Don’t understand why is he so downbeat in his responses. Is he suggesting that slowdown is about to hit them as well? I was not impressed with the cash generation in this quarter. It is sensible to keep expectations low and deliver better.

I suspect he is trying to talkdown the high expectations and preparing ground for a more subdued next quarter.

How does the concept of Deferred revenue work here? Is it subscription already paid which is not yet recognized as revenue?

It is getting recognised by the market slowly.

1 Like

Have been studying IndiaMART InterMesh recently. Please find my findings below from Annual Reports, Conference Calls, DSIJ report put above and IPO Prospectus.

Introduction:

IndiaMART is an e-commerce B2B marketplace started in late 1990s. It has tried various business models, pivoted with learnings and finally emerged as India’s leading B2B e-commerce marketplace with market share of 60%.

The company is going through a lot of tailwinds - Internet Penetration, GST, Tech adoption by SMEs, Network effect of Buyers and Sellers. And these tailwinds are expected to stay well for the foreseeable years. These tailwinds are causing the company to grow its business at tremendous rates with revenue growing at 25%+ CAGR over the past three years and profits growing at ~30%.

Also, there is a strong operating leverage coupled with this huge sales growth as the company recently turned profitable and unit economics are very strong. The CEO aspires to achieve EBITDA margins of Facebook / Naukri over the years, which are at 50%. He is looking at targets of 25%+ revenue growth and 20% growth in expenses over the next few years. Corporate tax cut would also help here, as they have enough pricing power.

Well-scaled tech companies are cash-oozing machines. Once a tech company turns profitable, the incremental re-investment needed for incremental growth is very low and this characteristic of the business helps it to continuously ooze cash. Look at well run Silicon Valley companies for examples.

There is a lot of pressure on the Indian government to boost manufacturing activity in the country and create jobs. If this leads to increased business activity in the country, it would immensely benefit IndiaMART.

IndiaMART is richly valued by the market at 65 times P/E and 11 times P/S. However, the strong sales growth coupled with operating leverage can give strong returns if things go well for the company.

Packages:

Silver (Rs 30k / year): Supplier storefront + Unique webpage with Personalized URL containing IndiaMART domain name + Access to online payment gateways + 7 RFQ credits per week + Product Listing Priority

Gold (Rs 30k to 60k / year): Silver Package benefits + TrustSEAL verification + 14 RFQ credits per week [OR] Silver package + Personalized URL without IndiaMART domain + 21 RFQ credits per week

Platinum: Gold++ (i.e. Higher Priority Listing, More RFQ Credits…)

Customers can buy also additional RFQ credits on top of these packages but these don’t contribute too much to the topline.

One can go through the solutions tab from below link for more details:

ARPU as of Q2FY20: 45000 Rs

Top 10% customers contribute 40% of the topline. ARPU of these customers is about Rs 1.6 lakhs.

Annual package subscribers typically churn at 20% per year => 2/3rd customer base.

Monthly package subscribers typically churn at 5% per month => 1/3rd customer base.

Renewal rate turns out to be significantly better as the customer becomes a turned one. So typically, you would see the first year renewals would be lesser as compared to the second year renewals and the third year renewals.

CMS & LMS:

IndiaMART has developed its Content Management Services (CMS) and Lead Management Services (LMS).

The CMS helps suppliers manage their product and service catalogues on IndiaMART while the LMS provides suppliers instant access to their IndiaMART business enquiries in one place online and the ability to manage them. The LMS also allows suppliers to arrange and respond to enquiries in one place. The CMS integrated in the mobile app allows suppliers to manage their listings and conduct business ‘on the go’. The mobile app also offers instant notifications of enquiries, RFQs and replies.

Sellers can also integrate their leads originating outside the IndiaMART platform on the LMS, which makes IndiaMART LMS as a single unique platform for managing their entire business leads. This also makes the supplier base sticky.

Payments:

Pay With IndiaMART is in beta phase, using which the company is trying to build an additional revenue stream. It is a payment gateway that allows sellers to create a payment link and send it to a customer over Email, SMS etc. The payer can click on the link and make the payment using credit card, net banking and other payment options. IndiaMART charges the seller a transaction fee of 1.75% and applicable GST (currently 18%) on the transaction fee.

The company also offers 100% buyer protection, which covers buyers against various issues such as non-receipt of product, damage etc. Buyers can raise a claim for refund with IndiaMART.

