Hi, does anyone knows if there is any bad news for iON exchange? I wanted to see if it is a good opportunity to buy the stock or something is getting changed in the fundamentals? Just curious to know. Personally i am bullish that water treatment companies has opportunity to grow. Not sure if iON exchange is aggressive enough to grow at good pace or it will be conservative growth. I was hearing their last con call and management doesn’t seems to be aggressive and they want to grow slow.

@dineshssairam what are your thoughts?

Disc- invested

I don’t think anything has changed fundamentally. In fact, if one were to believe in rumors, VA Tech Wabag is between a rock and a hard place in terms of Working Capital. Any new project that they are unable to take on due to this is an opportunity for others (Of course, not necessarily Ion Exchange alone).

Regarding Growth, the management seems to be guiding 20%+ PAT Growth at least for the next 3-4 years. But I would be happy with 15% over a longer period too. Water Treatment isn’t really an industry where one has to ‘move fast and break things’. There is enough opportunity for everyone. The winners will be the ones who optimize their capital allocation strategy for the upcoming surge in demand.

3 Likes

Hi @dineshssairam Thanks for your comments. I agree that there is growth opportunity in water treatment as we have scarcity of water and govt focus is also on making drinkable water available to everyone. We have many states having villages where people have to travel far to get water or govt send water tanks. Lets see how iON exchange use this opportunity.

Results are too good

https://www.bseindia.com/xml-data/corpfiling/AttachLive/046e4106-5735-4b39-9b8d-20b5b254d098.pdf

67% Topline Growth

79% PBT Growth

121% PAT Growth

If someone can build a similar table like I did for the previous results (Segmental numbers are also in the results), I would be grateful.

On a quick look, I can see that Engineering has done exceptionally well and Chemicals has taken a backseat (In comparison), which is surprising. Consumer Division is still reeling from losses. I don’t think turnaround is happening like the management promised. Good thing is, Capital Employed for Consumer Division has come down a lot too.

14 Likes

detail analysis by a blogger

Investor presentation for HY 2019-2020.

1 Like

5 Likes

Q2FY20 Concall: Stream episode Ion Exchange Concall (Q2FY20) by dineshssairam podcast | Listen online for free on SoundCloud (Q&A starts at exactly 10:14)

This concall was relatively boring, in the sense that most questions circled around near-term targets, segmental break-up and so on. Here’s a summary:

- Order Book: Rs. 1454 Crs (Out of which Srilanka order is Rs. 698 Crs)

- Bid Pipeline: Rs. 5000 Crs (Whatever happened to the additional Rs. 1000 Crs? In the last concall, bid pipeline was pegged at Rs. 6000 Crs). 30% of this would be Government Infra projects.

- Some significant large orders are in the talks (Like Srilanka order, maybe a little lower). But the discussions have not reached a conclusive stage yet. Announcement to follow.

- New Membrane opportunity. Ion Exchange is the only player in India, but are currently in the process of building capacity. Opportunity size is Rs. 400 Crs in India. Export opportunity is also there. On a full capacity basis (Once the Capex is done), the company can capture 25% of the Indian market.

- Rs. 50 Crs this year + Rs. 50 Crs next year Capex planned for Resins and other Chemicals. Announcement to follow later. Resins market size globally is “a few billion dollars”. Chemicals market size globally is “a couple of billion dollars”. 35-40% Indian market share in Chemicals, but significant portion of the business is Exports.

- 50% near-term consolidated Growth guidance maintained.

- Margin improvement likely because of increase in scale of operations.In another question, they said the huge increase in Margins over the years is also largely because of the scale they are operating at now.

- Chemical division is in part growing a lot on account of environment norms in China (Mentioned in the last concall too).

- Water Treatment chemicals have significant entry barriers. Ion Exchange to focus on the higher-end new and innovative chemicals. Lower-end of the market (Commodity Chemicals) is highly competitive. Double-digit near-term growth guided for Chemicals division.

- Consumer division: Focus is on volume growth right now (Looks like it’s been the focus for about 6-7 years now

). No significant change in product mix. EBITDA break-even by end of the year! Profits to be generated ‘conservatively’ by next year.

). No significant change in product mix. EBITDA break-even by end of the year! Profits to be generated ‘conservatively’ by next year. - Ion Exchange usually takes up small orders. But large orders are expected from Government agencies and others. The company is actively pursuing that opportunity. If even one such big order is landed in a particular, it will be beneficial.

- Treasury share de-classification has no impact on the business. There is no compulsion to sell these shares, except the de-classification to non-promoter non-public according to SEBI rules updated in 2019. A follow-up question was if Promoters would purchase more shares from the open market. Now we know the answer to that question.

