anyone attended conf call today? what is the status of resolving usfda issues

There are some Con. Call highlights mentioned on ICICI Research Report dated 09/02/2018.

Conference call Highlights

IPCA management has guided EBITDA margins at 18-18.5% in

FY19

YoY anti-malarial segment has reduced to 8% of the domestic

portfolio, whereas pain segment has improved to 44%, followed

by Cardio segment at 21%, thereby lowering the portfolio from

historical anti-malarial volatility in sales (earlier anti-malarial

contribution was at 13%)

On the generic exports segment, UK sales continued to remain

subdued. However, higher Canadian sales led by increased

product launches, strong 46% EU growth and 15% Australia and

New Zealand growth led to higher generic exports segments

growth. The management continues to remain positive on the

above segment and expects the UK sales to rebound in FY19

On the Institutional exports segment, the management expects

the WHO anti-malarial tender to kick start from Q1FY19. The

management expects DT business to begin in H2FY19 and

injectables launch in H2FY20

On the branded business, the management expects to grow at 20-

25% in FY19

US total cumulative filings stood at 47, of which 18 are approved

Health Canada has successfully inspected all 3 of IPCAs facilities

during the quarter

The management expects stable CRAMs numbers from H2FY20

The management has guided for effective tax rate at ~17-18% for

FY19

The management expects capex for FY19 at similar levels to FY18

i.e. 130-140 crore

The company has completed remediation at its three facilities and

has invited USFDA officials for inspection

For full report you can check below link

http://content.icicidirect.com/mailimages/IDirect_IpcaLabs_Q3FY18.pdf

1 Like

US Food and Drug Administration (FDA) has conducted an inspection of its formulations manufacturing unit in Silvassa and issued three observations. In a regulatory filing to BSE, Ipca Laboratories said the USFDA had conducted the inspection of the its formulations manufacturing unit situated at Piparia (Silvassa) from August 19 - 23.

“At the conclusion of the inspection, the US FDA issued a Form 483 with 3 (three) observations. The company shall be submitting its comprehensive response on these observations to the US FDA within the stipulated time frame,” it added.

The company said it is committed to address these observations promptly.

FDA inspection uncovers “a cascade of failure” at Ipca Laboratories in India

It has been over four years since the FDA banned the entry of finished drug products made by Ipca Laboratories in India. From a recent Form 483 issued to the India drugmaker, it seems like Ipca has a long way to go before the FDA is convinced that it meets its quality standards.

The warning letter issued to the finished drug manufacturing site located at Silvasa in January 2016 highlights that during the FDA inspection, the investigators found data-integrity issues in the Quality Control Lab.

Following an inspection of the same site from August 19 to 23, 2019, the FDA issued Ipca a Form 483, which reveals that the agency continues to have a lot of questions for the Indian drugmaker to answer on its approach to quality.

During the inspection, the FDA investigators observed “a cascade of failure” in its quality unit. And these failures pertain to “controls on issuance of GMP forms, review of laboratory testing data, conducting investigations” and conducting activities as per the written procedures.

The FDA investigators found that the Indian drugmaker had changed the computer system setting of its chromatography software to use the “inhibit integration” function which allowed it to calculate results based on “only select peaks of interest” and avoid integration of unknown peaks. Unknown peaks could represent impurities that were being excluded from the analysis and may have impacted the final decisions.

In another instance, quality control (QC) analysts were found to deviate from standard testing procedures for over 12 years while conducting dissolution tests and for more than over two years while conducting assay and related substances by HPLC (high performance liquid chromatography) tests.

The FDA also raised concerns after uncovering significant gaps in Ipca’s data integrity procedures with respect to handling of its electronic raw data.

Ipca also failed to investigate complaints in a timely manner as a complaint where “hair was found embedded in the tablet” was open for over five months. The absence of established timeline was also found to apply to changes and corrective actions as some changes had been open for almost three years.

5 Likes

Decent numbers from IPCA for Q2 , Hopefully it will sustain the breakout from months of consolidation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/593f25be-8621-4bc0-8726-a55f89ff95b1.pdf

Disc : Recently bought as part of core Pharma portfolio

1 Like

NCLT has approved the buyout of Noble Explochem by IPCA Labs as per the the provisions of the IBC.

The Resolution Applicant (IPCA) plans to manufacture key intermediates used in API’s business such as Losartan Potassium (Cardiovascular), Valsartan (Cardiovascular), Frusemide (Diuretic), Chlorthalidone (Diuretic) and Hydochlorthiazide (Diuretic) for captive consumption. This will streamline the API manufacturing capabilities of the Resolution Applicant and remove the disruptions in the supply of these raw materials.

