, is struggling for survival.

2 Likes

With his current interview with CNBC, Tulsi Tanti sounds positive as ever. But a clear message one can read is that 2018 is a transformational year for wind energy (in a very neutral sense). Some of the salient points discussed and my personal views on them is stated hereunder:

-

Mr. Tanti says that there is no renegotiation on PPAs contrary to what the states have been demanding. This contradictory statement, from what the States have mentioned, probably stems from his proximity to central government who he expects to convince the state govts to honor the PPAs. Based on the assumption that there won’t be any renegotiation, Tanti is confident of achieving 15% EBITDA margin. In my opinion, this would be the single most important issue which will decide Suzlon’s stock performance in FY2018. If the PPAs stay the way they are and if Suzlon is able to deliver 15% EBITDA margins, then their orderbook is strong enough to sail through this transitory phase without much impact.

-

Tanti is confident of gaining 40% marketshare in FY18 but he stood non-committal on volume growth. The volumes he said are dependent upon the bidding process and would be a prerogative of Center/State govt. For the reverse auction to succeed in progressing the wind energy sector in India, higher volumes from auctions for non-windy states would be critical. This I believe is a short-term complication which soon enough will be negotiated and resolved by the government. However, the uncertainty remains for FY18. If govt. is able to resolve matters in current year, then we could see wind sector making good progress in this year itself. If not, then I am quite sure than FY19 would be a breakout year for wind energy sector in India.

-

Suzlon is sitting comfortable on debt. I see them holding foreign currency debt of $600ml for long term (till 2023). It does not harm them either as the cost of debt is merely 3 percent odd. Offcourse they would be exposed to currency risk but with stronger rupee and improving balance of trade with US, I see it working out positively for them in near future.

-

Going forward Suzlon has much to benefit from its accelerated R&D where they are already working on products to increase PLF to 45% (from 42% currently) from wind turbines and PLF of 50% from hybrid technology. The lower LCOE would in turn improve margins and improve their competitiveness in the market.

-

Lastly the FCCB conversion is almost half way through and will continue till the end of FY18. With most estimates already accounting for these conversions, there won’t be a major impact on Suzlon, if only their operational performance treads the growth trajectory. Again if they continue to execute their orderbook without negotiation and get the payments in desired time, there will be enough retail interest to absorb FCCB selloffs.

-

And I find a sudden mum on CDR exit issue which I believe is becoming a procedural hassle for Suzlon. They have left it upon the banks to complete all compliance and have decided to refrain from giving any guidance due the nature of event being uncontrollable for them.

In conclusion, my conviction on long term performance of both the renewable sector and Suzlon stays bullish with a neutral stance on short-term performance. Since it is a transitory phase, it might get frustrating for stakeholders. There could be delay in policy formation. Also I see delay in next phase initiatives of formulating hybrid policy and offshore policy which I feel might see some action in 2019 furthering the growth of the sector in 2020 and thereafter.

16 Likes

Tanti has said that they are now testing S111 with 140 m tower. I think this is in addition to S128, which is already under testing and will be introdued in the market in the next year. In the game of higher and higher PLF turbines, Suzlon appears to be ahead of the competition. Inox wind does not even have a 120m WTG (as of now).

Secondly, Tanti speaking at the end of Q1 is saying that Discoms are going ahead with the PPAs already signed. This gives me hope that the Q1 and Q2 results may be not bad.

Thirdly, the FCCB getting converted and sold in the domestic market will continue through fy18. This may keep the share price subdued for the whole of 2018. And by next year, once the transition from FIT regime to auction based regine is completed and FCCBs are sold off…Suzlon may then make rapid strides.

Investors may view Suzlon as a story that will develop fully from next year onwards only…

10 Likes

-

what is the issue in suzlon coming out of CDR? I keep reading that the ball is bank’s court. Why is that?

-

TUlsi in the intreview said state govt is honouring PPAs witn even Rs 15. The difference is so huge that i am confused. Can someone clarify.

-

There are pockets of power surplus that we could see. No one is talking about it. Do we really have a huge supply demand gap?

There are procedural guidelines set by RBI for a corporate to exit CDR. It requires a detailed scruitiny of financials and setting of recompense mechanism. You may have to read the CDR circular to have more details. (Pg. 55 of the doc includes basic guidelines on cdr exit).

http://www.cdrindia.org/downloads/CDR-Master%20Circular-29Apr15.pdf

TT is referring to a ten year old solar contract in Gujarat where the state govt is still honoring its commitment. It is just a illustrative point he is making and has nothing much to read in it.

