Dhruv,

This is a brilliant and logical analysis. Very thorough and gets to the core. Like I have mentioned from my industry experience, they seem to be buying business… As shown in their DSO position and low AMC (when a product company needs to push hard, they will reduce the license costs and AMC comes down as a %). This is expected since IDA is a new entity and has to establish a base. But what worries me most is how they have spread to 14 products… Highly unusual in this industry. Particularly at the early days of growth… And that’s why so much equity dilution.

Disc- I remain invested in a small way. It is the classic Indian product company Frontier that I’m interested in…

Gary temenos clocked in 223 days DSO as I mentioned in the post. Theyre now down to 123. And yes, most companies in this vertical seem to have domain expertise in one product - temenos for consumer, mysis for corporate. i agree that intellect have spread themselves too wide and too soon. need to monitor how capital requirement moves in the next year.

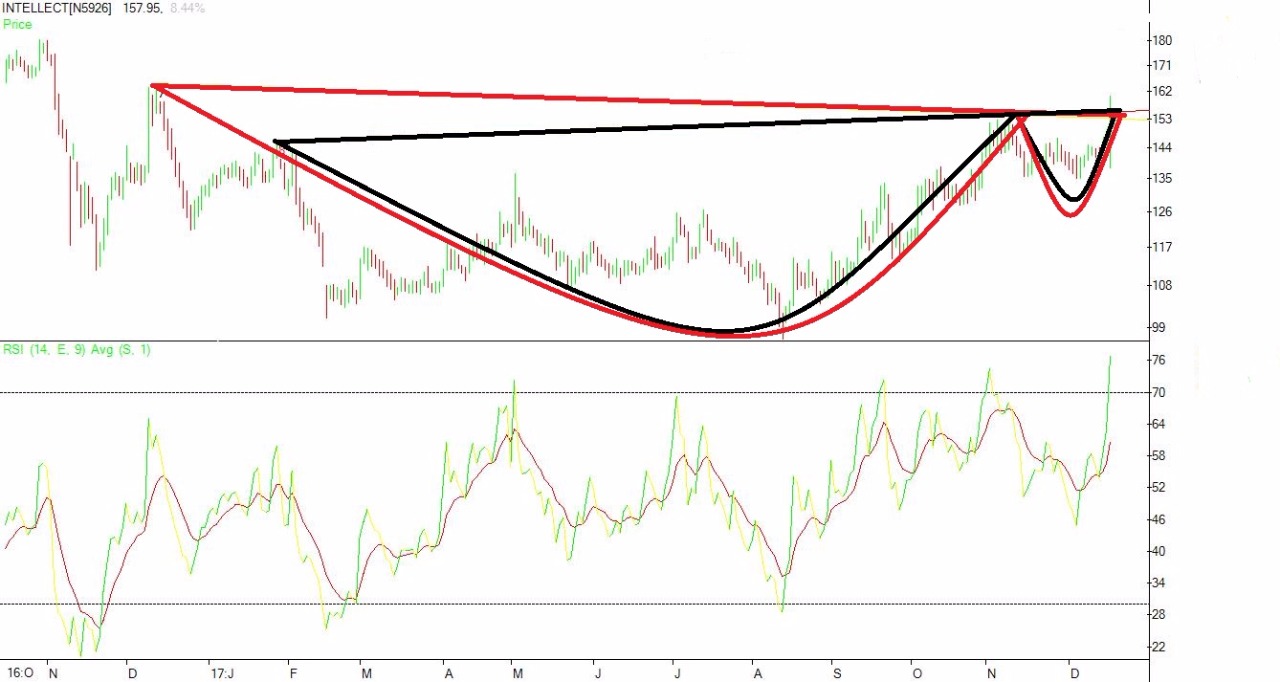

Finally after a year long cliffhanging game it finally raises some hope and feels like a company. Hope management delivers in coming quarters. It has potential to reach back its 52 week high means investors and deep pockets getting in and believing in turnaround of the business.

Company has exceeded market expectation. But at current price is fairly valued. Opportunity window is surely opening up. It is a long term hold as of now

Intellect has done well recently to both continue the growth momentum and recently won a large deal as above. Ofcourse valuation on a price to earnings multiple is very high. Any insights on how to value product companies which have potential non-linear growth would be appreciated.

Given profitability is currently depressed by product investment etc. EV/ Sales might be a good way of comparing against peers. I think Oracle Financial is c.7x, Majesco is 1.8x odd and Temenos is at 15x odd. IDA itself is 2.4x odd.

Thank you Nprao. Did you add debt to Market cap and took out cash equivalents to calculate EV or is that directly available at some source? Please let me know.

Interesting press release. They are saying iGTB will treble revenue by FY21. They reiterate group revenue CAGR of more than 21%.

According to slide 7 in above presentation iGTB generated Rs 459 crore of revenue in FY18. So they are implying this will rise to about Rs 1400 crore in 3 years.

iGTB grew revenues by 34% in FY18. We know group revenue was up 19% in the same year. This means Intellect excluding iGTB must have grown at 10%.

Assuming iGTB trebles in 3 years and the rest of the business continues to grow at 10%, then the ‘more than 21% CAGR’ Intellect is referring to should actually be closer to 26%.