The acquisition of the Corporate Debtor (Noble Explochem), the Resolution Applicant will make an entry into the Explosives sector. The Resolution Applicant will make necessary investments to restart this line of business of the Corporate Debtor. The required R&D will be carried out at the existing R&D centers of the Resolution Applicant as they are well equipped for the same.

The Resolution Applicant is of the opinion that the Drug & Intermediate division will commence from third year from the Completion Date, as it would take nearly one year for receiving environmental clearances and further one year for erection of plant and obtaining various regulatory approvals. The Resolution Applicant estimates that Rs.12.67 Crore shall be required towards working capital in the Drug & Intermediate division based on projections, from third year onwards. Capital Expenditure towards Drug & Intermediate is estimated to be Rs.260.00 Crore. Thus, total investment for Drug & Intermediate division is estimated to be Rs. 272.67 Crore, which shall be endeavored to be done over a span of 2 years from the Completion Date.

In the Explosives division, a Capital Expenditure Rs.10.00 Crore and Working Capital Rs. 8.31 Crore has been estimated. Capital Expenditure of Rs. 10 Crore includes repair and refurbishment of the existing machinery of the Corporate Debtor. The total investment for the Explosive division is estimated at Rs.18.31 Crore, which shall be endeavored to be done over a span of 1 year from the Completion Date.

I am not sure what to make of this. On the face of it, this seems like a bad choice since the company, Noble Explochem, seems to be in the business of making explosives. Can that facility be used to manufacture APIs? Not sure. Also, it is a very time consuming affair (3 years as per the resolution doc).

