This thread seems to have gone cold. I was wondering if the massive tariff cut on GSPL will have some negative impact on IGL as well. Does IGL also operate High-Pressure (HP) pipelines that could be impacted by similar tariff cuts?

I recently started studying IGL - got interested in it after the fall it has seen due to the Delhi Electric Vehicle policy and also the reduction in gas supply via the Administered Price Mechanism (APM). I only have a small position and have been thinking if I should scale up. Personally, I think EV impact is overstated. Further reduction in APM might be a challenge but that will apply for all CGD players, so at an industry level, my sense is it may not impact much as I expect they will pass on the cost increase. However, I am less clear about the impact of this regulatory decision. Given their NCR monopoly is over, if this price cut will happen to their pipeline infrastructure, then it will be a double whammy, no? Can someone provide additional clarity? Thanks!

Based on this interview, it looks like GAIL may also see a downward revision in HP pipeline tariff in the near future. That will bode well for IGL which receives its gas from the HVJ pipeline of GAIL. However, it is quite possible that the regulator may also ask IGL to share their city pipeline infra at lower cost if another player starts operations. I can’t seem to find any information about potential new CGD entrants in NCR. If someone’s tracking this and has some idea, please do share.

Out of 8.33 MMSCMD around 75% is contributed by CNG and remaining from PNG. Delhi government has issued notice to Cab aggregator companies to convert their cars to EVs in a phased manner. By 2027 100% of cars need to be only EVs. This will create a lot of pressure in terms of volume to IGL

Thank you for the reply. I believe the EV policy date for Delhi is by 2030, and not 2027. However, my assumption on volumes is based on 1) IGL’s own growth forecasts for gas sales, they expect to end FY25 at 10 MMSCMD 2) Conversion of inter-state transport and possibly, other heavy vehicles (IGL talks about dumpsters) to gas 3) Chances of EV transition being slower 4) IGL expansion to other geo areas.

That’s my rationale for being a bit more sanguine about volumes. I could be wrong, of course. However, I am less convinced about price/margin pressures. I would love to get some perspective on that.

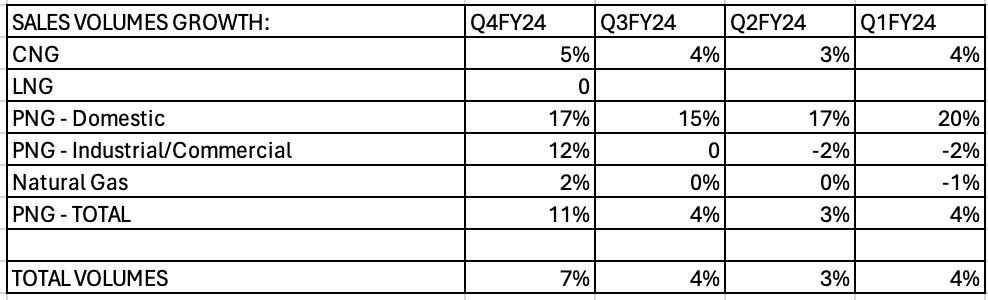

Initial reaction to Q4 results - a mixed bag, but more negative than positive given they had guided for better numbers in the Q3 earnings commentary. Volumes were up, but lower than expected. PNG growth (both domestic and industrial/commercial) has been quite good QoQ, and domestic growth has been particularly strong YoY. CNG growth is steady - the good thing is they are still growing here despite the headwinds around EV adoption.

However, clear margin pressures seen across both CNG and PNG. EBITDA margin down 1.2% QoQ and EBITDA per SCM was only Rs. 6.58, much lower than the Rs. 7.5 they are targeting for FY25. Given CNG prices were cut in March, chances are it will fall further in Q1 FY25. Haven’t listened to the earnings call yet - wonder what was the reason for this fall in Q4.

While valuations are ok, some more caution warranted here, I guess. Not clear to me what is the growth trigger even if margins bottom out in Q1.

Got around to listening to the earnings call, and there were some one-offs in Q4 Opex that led to the lower margins. That was good to hear. Not much has changed materially. They still expect to achieve 9.5 MMSCMD on average in FY25, mostly driven by new GAs CNG sales in commercial segment, and Industrial/domestic growth in older GAs. LNG and CBG sales will also contribute and possibly offset the CNG sales loss to EVs. The EBITDA per SCM range shared was quite broad - between Rs. 7 to Rs. 8.5. I am guessing it’s because APM allotment continues to come down and it’s hard to predict spot price which in recent years has fluctuated wildly.

Overall, it was a reasonably positive update in my opinion. If gas prices stay low, the stock should do well, given the reasonable valuation. I don’t foresee much of a downside risk unless there’s some major policy change (always possible) or unexpected competition (seems unlikely as of now).

Disclosure: I am invested, may add or reduce anytime. I am not making any recommendations here. Just sharing my thoughts.