IndusInd Bank Q3 concall -

Advances-2.72 lakh cr, up 19 pc yoy

Deposits-3.25 lakh cr, up 14 pc yoy

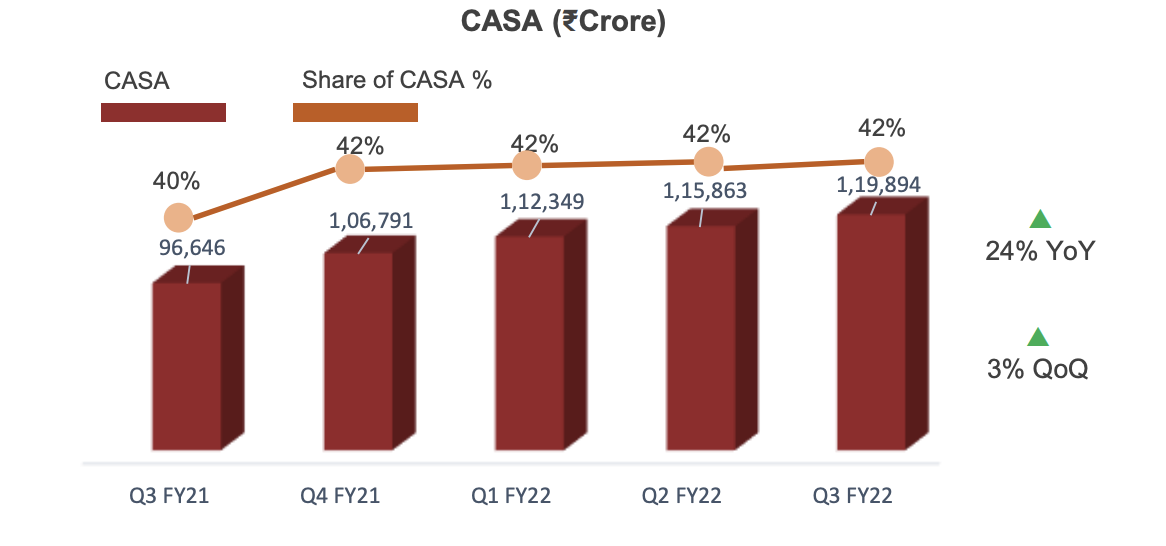

CASA-1.36 lakh cr, up 14 pc yoy (encouraging)

NII-4495 cr, up 18 pc yoy

Fee Income- 2077 cr, up 11 pc yoy

Operating Profit - 3686 cr, up 11 pc yoy

NP- 1964 cr, up 58 pc yoy

NIMs-4.27 pc

RoA-1.87 pc

RoE-15.23 pc

Cost/Income-43.91,down 232 bps

Gross NPAs-2.06 pc,down 42 bps

Net NPAs-0.62 pc,down 9 bps

Restructured assets -1.25pc,down 205 bps

Loan book composition-

Large corporates-27 pc

Mid Corporates-16 pc

Small Corporates-4 pc

Consumer bank-53 pc

Consumer banking breakdown - Vehicle Finance - 26 pc ( Bank’s Niche )

Micro Finance - 11 pc ( MF percentage is high as Bharat Finance was acquired by bank 5 yrs ago )

Non Vehicle Finance - 16 pc ( includes LAP,Credit cards, Business banking, Personal Loans etc )

Vehicle Finance book at 71k cr, up 18 pc yoy

Micro Finance book at 29k cr, up 8 pc yoy ( avg ticket size of Rs 30k )

Corporate Loan book at 1.27 lakh cr, up 20 pc yoy

Yield on Assets- 8.65 pc

Yield on Advances - 11.51 pc ( corporate yield at 8.2 pc, retail yield at 14.3 pc…due contribution from MFI book)

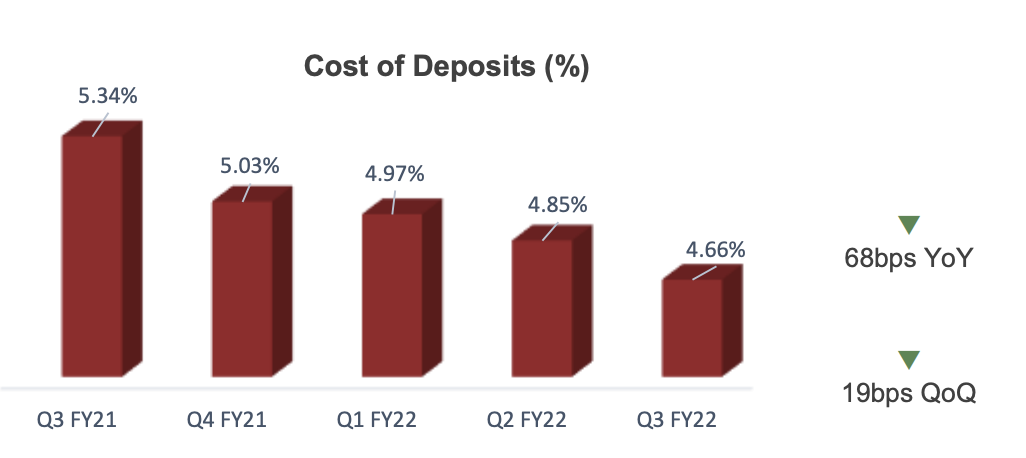

Cost of Deposits - 5.10 pc

Cost of Funds - 4.41 pc

NIMs - 4.27 pc

Gross slippages in Q3-1467 cr (which is about 2 pc annualised, fairly ok)

Non Vehicle Finance book at 44k cr ( Credit card, LAP disbursement up 46 pc, 10 pc yoy )

Total Provisions at 130 pc of Gross NPAs

Total Branches at 2384 vs 2103 yoy

Bharat Finance branches at 792 vs 825 yoy

Micro finance lending picking up pace wen Dec 22

Started disbursing Home loans for the first time in Q3. Disbursed 200 cr during the Qtr

Went live on Income Tax portal in Q3

Share of top 20 customers in deposits down at 15 pc vs 17 pc, qoq pointing to increased granualrisation of deposit base

Aim to close the year at 2450-2500 branches

Mobile app user base up 26 pc yoy

Hired 1800 employees in Q3 while maintaining healthy cost/income ratio

SMA1 and SMA2 books at 8bps and 24bps ( very healthy levels )

CRAR at 18.1 pc ( including 9M profits )

Guiding for a loan growth of 20-22 pc in Q4

Restructured book trending down QoQ at rapid rates

Bulk of Corporate book is floating book. Bank reprices it every Qtr

Exposure to Idea-Vodafone at 1700 cr. 900 cr out of this has already been provided for

Carrying surplus liquidity to the tune of 45k cr. Aprox 25k cr out of this is held as G-Secs

Aim to keep carrying 20-25k surplus at all times as a matter of prudence

Current yield on newly introduced housing loans at 8.95 pc

Disc : Holding, Invested

) that is long written off.

) that is long written off.