Initially, the company saw good traction but is finding it difficult to scale up on the payments side. They only do 5000 payment transactions per month and these are early days. The company is trying to tweak the payment product on a monthly basis to find the sweet spot at which they can scale very well.

Other Potential Revenue Streams:

Credit: The company seems very interested here as they have access to transaction data between the buyers and sellers. There are two ways to run a credit business in marketplaces.

- Act as a medium and let financial institutions lend to the suppliers while IndiaMART charges commission

- Lend out of your own books by getting an NBFC license

IndiaMART plans to go explore the first route as they believe building platforms using technology is their core competency than lending.

SaaS: This can be an additional top-up to the SMEs on top of IndiaMART’s subscription package to help them manage their businesses well.

Investments: IndiaMART already started using its cash to fund new startups. It has recently invested in a startup called Vyapaar which helps the business in accounting, invoicing and inventory. IndiaMART wants to help this company grow over the next two years and then later consider fully merging it into IndiaMART.

Udaan:

Lots of startups have started focusing on SMEs like Power2SME, Moglix, IndustryBuying, Udaan, Bizongo, OfBusiness… Out of all these, Udaan has drawn heavy focus from the VCs. It commands a huge valuation of almost $3 billion, while IndiaMART is valued by Dalal Street at < $1 billion. Udaan is flush with cash of $500+ million, as of October 2019.

However, the operational business of Udaan is still small compared to IndiaMART and we need to see how they will expand and compete with IndiaMART. Udaan operates only in few verticals like apparel, electronics, pharmacy, staples, fresh food and FMCG products while IndiaMART’s main focus is on long-tail manufacturing products (Also no single category contributes more 10% of revenues of IndiaMART). Udaan is also into lending business and yes, it is lending from its own books. I think lending is not a very easy business to learn with speed even though you use cutting-edge tech, so we should check if their loan book growth would be a conservative one or an aggressive one. Another aspect of Udaan is they also handle the logistics between the supplier and the buyer, while IndiaMART doesn’t service the logistics but just connects the buyers and sellers. IndiaMART has already given a shot at logistics part through Tolexo.com and observed that the unit economics there doesn’t make much sense and hence pulled it off.

Such huge focus / funding by VCs and entry by new startups in this area asserts the longevity of the industry.

Promoters:

The promoters’ educational background doesn’t look very impressive, however his professional experience from the Wikipedia article gives confidence. But I think we can give low weightage to his education given the way he has built IndiaMART and pivoted it through his learnings.

The promoter doesn’t seem to like investors of the type “Burn fast to Run faster”. Look at the video below where he talks about it. It suggests he is building a business to run during his lifetime than to just sell and cash in.

Promoter’s story in his words:

Will have to do some work on the promoter side, to have more confidence that the business is being by strong people.

Financial Metrics:

Balance Sheet, P&L Statement and the Cashflow Statements can be looked up on Screener.in. Let me devote this space for even more interesting metrics.

| 2019 | 2018 | 2017 | 2016 | ||

|---|---|---|---|---|---|

| Suppliers (millions) | 5.5 | 4.7 | 3.2 | 2.3 | |

| Paying suppliers (000s) | 130 | 108 | 96 | 72 | |

| Product Listings (millions) | 60.7 | 50.1 | 33 | - | |

| Buyers (millions) | 82.7 | 59.8 | 39.4 | 27.1 | |

| Visits (millions) | 723.5 | 553 | 326 | 262 | |

| Enquiries (millions) | 448.9 | 290 | 157 | 115 | |

| Product Listings / Suppliers | 11.03636364 | 10.65957447 | 10.3125 | - | |

| Visits / Buyers | 8.748488513 | 9.247491639 | 8.274111675 | 9.667896679 | |

| Enquiries / Buyers | 5.428053204 | 4.849498328 | 3.984771574 | 4.243542435 | |

| Enquiries / Visits | 0.6204561161 | 0.5244122966 | 0.481595092 | 0.4389312977 | |

| Paying suppliers % | 0.02363636364 | 0.0229787234 | 0.03 | 0.03130434783 | |

| Calculated ARPU | 39032.07692 | 38010 | 33100.3125 | 34132.36111 |

Buyers => Growing at a tremendous rate - 3x in 3 years. And the number of enquiries per buyer has also risen from 4.2 to 5.4.

Suppliers => Also growing at a fast rate - 2.5x in 3 years. And the number of product listings per supplier has also risen from 10.3 to 11.