- My question is around the 53:00 mark. It was about the opportunity from GOI (Nal Se Jal, Jal Jivan), whether the company is actively pursuing it and how it will be handled strategically. The response was that the company always makes sure that the Margins and WC terms are favorable to them and the same applies to all types of orders, including GOI/Municipal orders. Contracts that do not allow this flexibility will not be bid for. But the management reiterated that better quality orders are seen on the market. A follow-up question was about the RailNeer opportunity, but that one received a generic response.

16 Likes

Hi @dineshssairam Do you know why margins are low for Ion Exchange? I saw the quarterly results. Revenue have increased. But so as expenses. Margin are still 6-7%.So wanted to know your thoughts.

Margins in the Engineering Division can vary a lot depending on the project delivered for that quarter. This quarter’s Sales was largely from Engineering. So one can assume that some low Margin projects may have been delivered.

But I don’t understand why you’d consider 6-7% Margins as “low”. That’s pretty much the standard for the industry. Surely you wouldn’t expect a dairy company to have the same Margins as a FMCG company. It’s all relative.

4 Likes

Thanks @dineshssairam. I know comparison to different industry is not apple to apple comparison. I was just trying to understand reason of 6-7% of margin.

Hi, reg. treasury shares, how to look at them? Don’t shareholders have a part in it, given it is tsy? It seems like the Tsy shares have been sold, and that money is used to buy shares by promoter. And also, as the trust was for employee benefit, only current promoters got that? Basically, who got the money by the Tsy shares sold, and dont we as shareholders have a part in it? Thanks.

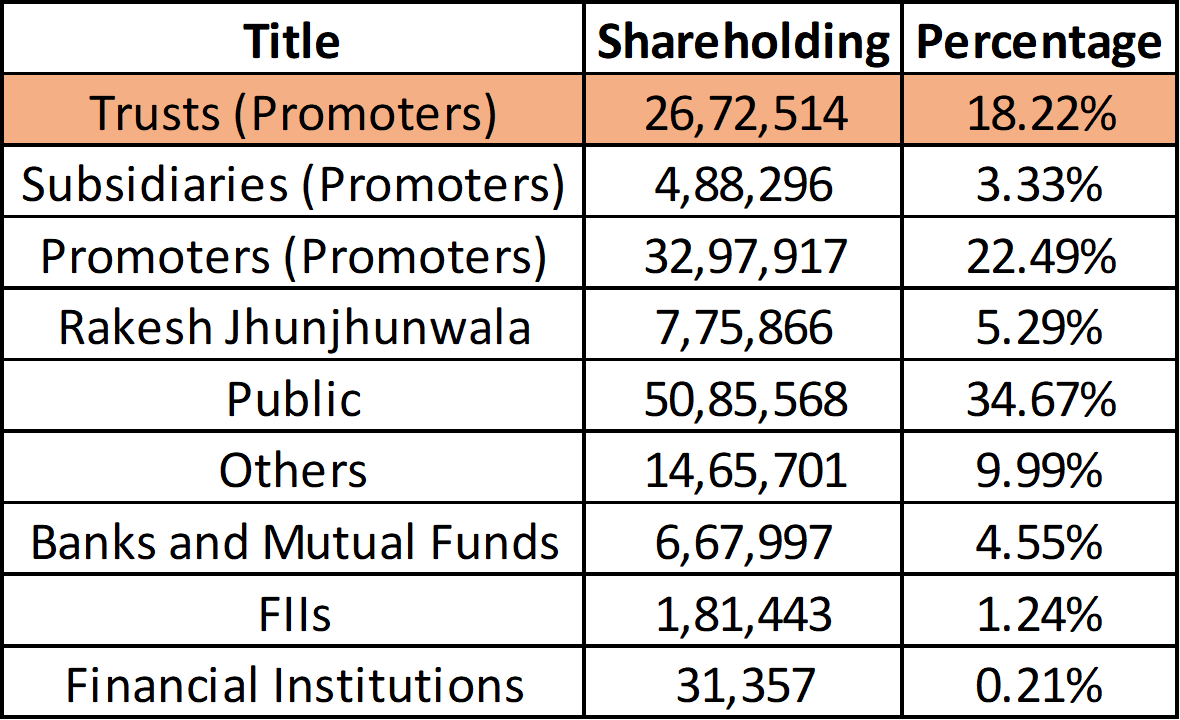

As per the latest Annual Report, IEI Shareholding (Staff Welfare) Trusts held 2,662,914 Equity shares (About 18% of the outstanding Equity Shares). Some small discrepancy exists when compared to what’s reported on different sites online, but we can let that slide.