Indeed India is a power surplus country overall, but just like wealth there is uneven distribution of power too in India. Surplus states sell power to deficit states at high rates. The business suffers due to higher cost of inputs making the industrial units in deficit states less competitive to ones in the surplus states. Also, it becomes hard to supply uninterrupted power to several part of the state. Millions still live in darkness. Pilferage is another issue faced by discoms due to high power prices. It becomes a vicious circle. Anyways that is an old story. The new story is that with Paris agreements the source of power generation will shift from fossil fuels to renewable. Also, the new initiatives by Govt. like Made in India, Digital India, power to all (rural electrification), 100% e-vehicles by 2030, etc. will have substantial increase in power demand in coming years. And there is no points for guessing the sources it will be generated from - offcourse renewable mainly. Also, just like we have surplus water in some states and deficit in others and to address this govt. came up with National River Linking Project, similarly Govt is working on ‘One Nation, One grid, One Frequency’ program to address uneven distribution of power. These structural reforms in power infrastructure are long due and much needed to meet the growing social and economic needs of our country till 2040.

12 Likes

Thanks. Excellent and educative reply. Respect!

2 Likes

Hi -

Excellent analysis, and comments throughout the thread.

I was trying to find the international business the firm has. In the investor’s presentation, they have mentioned that they are targeting/developing S128 - 3 MW, specifically for international market. Do they have any presence/existing relationship there, or they would start from scratch?

Thank You

Dear experts,

Few more points and questikns.

-

Looks like india is a power surplus country. If the operational and connnectivity issues, grid, etc are addressed, the supply becomes even more. Will this not bring down unit prices further?

-

I watched Mr. TUlsi’sinterview. To me the whole thesis looks like govt wants to dramatically increase wind and solar power. When the supply is more, govt. might decide to go slow. Is there a clear plan to shut down existing coal power plants. Is that possible in india?

-

Mr. Tulsi feels the past issues are more do to with unresonable conditions by foreign bankers etc. I dont get the past story fully. The fall seems to be too big to have been caused by one reason alone. Can some one experienced give a gist? Or share a link to case study etc.

Dear @goyal_nike , Folllowing link can be a good starting point for your research. http://www.suzlon.com/about/suzlon-worldwide

Dear @Maddy ,

I appreciate your inquisitive posts. And I don’t mind answering any question as long as I know the answer. However I would also request you to do a bit of fishing yourself as some of these details are already available publicly. [quote=“Maddy, post:281, topic:5575”]

Will this not bring down unit prices further?

[/quote]

Yes but its not bad. It happens in many businesses. There are high-MARGIN businesses and there are high-VOLUME businesses. For ex. in automobiles Ferrari, Lamborghini, Bentley are high margin cars which sell less number of units. While Maruti and Tata Motors (not JLR) are high volume cars but low on margin. It depends upon the company whether they want to adopt a differentiation model or low-cost model. Similarly there are industries which over their lifetime transition from being a high margin industry to a high volume industry. Telecommunication services (both voice and data) had high per unit rates when they were introduced in late 1990s and early 2000s but to make them mass consumption services, prices kept reducing and industry kept growing. In India, TRAI ensured price moderation for the benefit of conumers. Voice business did very well for 10-15 years giving excellent returns to companies and shareholders. The next set of growth would come from lower prices in data services and VAS which still has further growth potential in India. Similarly, for wind sector to grow in volumes, price moderation is necessary and would pave the way for next 10-15 years of excellent volume growth benefiting companies and shareholders.

Shutdown? No. But their contribution will reduce significantly.

Long story short, Suzlon was not allowed by German banks to use their subsidiary Senvion’s cash resources to pay for its obligations, although Tanti tried very hard to comply with merger requirements.Consequently, Tanti was left with no choice but to sell the asset to recover cash and pay debt.

4 Likes

Thanks for the detailed reponse. The link is useful and gives a detailed story. I will surely try search.

1 Like

Yeah…i too would like other members to do some research and post it on this discussion thread. It is the diversity of views that leads to a better understanding. And contrarian opinions are nost welcome.

2 Likes

Friends, I had a chance to chat with a ratings guy in renewable space on Suzlon.

Expectation is that all the states will move to auction format; which will result in increasing competition on technical aspects and possibly also bring down prices for wtg manufacturers Suzlon or Gamesa.

Suzlon technically has good turbines and should be able to compete over next couple of years; but the technical evolution in Europe is quite amazing with some companies building digital wind farms. So, Suzlon will have top continuously upgrade its wind mills.

Apart from Games, Inox & GE i.e. existing players, new players are also entering the country including a Chinese player and Senvion and few others.

repowering could benefit Suzlon in a big way as Suzlon’s early customers have best land access; which Suzlon should be able to capture once the policy is finalized.

To the fellow investors, can we get a view on LCOE and per MW pricing of key models for Suzlon and Gamesa.

As i see, over next two years competition would be with Gamesa and so good to understand the economics, given bidding based PPAs.

6 Likes

two seprate news article

gamesa is slightly ahead in mw game at 3.3 mw, their offering in turkey. the technology i believe they could easily bring in to india on need basis.also now with merger, their onshore and offshore portfolio looks amazing… suzlon 's international offering at 3 mw of s128.

second one talks about coming competition!! almost like winter is coming & there will be bloodshed!