1 Like

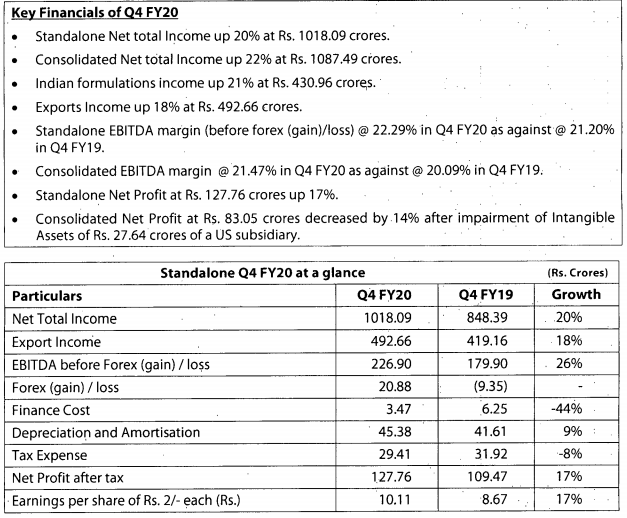

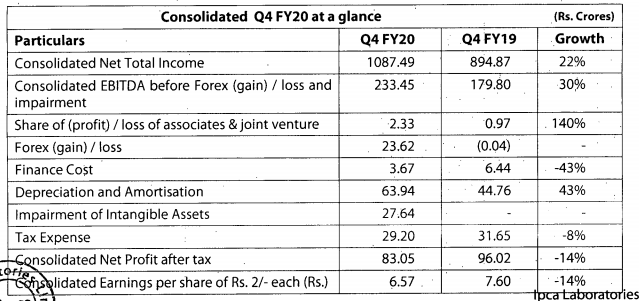

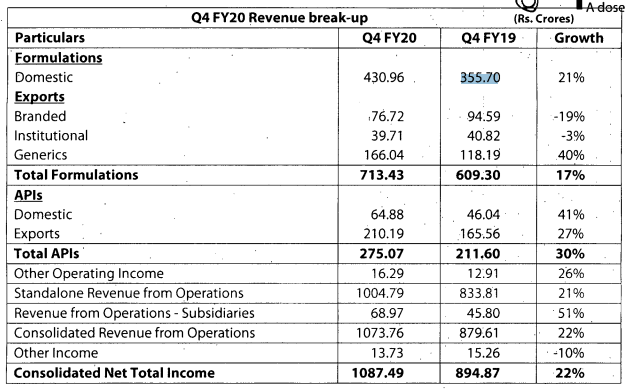

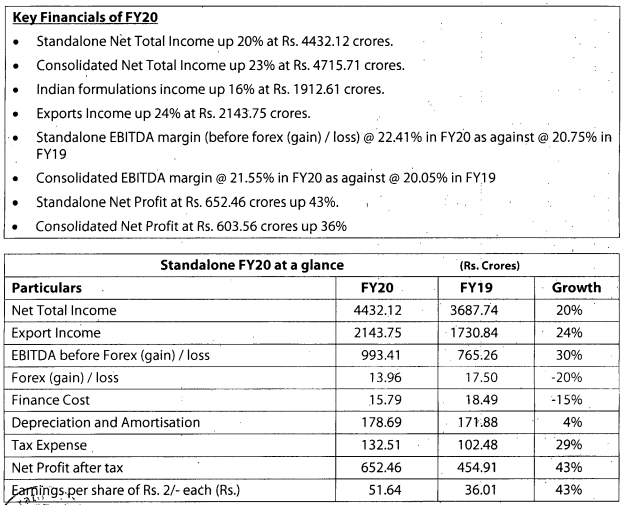

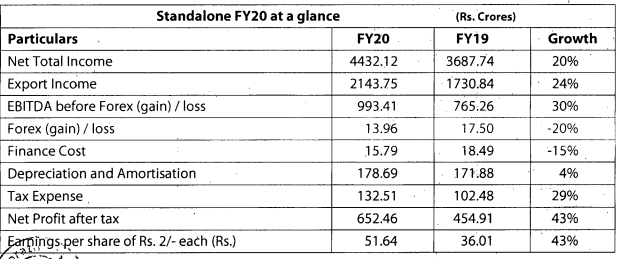

Q3FY20 Results

Good set of results. Domestic and export markets clocked good growth YOY.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/50af3436-169c-4892-8825-ab841aa6c829.pdf

The management clarified on the concall that Noble has around 1100 acres of freehold and leasehold land. The company has been shut down since 2006. The main intention of buying the company is to acquire the land for setting up capacities for intermediaries for APIs that are currently imported from China.

Capex for this could be 200-250crs in FY21 provided the company is able to get environmental clearance.

The other key takeaway from the concall for me was that there has been no progress on the US FDA approval front.

API growth has been very strong and the company expects a more muted sales in Q4.

8 Likes

-

USFDA has made exception to the import alert for the IPCA’s following APIs and formulation -

- Hydroxychloroquine Sulphate API

- Chloroquine Phosphate APl

- Hydroxychloroquine Sulphate Tablets.

-

Several credible articles / reports / research papers claiming prophylactic as well as treatment potentials of Chloroquine Phosphate and Hydroxychloroquine Sulphate formulations in managing/treating Coronavirus Disease (Covid-19), though these drugs are not approved for treatment by any regulatory authority.

-

Ipca is noticing an increase in the emergency demand and inquiries for the Chloroquine Phosphate and Hydroxychloroquine Sulphate APls and its formulations from several countries world over. Foreseeing this increased demand, Ipca being amongst largest manufacturer, vertically integrated with capacities and capabilities for manufacturing of these APls and its formulations, is gearing to manufacture and supply these products meeting the stringent cGMP, quality and regulatory requirements and thus help mankind in the best possible way in these testing times.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/af31e003-575e-4550-b6f2-c1340aec82e9.pdf

12 Likes

“Mr. Trump said he also had spoken to Prime Minister Narendra Modi of India about procuring millions more doses of hydroxychloroquine from that country.”

2 Likes

The antimalarials is around 6% in the pie, domestic pie, and degrowth by around 4% and for first 9 months of current year, there is around 4% growth on that.

And almost around 8 to 10 top API, we have large amount of integrations announced on your intermediate side, but there dependence is still there on China as far as the key starting materials are concerned, we hardly import any kind of API from China. It’s basically we used to import some key starting materials and some chemicals from there

Normally, we don’t talk of each intermediate wise, but the overall business-wise, I can talk because a lot of key starting materials come from China. And that dependence is there because practically everything comes from China. So that dependence is there, and we like to reduce those kind of dependence in time to come and the R&D is working currently, and this Nagpur Wardha site will be one where we will start producing but it’s almost around 2 years away. As far as this coronavirus issue is concerned, we have currently, the available intermediates with us, which can take care up to April of the next financial year. But supply has to start coming somewhere between mid-March, so that your May production is not hampered. So we are continuously in touch with wherever we could establish contact. So somewhere the production factories were, again, restarted and all. But logistic issues, supply issues, still we have to get the answer. But hopefully, maybe I think maybe around next 15, 20 days, a lot of more clarity will emerge on that side. And I don’t think so that too much of disturbance will be there as far as supply lines are concerned.

Taken from their concall. 1. whether product mix can be changed quickly to ramp up from 6%.2. How do you expect Chinese to supply key API.

Pharma experts need to find out which co can without Chinese dependence to do this. Apart from cadila, we have Dr Reddy, APLLTD but key answer whether manufacturing and supplies can be made. Then only sales can come. Can DIVIS supply the key RM. The share price has gone up on hopes .If hopes don’t turn reality, the fall can be big.

1 Like

The news articles does not answer the key questions. This is the place where we retail are handicapped. We cant access data and then how do we decide. What are the key questions to be answered?