Although you may be confused by the terminology ‘Treasury Shares’, these shares are essentially ESOPs, largely issued to Directors and some employees. There was a lot of resistance from the shareholders when this was happening, as they felt the allocation was too high (By FY08 when these allocations were stopped, they were worth about Rs. 36 Crores):

In other words, IEIL Promoters hold ~23% of the company and they also hold 18% of the company indirectly via the Trust (Along with some employees) and ~3% via Subsidiaries, taking their total shareholding to 44%. The highlighted part below is the shareholding in question:

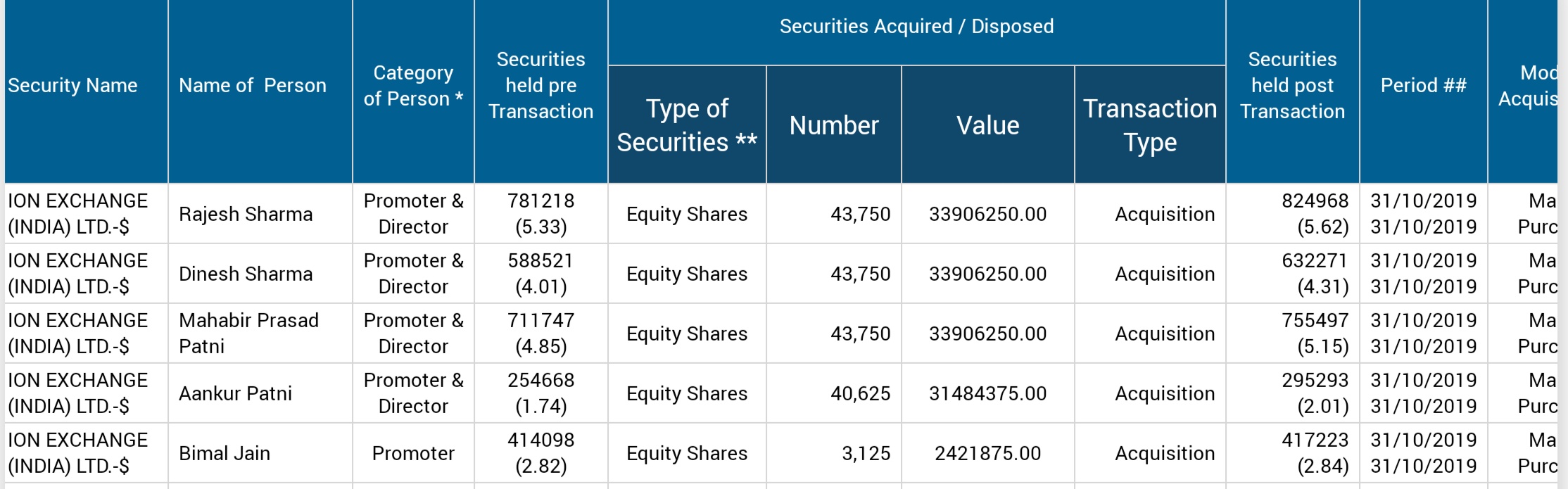

Recently about 175,000 of these shares have been sold by the Trusts and the same has been brought by the Promoters and Directors. This is because of some SEBI rule directing companies to classify shares held by Trusts as ‘Non Promoter, Non Public’.

What’s interesting is that the management said in the concall that although the category reclassification was done, there was no compulsion to sell the shares. But it would seem that IEIL is interested in slowly converting them back to Promoter shares. Will they do it for all the shares held by Directors? We will have to wait and see.

TLDR: It was a bad move to issue so many ESOPs back then. However, these type of ESOPs are no longer being allocated since 2008-09. It seems like the management is interested in converting this convoluted holding structure into a more direct one.

3 Likes

NO, Dinesh. So these are 2 separate issues here - one is the ESOPs allotted between FY01-08, and another is the shares lying in the IEI Trust (this is from 1984).