1 Like

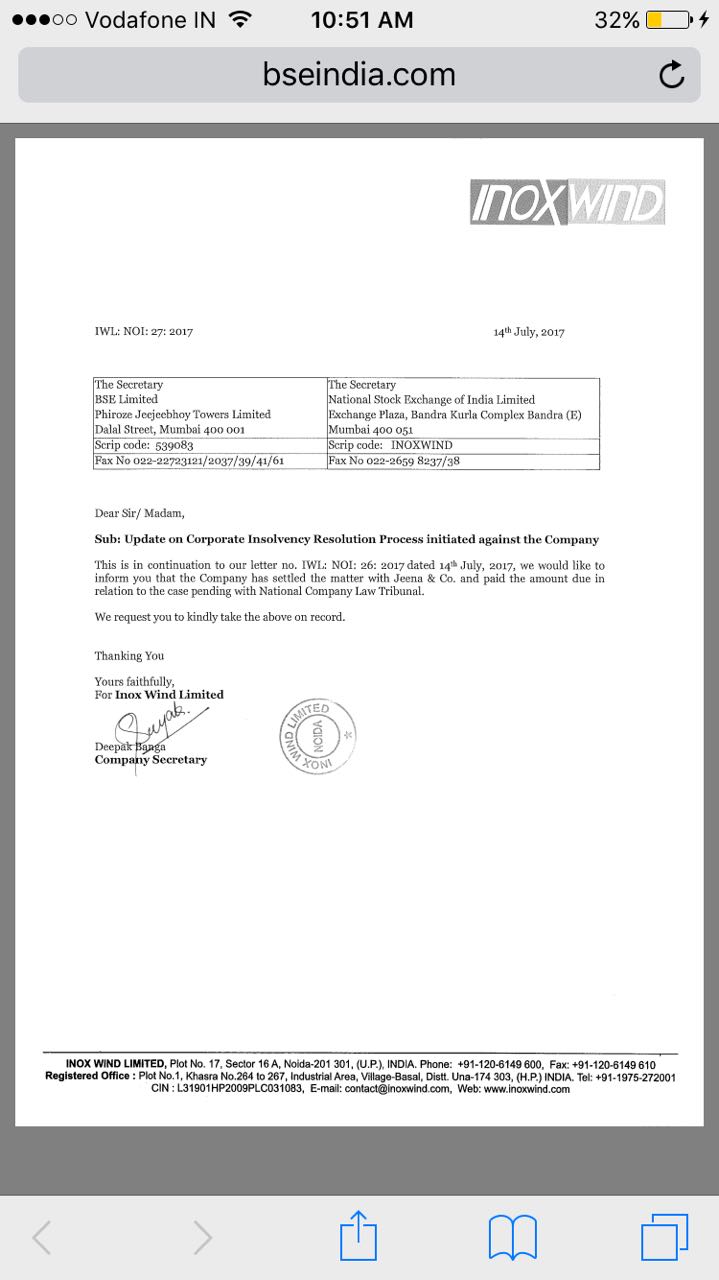

It seems the worst is happening for Inox Wind. I wonder how it will impact the sentiments of the renewable sector.

Very concise and apt note…my sense is that industry will move towards the telecom model as it matures more. Though while telecom may be a mass consumptin play…wind energy will be a more govt regulated affair…Non renewal sources is a natural imperative for the future and while suzlon is well entrenched in India in terms of reach, Investments in leading R&D and technology…it should use its own hard past experiences to navigate the future.

Disc: Invested between 17.5-18.9 and will add on each Qtry result and review of Industry dynamics

I cannot comment on the matter or its relevance. But it looks that competition is certainly taking toll on Inox wind.

1 Like

wind generated power now accounts for 28.70 GW or 57.4 per cent of installed renewable energy capacity in India, followed by solar power with 9.01 GW, small hydro power with 4.33 GW and biomass power accounting for 7.85

When it comes to future growth, the 175-GW target for renewable energy capacity (including 60 GW of cumulative wind power capacity) announced by India at the Paris Climate Summit looks aggressive; and rather steep – an addition of 12 GW of wind power capacity annually.

Looking at this it looks suzlon may grow by 20% for next 4-5 years considering many small players will not be able to sustain the auction tariff model

Wind turbine maker Suzlon Ltd. has initiated the process of closing down its loss-making overseas subsidiaries as indicated by the company’s promoters following fourth quarter earnings.

the revenues of this subsidiary is less than 1 percent of the total revenue. This move will help cut losses of the company.

India already has installed capacity of 30 giga watts and needs to add just another 30gigawatts to reach the target of 60 giga watts. Therefore, to reach that target requires addition of around 5-6 giga watts annually. Its not such a big issue…target is easily achievable.

Tulsi Tanti says that the yearly installation of wind energy may be around 8-10 giga watts after 2 years on account of demand from states to fulfill their renewable purchase obligation. Therefore, there is very good probability of India exceeding the wind energy target of 60 giga watts by 2022.

3 Likes