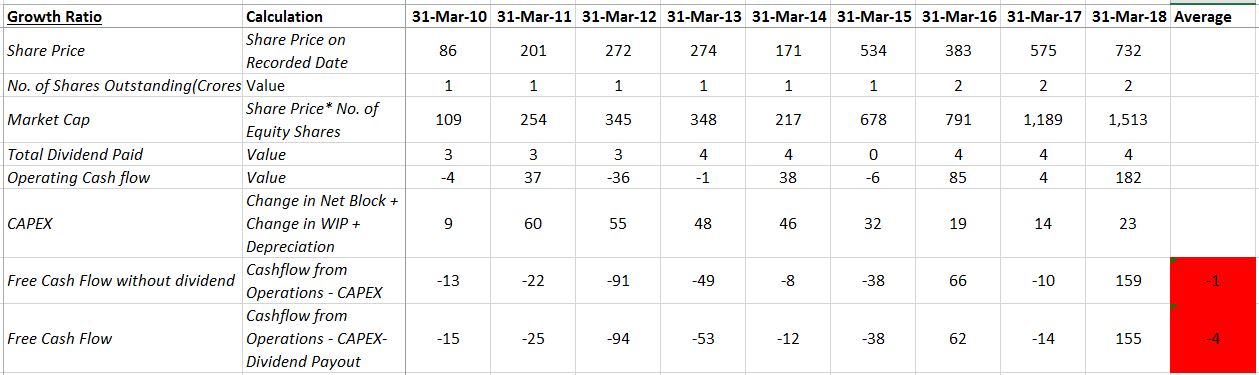

While all sounds good (including the R&D, new product launches, positive sales and PAT growth), the red flag at the moment appears to be the generation of ZERO Free Cash Flow by the Company over the period of last 9 years.

If the sales and/or profits are not translating to cash despite revenue growing from 250 crores to 1100 crores+, appears to be a cause of concern.

Moreover, the business is cyclical in nature and depends a lot on normality of monsoon season coz company derives ~40% of its revenue from Jul-Sep quarter. Considering the volatility, working capital is required to maintain inventory which is reflected in the financial numbers of annual reports.

Considering that UPL Limited also caters to crop protection segment, it generates huge free cash flows.

Could not comprehend why Insecticides does not have the same trend.

Disclosure: Not holding