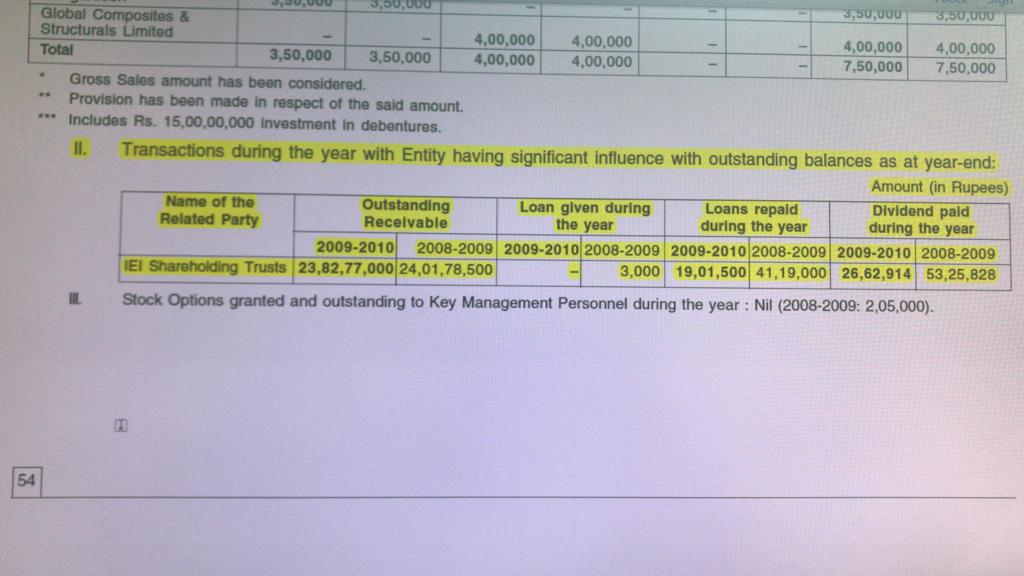

Back in 1984, one of the investor/promoter then wanted to sell his/her stake. The employees of ION then (Mr Sharma, Mr Patni, etc - who are the promoters now) bought that stake out. This was done using ION’s money (as debt to the trust). ION gave out a loan of 20-25 crore to the IEI Trust. This money was used to buy the shares/stake from the ‘1984 promoter’. It seems that this was an interest-free loan of sorts (re-repayment of the loan was usually lower than the dividend received by the trust) and in the range of 10-20-40 lakh per year! Attached a screenshot from FY10 AR. (Unfortunately, sounds similar to what Meghmani did last year)

My sense is, the trust will sell some of the shares (like they did now), repay this 20-25 crore loan to ION, and thus the transaction stands to complete.

So, majorly - the employees then, promoters now (Mr Sharma, Mr Patni, etc) - their stake in the company has been built by issuing huge ESOPs to themselves and by using ION’s cash (as a loan to the trust) to buy shares in the trust.

16 Likes

Do you have source for this? For now, I am taking this at face value. Would love to research it more.

The problem is, Ion Exchange was a subsidiary of Permutit (UK) until 1984 and became wholly owned in India only by 1985. Perhaps the ‘Trust’ was formed only back then and Permutit might have decided to give low-cost loans to it.

Of course, I am just guessing all this. If you have a proper source for the loan, that would make thing clearer.

If they are doing this just to close the loop, why purchase the shares directly once again? Essentially, the stake bought out from the 1984 promoter (Using low cost Debt of Ion Exchange like you say - we will have to look at that closely) is now being sold out of the convoluted holding structure and being brought back by the Promoters directly.

In all, it looks like:

-

The ESOP allocation was high / unfair to existing shareholders and it also created a convoluted holding structure. The 1984 Promoter shares is also part of this. We need to understand if there is an effort towards correcting this structure (Which I think is happening). The formation of the Trust in the first place might have been related to Premutit selling its entire stake.

-

The issue of low cost loan to the ‘Trust’ is a different question, which needs further research. Again, I doubt this may have something to do with IEIL becoming wholly owned in India.

In any case, the allocation of huge ESOPs to the promoters was in bad taste. The management seems to defend it by saying that it was required to retain employees at the time. Even if we call it bad water under the bridge, the question of whether the convoluted holding structure will be corrected remains.

They mentioned this at their AGM, or also if you get a chance to meet them in person. Maybe you can check this with them on the next con-call.

Do check the screenshot that I have attached.

Abhiram Seth, an Independent Director of Ion Exchange, has bought 76,050 shares in Ion Exchange on 20-12-2019, a transaction valued at Rs. 5.63 Crores or ~0.52% of the company.

From the Annual Report:

Mr. Abhiram Seth has more than three decades rich and varied professional experience in the area of sales and and marketing including exports. Mr. Seth worked for Hindustan Lever and Pepsico India. He was the Chairman of Water Committee of FICCI and Food Regulatory Committee of CII and currently is director on the Board of various other Companies.

Also the cleaning up of the convoluted holding stricture continues in the earnest:

12 Likes

@dineshssairam - Looks like the shares bought by Abhiram Seth are sold by the trust so it is just a change of hands among the promoters.

If this is true then this is not insider buying right? This is just to comply with the regulations.

Disclosure: Tracking, Not Invested

1 Like

There is no regulation to comply with. But the current holding structure is convoluted and the re-classification to non-promoter shares is a hitch.

Either way, I welcome all signs of shifting towards a more direct holding structure.

1 Like