- What is the production capability - what is key ingredient required, where it has to come from, if yes what is the price, ratio of dependence (inhouse to Chinese), inventory ,etc

- Pricing power and whether they will make profits as the key RM price will shoot up and buyers are Govt. and it is in a crisis.

Going by the above, I don’t think this situation can help IPCA/Zydus to improve its margin and one should invest based on this. Import alert was never there for this hydrosulphate ( again wrong news).

However, it is a good investment in terms of valuation and the technical model I follow. I entered this stock based on that long before this fall. If this situation turns out good, it is bonus. So my conclusion, retail need to work on a combination of fundamentals and price action as their access to data is limited. Just based on good financials, one cannot decide on investment . Business is more important than DCF,etc. Excel can produce any number of values you want. Pl see this link also how PA helped me to enter long back

2 Likes

This limits upside for IPCA going forward.

Disclosure - under watch

The story in ipca is that their domestic business is like an FMCG company. It is a cash cow for them.

2 Likes

4 Likes

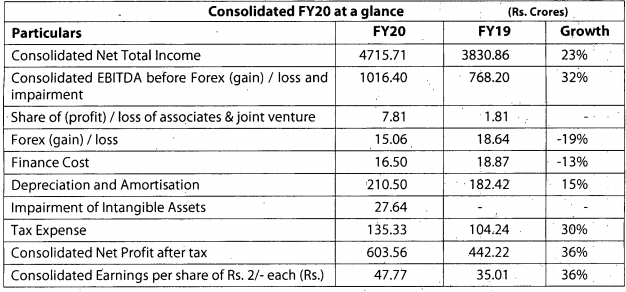

Ipca

Conference Call Highlights

Forex: FY20 – loss | 14 crore; Q4FY20 - loss of | 21 crore

Therapy growth rates for FY20 are- pain: 20%; CVS & diabetology: 10%; anti-malarials: 7%; antibacterials: 35%; CNS: 20%; ophthalmic (newer): 38%

The management will continue to focus on improving productivity, asset utilisation and brand building

Gross margins decline in FY20 due to increased input cost and higher API mix (~27% of revenues)

The company has guided for | 250 crore of capex in FY21 including solar/wind power initiatives. Most of the capex (excluding maintenance capex) is contingent on Dewas API plant environment clearance, which is expected in early July 2020.

Dewas: 2-3 plants to come up; FY21 capex to be | 50-60 crore for civil work at Dewas; operational in FY22/23

FY22 Capex to be ~| 200 crore

Branded formulations export came in at | 77 crore in Q4FY20 vs. 94 crore in Q4FY19 (| 26 crore of shipment deferred to Q1. In FY20, Branded formulation grew 6% to | 381 crore (12% adjusted for deferred sales)

In FY20, Europe sales grew 31% to | 319 crore; SA grew 15% to |110 crore and Canada grew 59% to | 78 crore.

Subsidiaries:

Onyx (UK – CRAMS) – | 18 crore profit in FY20 (Revenue US$8 million);

Baysure (acquired for front end US) – currently in trading business (Profit contribution: US$ 0.2 million);

Pisgah (acquired for CRAMS front end at UK) – Currently loss making due to delayed projects and loss of out-licensing royalty due to drop in market share (impairment of | 27.6 crore taken)

FY21 Guidance– 14-17% growth in revenue and EBITDA margin improvement of 150bps

11.5% growth expected in domestic business; API continue current trend

Institutional business may reach | 240 crore from the current | 176 crore

No MR addition for FY21

R&D spend for FY20 was at 2.5% of sales

Remedial – | 16 crore FY20 (Q4FY20: | 3 crore); Going ahead, this cost will come down

On the Hydroxychloroquine front – capitalised on opportunity due to Covid-19 in January/February 2020

12 crore tablets supplied to the government in 45 days with a realisation of | 42 crore

Captive API consumption at 55% in FY20 against 54% in FY19

Tax rate for FY21, FY22 to be around 17.5%; post that move to the 25%.

3 Likes

Ipca lab

Highlights from management commentary

COVID-19-led CQS/HCQS sales stood at INR2.6b for 1QFY21.

Overall sales are expected to grow 18–19% YoY in FY21, with 10–12% growth in the DF business, a 20% YoY increase in API, and better opportunities in Export Formulations. Gross margins are expected to expand 100–150bps YoY in FY21 on lower raw material cost and a product mix change.

Overall, operational expenses are expected to grow 5–6% YoY in the near term.

With environmental clearance in place, IPCA would commence construction at Dewas post the monsoons; it intends to spend INR2.5–3b capex over the next 15M to expand API capacity.

1 Like