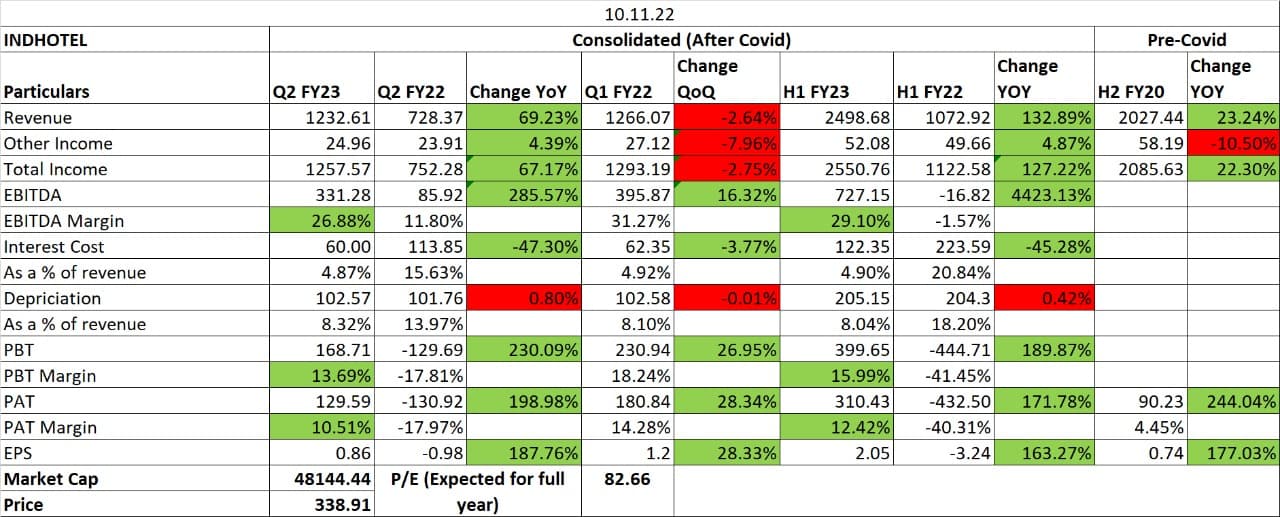

Analyzing Indian Hotels is inherently difficult even in normal times, and the pandemic has further distorted the data last three years. Here an attempt is made to compare the current fundamentals over FY20 with some back of the envelope calculations.

In the data shown above, we can see that on a TTM basis, revenue from operations is currently 1.35 times FY20 figure. Operating profits are 1.9 times with a big improvement in operating margins from 22 % to 31 %. Due to this, PBT is higher by 3.43 times and EPS by 2.77 times the FY20 figure. The company has turned cash positive from a net debt position, thanks to an equity fund raise and improved business cash flows which were double last year over FY20. I have not included operating metrics like no. of rooms, RevPAR etc. as all that is factored in the revenue and profit figures.

Looking at the macro, management says hotel demand in FY23 grew by 11.1 % and supply grew by 4.5 % Vs. FY20. In the current year, domestic airline passenger growth is flat in June 23 vs. June 19 at around 120 - 125 lac passengers per month. Overall, airline passenger traffic for August inclusive of international is still down from pre-pandemic levels. Foreign tourist arrivals are also running below the pre pandemic levels.

Thus, the improvement in company fundamentals seems largely a result of the management’s efforts at re-engineering the business model and does not factor any industry-wide / macro factors. This leaves scope for more upside on the performance.

Coming to the valuations, the Price to Book during the period has gone up from 4.40 to 7.40 and Market Cap to Sales from 3.80 to 9.80. So the stock is certainly more expensive than it was pre pandemic and is also valued more richly than others in the sector. What should be the steady state valuation of the new IHCL is not clear to me. Any views?

So far, in the current financial year till date, we have signed 18 new hotels and opened 9. We have guided in the past to open at a minimum of 20 hotels in this financial year.

We have reorganized Ginger, Qmin and Ama under a dedicated vertical of new businesses, which is being headed by Ms. Deepika Rao - Executive Vice president and Member of Executive Committee

The first 26 days of October have been very strong and we expect this trend to continue (concall was held on 27th Oct)

One analyst noted that on the international side, EBITDA is down on a Y-o-Y basis

Why occupancy wil go up further - Most of the supply is coming not in the key metros but in the outside of the key metros. So, that means that existing micro markets and key metros should be well protected and should benefit from rising occupancy. Secondly, all the demand factors like for instance FTA, foreign travel visitors, all that should help.

If new supply additions have to come, they will take 3 to 5 years to get added and by that time the demand “in theory” should grow faster than the supply would.

