It looks like KKR has taken control of the board of the investment manager. See Press release.

Can this be a safe bet for a retired person present post tax yield being around 10% when interest rates are going down. At least it can be part of debt portfolio though it is not debt if you call so in strict sense . What can go wrong in the medium term. Request guidance from seniors.

Disclosure Bought one lot one month back

1 Like

Hi,

I am not a senior but have worked in this sector I will share some thoughts. Seniors please correct if I am wrong.

There are three main risks for this asset.

-

Operational Risk: Transmission is the middle part of the whole electricity sector (Generation to Distribution) and also the strongest financially. Generators face high debtors issue and distributors face collection issue, but generators and discoms have to pay in advance to PGCIL to offtake the load. From my experience, private IPPs have to pay in advance for transmission, not sure about state gencos but I believe it is the same. Then PGCIL distributes the monies to transmission companies based on availability of the system (asset). As per Indigrid’s report they have maintained 95%+ availability till now, so this risk is minimum. Further, increase in renewable assets increases the need of transmission to different parts of India.

-

Financial Risk: Debt to AUM ratio is below 49% as someone mentioned above. The older debt is also raised at competitive rates and we are in a downward trend for interest rates. So this risk is not significantly different than other companies in this sector.

-

Regulatory RIsk: I believe this is where the most risks comes from. Power sector is knows for haphazard knee jerk regulatory changes. Currently, low cost power (agriculture) is subsidized by industry and retail consumers. Discoms and power companies are under lot of stress, if the govt feels they can milk the transmission sector they will. Many times Govt has changed / scrapped power purchase agreements (PPA) with generators, the same can happen here.

I am not sure how to factor this into the returns.

4 Likes

Thanks Mr. Parth for clearly explaining all the points and giving your valuable opinion based on your personal experience.

I think in the medium to long term main risk is from change in Government policies only. But to my mind buying it at present level you get 9-10% yield (post-tax) which is fairly attractive and you get cushioned to some extent even if those risks play out in the long run and yield comes down by few percentage.

In what % among (principal,Dividend & Interest )this 90% distributable amount given to unit holder? Also, what’s the tax on each of them at the hand of unit holder?

Thanks

Disc. on watchlist

There is no specified % mix between principal, dividend and interest specified in the regulations or committed by the company. Till date, almost 100% of the distribution has been in the form of interest and I think there was only one quarter since listing where some capital was repaid to investors.

Tax treatment would be as follows:

- Dividend is exempt in hands of the investor as the company would have already paid dividend distribution tax

- Capital repayment is not liable to tax

- Interest is fully taxable at whatever rate is applicable for the investor (10% TDS is also deducted before payout of interest happens)

For further details you can refer to this link: https://www.indigrid.co.in/pdf/indi-grid-faqs.pdf

Disc: Invested

2 Likes

Regarding regulator risk - This is pure demand and supply dynamics here. You need to figure out do we have extra capacity in transmission like we have in generation? absolutely not. Even 10y down the line we would be hardly sufficient in effective transmission capacity. If the govt. is unhappy with a transmission line can they create another one? The country risk is always there but long term consequences of interfering in the transmission sector is huge and completely avoidable. Can they nationalise all these assets at some point of time? I think yes but they might have to pay at least book value and investors will protect downside.

1 Like

I think you have put forth all the risks very well.

I always wondered about another kind of risk - inflation in operating & maintenance expenses. Since you have worked in this sector, do you know if regulations have some kind of in built protection against inflation?

Hi Subodh,

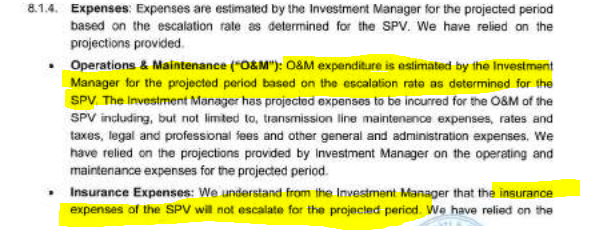

From the half-yearly valuation reports that IndiGrid is mandated to disclose, it appears that escalation in operating & maintenance (O&M) expenses over the life of the project are factored into the projections and valuation.

For instance Pg 58 of the latest valuation report has the following note on O&M and insurance expenses:

Similarly a quick glance at the projected EBITDA margins for the one of the projects (Pg 65) indicate that O&M expenses will increase while revenue remains constant, hence leading to fall in EBITDA from 94% in FY20 to 82% in FY49

The tariff for transmission projects are of two types - either a fixed return on equity or a fixed tariff - as explained in the slide below (page-not-found). In the first case I would assume that opex escalations would be built in the RoE computation by the CERC, while in the 2nd case it would be up to the developer to factor in O&M escalations while bidding for the project.

Disc: Invested

1 Like

Thanks for digging up the details.

I remember the management mentioning in the last concall that:

Your findings have confirmed this. Thanks!