One analyst noted that ARR was up only 1 % in Ginger. Management said we are investing in refurbishment and renovation and RevPAR growth which was 14 % would be north of 20 % going forward. Even in other properties, this is what is giving us the ability to charge higher. there will be double digit RevPAR growth in the current year, that is not a problem at all.

Investments will be very much India centric, no intent to invest in international markets on our own money, but open to signing management contracts. Everyone is looking to invest in India. It would be foolish of us to go and invest outside.

Intent to increase stakes in subsidiaries, JVs and associates is there. Will do when the opportunity comes.

At the end of the quarter, cash is approximately Rs.1400 crore.

As India is slated to grow, all these things that you are hearing as a one off now will become almost like a habit going forward (World Cup, G20, even Olympics etc)

The cyclicality in the sector will always remain and we have to differentiate here on the domestic versus international front. But cyclicality impact should be lower than what we have witnessed in the past. Last time when cyclicality hit, we were at 17% EBITDA and we gave a guidance of 25% EBITDA margin. Today, we are giving a guidance of 33 % and even if it drops by half in a downcycle, we will be at 17 - 18 % EBIDTA. That is the change in the business model itself and the portfolio mix.

Occupancy was 75 % even in a seasonally weak quarter Q2.

One reason we will see higher pricing is because transient proportion of customers will keep going up. We have discouraged a number of small corporates from getting into long-term contracts and we have actually asked them to book on the web. We have changed the corporate contract from a fixed rate to partially to a rate which is linked to ARR.

One analyst noted that the company can generate Rs.8,000 crore kind of cash over next 5-year time period. And at Rs. 2.5 crore per room kind of a number, the company can add anything around 3000 to 3500 rooms in a luxury segment.

Taj SATS is very well positioned to go beyond Rs. 1000 crore in the next financial year and far beyond Rs. 1000 crore in the following year. Non-aviation business is less than 10% at the moment, but the aspiration is to grow it to more than 20 % over the next 3 to 5 years.

Ginger Santacruz is our trophy asset. We do believe that in 3 years of operation it should reach Rs. 100 crores in revenue. It should operate at Rs.6500 to Rs.7000 per room stabilized rate

Going forward the owned to managed properties ratio is expected to be 45:55

We have 80 hotels in pipeline. If we even stopped signing any new contracts today, we would be opening 20 hotels every 12 months for the next 36 months which means 60 hotels to open.

Management contracts are not signed when the property is fully ready. Management contracts were signed when the owner is kind of trying to start the design process and we get a share at that stage itself. Inventories per year is 3000 rooms per year which we will open, and these contracts have been signed today which we will open say in 2027.

Overall, business momentum seems intact as before. No headwinds.

Hi @Chandragupta I have been following your posts and comments. They are always insightful and most of the times I learn something or the other from them!

I am holding Indian Hotels since the covid lows and am obviously sitting on decent multibagger gains. I attended the investors call and the Management seemed confident about the long term, structural kind of a growth in Industry and an industry leading growth in Indian Hotels. As many of us believe that hotels specifically are highly cyclical and it seems that the boom upcycle post covid is getting over since the triggers are diminishing for the earnings to grow more than 20-30%, in my view.

What is your take on the Hotel industry as a structural play on premiumisation and increase in per capita income? Should one hold the stocks for, per se, 2-3 years from now?

Disclosure: Invested, since lower levels of covid.

Hi @Anubhav_Garg Thanks for the kind words. I agree hotel sector does indeed seem to have a lot going for it and many of the factors seem structural in nature, so unlikely to reverse anytime soon. If the current trends continue for the next ten years, growth can continue for the next ten years. You don’t need any “new” triggers. Risks mainly are from geopolitics – war, terrorism, civil disturbance etc or a macro economic black swan event like covid, demonetization or a severe macroeconomic mismanagement by populist politicians. None of these risks should be completely written off IMHO. But my main grouse with hotel stocks is with valuations. I was late to the party and am still unable to understand how to value them, so my allocation remains low. Whether to exit or hold on - you seem to have got in at the right moment, so actually I should be asking you for advice and not the other way round!

Well thanks for the motivation!

I do think that the price I bought this stock, offers me great downside protection but the idea is to not hold on to it thinking it would keep growing up!

I am also in the same boat as you I’ve been wondering should we consider EV/EBITDA multiple? Another way to look at this may be to forecast what it would be in FY27 after Ahvaan (take a 3 year view just like with other G20 players/logistics space)

In this report - though OPM is taken at 33%, I think revenue growth is far understated here for FY25. Given the industry tailwinds and management transformation (Ahvaan program) along with cost optimization through COVID, expect revenue growth of atleast 15-20% with demand/supply situation

EV / EBIDTA is indeed currently the most fashionable valuation metric – not just for hotels but I think across majority of the sectors.