1 Like

1 Like

One thing to note is the impact of interest rate reduction on distribution. Latest concall suggests that 1% reduction in their cost of funds will result in 0.8/unit increase in distribution. They would go for major refinancing in FY23 so expect some bump up then or assume it as another factor of safety for your retrurn expectation. I think we will see 2% reduction in interest rates in the next 3-4 years.

Disc: invested in family accounts.

1 Like

The MD also mentioned that out of the overall debt of Rs 5000 crore, only About Rs 2400 crore is up for re-financing in FY 23. So we won’t see the entire Rs 0.8 per unit benefit anytime soon. Unless the cost of debt comes down drastically (2-3%) and the management decides to approach banks to revise their interest rates downward.

On the flip side, history has taught us that things like inflation can shoot up drastically, with a surprise. Since interest rates follow inflation, then in an increasing interest rate scenario the trading price of Indigrid units is likely to go down.

Sharing some clarifications (shared as Q&A) on the IndiGrid structure, which I discussed with a more seasoned investor. Have not invested, yet evaluating.

Questions and some Answers

1. Why did IndiGrid InvIT price fall to Rs 88 post the IPO price of Rs 100? Possible reasons

A) Reportedly, due to institutional investor/s exiting their InvIT holdings. The instrument is not liquid, hence bid ask spreads are high. In April 2019, SEBI amended the minimum allotment for initial offer & follow on offer for publicly offered InvITs to Rs 1 lakh and multiples thereof. It is not certain if liquidity constraints of this instrument have been corrected as yet.

B) As InvITs are hybrid debt instruments, if interest rates rise, they are marked to market linked and the unit price falls. Briefly, interest rates rose in 2018, leading to unit prices to fall.

C) Possible over valuation of the underlying SPVs

2. When will capital gains accrue from this structure?

Over the long term, if cash flows of the underlying SPVs are steady and interest rates continue to soften (most likely scenario), the unit price could improve.

3. How steady are the cash flows received by the underlying SPV?

Revenue stability of these SPVs is driven by their respective TSAs (transmission service agreement), which ensures payment of stipulated tariff, subject to achievement of the normative line availability of 98% annually.

As per CRISIL Rating Rationale of IndiGrid “Cash flow stability is ensured by pooling under the PoC (point of collection) mechanism, wherein Power Grid Corporation of India (PGCIL), as the central transmission utility, collects monthly transmission charges from all designated ISTS customers (inter-state transmission system) on behalf of the licensees. All ISTS licensees are then paid their share of transmission charges from the centrally collected pool. This method diversifies counterparty risks, as the risk of default or delay by a particular customer is distributed among all ISTS licensees in proportion to their share. Despite weak counterparties, PGCIL has demonstrated strong collection efficiency over the four fiscals through 2018, signifying its high bargaining power. All of IndiGrid’s SPVs will continue to benefit from the strong collection efficiency of PGCIL and diversification of counterparty risk under the PoC pool mechanism.”

Cash flows for existing projects (FCFF – free cash flow to the firm) are lower by ~ Rs 105 cr in March 2019 valuation report vs the September 2018 valuation report.

Discussions with a power analyst however, indicate that pooling mechanism could be temporary and may not continue for the entire duration of the contract. This is a risk which needs to be checked with management

4. What is the rationale for shares being issued at a discount to new investors?

This is not clear - Rs 2514 cr equity issue was subscribed by KKR, GIC and other capital investors in May 2019. These shares were issued at 83.89 per unit, a discount to the prevailing price. This has resulted in dilution of existing unit holder’ returns.

Given overall equity post new equity infusion is Rs 5,352 crores, IndiGrid is allowed to leverage upto Rs 12,488 cr (keeping 0.7 x leverage) or in other words, can fund transmission assets worth Rs 17,840 cr. IndiGrid has stated its goal of achieving Rs 30,000 cr of assets under management, to realise this, equity will need to rise further to Rs 9000 cr so that with debt of Rs 21000 cr (0.7x leverage), this objective will be met.

5. Does the Haribhakti valuation report include the servicing of debt at IndiGrid InvIT level?

IndiGrid has issued debt on its own which has to be serviced in addition to the servicing of SPV debt. This needs to be taken into account while arriving at valuation and can affect unit holder returns. Given IndiGrid InvIT structure is rated AAA/Stable, one assumes that the debt will be refinanced and only the interest will need to be serviced. If the debt is refinanced at unfavourable terms or has to be partly redeemed, this will impair unit holder returns.

(As per latest InvIT guidelines, the leverage norms (debt to asset value) for InvITs have been relaxed to 70 per cent from 49 per cent, subject to trusts retaining ‘AAA’ credit rating, along with a track record of six continuous distributions to unitholders.)

6. How are new assets acquired? What is conversion from ROFO assets to Framework Assets?

IndiGrid has signed definitive agreements to acquire INR 11,500 crores of assets from Sterlite Power. The valuation of these new assets will determine returns to unit holders. If new transmission assets are based on Tariff Based Competitive Bidding (TBCB), which offer less attractive IRRs then the existing pool of projects, then unit holder returns can be affected.