I tried to look up how brokerage houses are valuing IHCL. Geojit Paribas has used a valuation of 22 X FY25E EV / EBIDTA. HDFC Sec assigns a multiple of 22 X EV / EBIDTA. Axis Securities gives a value of 38 X FY26E PAT. I-Sec does slightly better, as it gives 23 X FY25E EV / EBIDTA and also does some adjustments for cash, minority interest etc. and then adds values of Taj GVK & Oriental Hotels (but not others), doing a SOTP valuation. Motilal Oswal gives a value of 25 X EV / EBIDTA and does the same SOTP as I-Sec but also includes Taj Sats. Ventura Securities assigns a flat P/E of 46 X to FY25 PAT.

Traditionally, hotel stocks used to be valued on asset value basis. You could count how many rooms it has, assign a value of X per room, calculate the value of the hotel and then adjust it for other factors like debt on the balance sheet. Or based on benchmarks set during comparable buyout / M & A deals. But given that a significant share of revenues now a days come from management contracts, this too doesn’t seem appropriate now.

I am not a fan of EV / EBIDTA, but I don’t have an alternative either, especially for a complicated business like IHCL. Perhaps a better (and lazier) option is to ride the uptrend so long as it lasts, and exit based on technical analysis.

The Indian Hotels story is turning out to be better than expected. This is not just a macro story of demand outstripping supply “currently” or a “if India grows, IHCL will also grow” argument. The management has been taking several actions to seize the emerging opportunities in the economy with both the hands, much beyond what others are doing. In one of my previous post, I had reached the same conclusion when I said “Thus, the improvement in company fundamentals seems largely a result of the management’s efforts at re-engineering the business model and does not factor any industry-wide / macro factors. This leaves scope for more upside on the performance.” (See link here)

In the latest Q3 FY24 concall, management revealed several new initiatives and innovative steps to propel the growth going forward. Some highlights from call (reworded and paraphrased for readability):

Guidance: Expecting double-digit revenue growth to continue in the next financial year as well.

In ‘24-25 with 85 hotels in pipeline, the pace of openings will increase. Targeting to open on an average two hotels every month, or even higher.

The Taj brand achieving in Q3 which is the best quarter Rs.17700 ARR is less than $200, so obviously there is still some room to grow.

“New and reimagined brands”, which include Ginger, Qmin, Amã Stays & Trails, the Chamber’s and the Taj SATS will deliver 30 % YoY growth going forward.

The new businesses will do margins around 35 % plus.

Have very ambitious targets especially with Ginger brand - Rs.600+ crore.

Taj SATS will do Rs.1000+ crore next year.

New initiatives: Working on and expect to launch two new brands in the next six months.

Any new brand launched will look at getting to minimum 50 hotels in that brand in a very short period of time. The starting will be a minimum of a double-digit number before it is launched.

It is doing some very interesting things in F & B. For example, it has been catering to the IPL, the Cricket World Cup, catered to a big event the Prime Minister did at Dehradun with 7000 people, catering to some very interesting outdoor large catering opportunities is another novel step.

At some point of time, the company will not want to keep owning assets, especially in non-metro markets where the pricing of the asset is not expected to go through the roof. So, they will go for sale and leaseback. For example, the two hotels in Ekta Nagar, the Vivanta and the Ginger near the Statue of Unity. Such hotels need not be owned for perpetuity but cash can be freed through sale & leaseback deals.

Will have 7 to 10 “iconic” hotels in the next few years. One can expect every year one & half to two iconic Taj assets getting added.

Immediate future: Demand continues to outpace supply; the January trend is very much in line with what was seen in Q3 in terms of top line growth. Pickup is equally good for the month of February, and they have visibility till March as well. There is the IPL in end of March till May, again this year. So, all in all the demand is very strong, supply remains constrained.

New brand for Tier II & III cities: Price point will be somewhere close to Vivanta. So, just a little below the Rs. 10,000, higher than Ginger but lower than Taj somewhere in between but a full-service brand. It will help us cater to the mass market of 400 to 500 million Indians who are also not in metros but in Tier-2 and Tier-3 cities. It will be a full-service upscale brand. The details are being finalized, but it will be something that serves the needs of mass market. It will have 26 - 28 square meter room, a couple of restaurants, it will have large banqueting spaces which can accommodate weddings of 300 to 500 people easily and at an affordable price. Upper midscale, upscale - that is the positioning.

Emerging destinations: Ayodhya the first hotel should open in less than 12 months. Also looking at large homestay opportunities in Ayodhya, the Vivanta and Ginger combo hotel will take another 20 months to open. Lakshadweep will take longer because of the nature of the development, it’s not just building hotel its developing two islands, the islands of Suheli and Kadmat so that would take anything between three to five years.

Sea Rock: Will try to get a strategic partner and everybody is knocking at the doors whether from within the group or outside. IHCL will keep the majority, but they have no intention of spending further Rs.800 crores from their own cash reserves. But definitely Sea Rock will be made the Icon of India, a second gateway after the Gateway in Colaba.

Taj Sats: Doubling of airports from 75 to 150 provides another opportunity for Taj SATS

Government support: There is more and more travel happening as 50 new airports, so many new aircrafts ordered by India is going to propel a kind of growth in travel that we have not seen. And government’s focus this is second year in a row that tourism got a mention in the budget presentation of the honourable FM and also, they have got industry status in several states in India now.

Going ahead: Likely to achieve the 300 number at least one year in advance of our 2025-26. (300 hotels target was given as part of Ahvaan 2025).

Some more from an ET report quoting Ms.Deepika Rao, EVP New businesses and Hotel Openings:

Ginger: Planning to have a presence in all 800 districts of the country. By FY26, Ginger would become a 125-hotel portfolio. The expansion is based on the asset light model. Typically, large box projects consisting of 300 plus rooms are based on a management contract model, while the smaller ones with up to 80 rooms are taken on a lease of up to 30 years. About 30% of Ginger hotels are managed, while the rest are either owned or leased. The number of rooms in Ginger hotels vary from 80 to 300 plus. Ginger will continue to grow at 30 %. Ginger has all day dining under QMin brand. Almost 50 % of the Qmin’s Rs.100 crore revenue will come from Ginger hotels.

TajSATS: Its share in IHCL’s topline will increase from 11 % to 25 % in the next few years. Expected to clock a revenue of Rs 1,000 crore in FY25 against Rs 650 crore in 12 months ended January. Qmin will be used for TajSATS’ institutional catering. Has also got into QSR space with Chhayos and Starbucks as customers. Starbucks has close to 1000 outlets in the country.

Some highlights from the Indian Hotels Q4 FY24 concall:

The year gone by:

Company now has surplus cash reserve of over INR 2,200 crores.

60/40 mix of capital light versus capital heavy assets

34 hotels opened during FY '23-'24

218 hotels operational

New and reimagined businesses currently contribute roughly 14 % to consolidated revenue (this is Ginger, Qmin, amã Stays & Trails, The Chambers and TajSATS)

ARR growth for Standalone Q4 like for like is 8 % and Revpar growth is 15 %. For reporting numbers such as ARR growth and RevPAR growth, the company includes all hotels, which have been in operation for a minimum period of 1 year. But it takes 3 years normally for a hotel to stabilize. So the reported numbers get diluted technically.

Margin for us is an outcome rather than a target

Gateway brand launched:

The Gateway brand rollout will commence with 15 hotels and will scale to 100 by 2030. Now is the right time to launch this brand, which will be upscale, full service and a gateway to that city. It will be a very regional brand, which will have all the important characteristics of that city. So Gateway in Nasik will represent in its art work, in its style, in its arrival experience in Nasik. A Bekal in Kerala will represent Kerala. All 15 currently planned are on asset light model. Management also gave an explanation behind positioning of various other brands like Taj, Vivanta, SeleQtions.

Coming year FY25 and beyond:

Target to open 25 hotels in FY '25

New business will continue to grow also over 30 % in the next fiscal, which last year was at 35 %. As the base gets larger, the guidance you can expect will be in the range of 30 now and going forward, maybe at 25 %. For the company as a whole, anything which is north of 10 % on an average for the year is a realistic number going forward because the base has become larger.

One analyst noted that the company will be generating Rs.8,000 to Rs.9,000 crore cash in the next 5 years.

I.T. will be a big focus for the company in the next 18 months, lot of capex is allocated to that as well.

There will be some temporary impacts in terms of elections in Q1

Other points:

India is now not anymore talking October to March destination. It’s becoming a 12-month destination

Management says competition is not a problem and there is no fear of oversupply. Hotels are a micro-market business. And if you look at our hotels in our micro market, there’s effectively no new supply coming. The company has 92 hotels in pipeline. In the number of hotels in pipeline, they are way ahead of anyone, feels the management. And these are signed legal binding contracts. Pipeline is not just projects under negotiations. That number is even larger.

The management says with our size now, we can start talking ourselves as a consumer business

Today, 75 % of business is still in the business segment and 25 % in leisure. The opportunity in leisure structurally is much better.

A new dividend policy is declared which targets a payout ratio of 20 to 40 % of PAT (Standalone or Consolidated, whichever is higher). Current year dividend is declared at 20 % of Consolidated PAT

Can you please share the sources that you use for getting the reports that calculate valuation parameters such as EV to EBITDA after calculatedly anticipating/predicting a company’s future performance?