7. Risks (What are the risks to the cash flows)

• Regulatory Risk: Power sector is known for haphazard knee jerk regulatory changes. Currently, low cost power (agriculture) is subsidized by industry and retail consumers. Discoms and power companies are under lot of stress, if the govt feels they can milk the transmission sector they will. Many times, govt has changed / scrapped power purchase agreements (PPA) with generators, the same can happen here.

• Cash flow sensitivity to tariff changes, if any

7 Likes

The other InvIT IRB InvIT is trading at 65. That’s a even steeper fall. Any idea why?

Thank you sharing this. Its quite elaborate and helpful.

Is there a combined valuation report for all SPVs or did you go through every valuation report to figure this out? Of all the points you have shared, this one stood out for me. Would be great if you could elaborate on this.

Valuations is purely based on future cashflows, isn’t it? So it will depend on the discount rate and the revenues from TSAs, which are predictable. How can overvaluation creep in?

Thanks

Disclosure: Invested.

My limited understanding is that IRB cash flows from road/toll projects are a function of vehicle traffic and toll rates or more volatile cash flows. Vehicular traffic in turn is dependent on state of the economy, turnaround time of commercial vehicles, their loading regulations etc.

In contrast, IndiGrid cash flows are through a pooling mechanism under PoC as mentioned in CRISIL rationale.

Clearly believe that this point needs to be explored further as this will determine whether investors’ exit values will be neutral/depletive/accretive

PS: Not invested, nor a subject expert, just trying to make some sense of this investment

The other thing which is relevant here is that IRB assets have shorter concession periods and dont have any residual value when the project is handed back to the govt at the end of the concession period.

Indigrid assets have a longer concession period (~30 years) and are perpetually owned by Indigrid with asset life of up to 50 yrs. At the worst, they can be sold for steel/aluminium scrap at least.

Disc: Invested in Indigrid

1 Like

Hi Subodh,

Will try to answer to the best of my ability

a) There is no combined valuation report, went through each project valuation report individually. Given that it is a scanned document, it is slightly tardy. Also, new projects post the May 2019 investment do not figure in the March 2019 report, so the September 2019 valuation report may provide more insights on how fresh funds will be used. I was guided in the analysis by a more seasoned investor. The 105 cr difference was the difference in cash flows between the two valuation reports

b) Overvaluation point - It is possible that market is discounting it at a higher rate vs the discount rate mentioned in the Haribhakti report

PS: Limited understanding and not invested

2 Likes

Thanks. I am going through the valuation reports of September 2018 and March 2019. Have only managed to read through the valuation reports of BDTCL & JTCL. Here are my observations.

The process

The valuer (Haribhakti) relies on information (TSA agreements & other documents) and projections given by the investment manager to arrive at a valuation. The valuation method used is discounted cashflow valuation. So this requires 2 things:

- Estimation of discount rate

- Predict future revenue

Then arrive at the ‘present value of future cash flows’.

Asset value is bound to decrease every quarter

In September 2018, the cash flows from October 2018 to March 2019 would be included in the valuation model. They won’t be included in the March 2019 valuation, hence there is bound to be some reduction in ‘present value of future cashflows’ i.e. the valuation.

Estimation of discount rate

The valuer uses the weighted average cost of capital (WACC) as the discount rate. The WACC is the weighted average of cost of equity & cost of debt with an assumed debt to equity ratio of 70:30.

i.e WACC = 0.7 x cost of debt + 0.3 x cost of equity

Cost of equity is arrived at by taking the risk free rate (10 year sovereign bond yield) plus some risk premium. Please refer to the valuation report for details. It came to:

- 12.44% (March 2019)

- 12.74% (September 2018)

Pre-tax cost of debt:

- 8.45% (March 2019)

- 8.37% (September 2018)

The post tax cost of debt is arrived at by multiplying this with (1 - tax rate).

The final WACC (discount rate):

- 8.24% (March 2019)

- 8.32% (September 2018)

Future cashflows

Should be predictable since the terms are laid out in the Transmission Service Agreement (TSA). Also the SPVs file for escalation of revenues whenever project costs increase. And the TSA have some escalation of revenues to take care of inflation.

Confusion

Revenue

The valuer is not consistent with how they consider revenue. For example for JTCL the revenue numbers considered in September 2018 show a very small increase every year, whereas the ones in March 2019 are almost constant.

Tax

Also the valuation report says:

The SPV is eligible for tax holiday under section 80IA of Income Tax Act.

Such tax holiday shall be available for any 10 consecutive years out of 15 years beginning from the date of COD.

The COD date is in 2014, however the forecasted cashflows show tax for every year of forecasting. Why is this not being taken into account? What am I missing here.

Different WACC for different SPVs

In March 2019, the WACC is different for JTCL and BDTCL

- BDTCL 8.24%

- JTCL 8.30%

I fail to understand why. They were same (8.32%) for September 2018 for both SPVs.

@Revathi: Coming back to your point, since this is discounted cash flow valuation, the future cashflows in Sept 2018 are bound to be more than the future cash flows of March 2019 i.e. 6 months worth of cashflows. So this is not a point to be worried about.

4 Likes