Only bad part among those metrics is that the proportion of paying suppliers is falling and I hope to see it increasing too. However, the ARPU is increasing very well over the years, implying customers are really seeing value in their subscriptions and upgrading their subscription package.

Due to upfront payments for the subscriptions, the company is working capital negative of 1 month. This helps the company stay flush with cash and helps it react quickly whenever an opportunity surfaces.

| 2019 | 2018 | 2017 | 2016 | ||

|---|---|---|---|---|---|

| Inventory days | 0 | 0 | 0 | 0 | |

| Receivable days | 0.3800495634 | 0.5769965031 | 0.5838926781 | 0.3504456016 | |

| Payable days | 29.9533634 | 35.59872976 | 33.25219319 | 54.72622496 |

IndiaMART has this concept of “Deferred Revenue”. When suppliers buy package for the full year or for couple of upcoming years, you already have the cash in your accounts but the revenue is recognized only when that time period passes. All the remaining cash will be accounted as “Deferred Revenue”. Typically, 60% of Deferred Revenue represents contracts for the next 12 months and remaining 40% represents for time period post next 12 months.

Risks:

Disruption => With VCs shifting focus to B2B now and they are very aggressive and happy to see red P&L statements, we should see how IndiaMART will face this competition while maintaining profitability.

Fake suppliers => Listing of fake products by the suppliers can cause trust issues in the marketplace. The company has turned very stringent while approving suppliers. It is looking for suppliers with 100% verification of mobile numbers and also registering suppliers who have their GST registration completed.

Hacking / Security => Leaked information of customers can lead the company to a huge trouble.

Advertising Costs => IndiaMART had incurred losses few years back when they were bang on in advertising. As of now, they have stopped advertising. P&L statement can take a hit again if they have to go aggressive on advertising again in the future.

Differential Pricing => IndiaMART prices SMEs the same across categories, industries, towns and cities. This can cause some suppliers to never afford the packages sold by IndiaMART thus losing out revenues from them. This leaves room for competitors to come up with niche platforms to grab these customers. The company said it will work on this direction after two to three years.

Disclosure:

I have no investments in the company, but the opportunity looks interesting to me. This is not a buy / sell recommendation. Investors are expected to do their due diligence before buying / selling shares of IndiaMART. I’m not a SEBI registered advisor.

13 Likes

Actually checked my LinkedIn network and realized I have a friend working at Udaan. Here are some points I have noted from my conversation with him.

- Udaan’s current product lines are on items which are smaller in size, as that is what their current logistics infrastructure can support. But in the long run, the product categories would be expanded to larger items.

- 97% of business in India is B2B. So there is a much higher potential than B2C and thus valuations of Udaan reached so high (~3 Billion USD) in just three years.

- Udaan’s current focus is more on connecting product distributors to retailers while IndiaMART’s focus is on connecting manufacturing SMEs to other manufacturing SMEs. However, in the long run, Udaan plans to increase their perimeter of business to all kinds of B2B.

- Employees at Udaan don’t discuss much about IndiaMART in their office but discuss a lot about Reliance and Flipkart. My guess is this is because these are more focussed on the distributor to retailer network.

- Udaan has got its own NBFC license to write off loans to buyers.

- On the logistics side, 70% of orders in Udaan go through Udaan Express, while 30% go through third party vendors. They go through Udaan Express when they have a lot of orders going through the same route, but use third party vendors when the orders are thinly spread.

- Udaan is giving away huge discounts on the logistics side. In fact, delivery used to be free a while ago and now, they have started charging but still at huge discounts. In a given vertical, their losses are a multiple of their revenues.

My inference: Such aggression by Udaan will definitely be worrying for investors of IndiaMART. It will only increase with time as Udaan is just three years old. Udaan not being present in most categories of IndiaMART can give comfort for next one or two years.

Disclosures: Same as above.

9 Likes

so as for the valuation you cant logically even look at India mart by a PE multiple , in this case it gives a completely distorted view of the company and the new profit is just an accounting number specially in India marts case. If you see the cashflow and the net profit its a huge difference, the net profit is 97cr but the actually cash generated ( operating cash-(working capital+mainiance capex+ growth capex) is 255cr last year ! so its actually on a free cash yield of 5-6% , and it has 750 cr cash on books! so the expensive valuation statement a very unsophisticated and rudimentary answer you gave, the company is actually trading at 17 times I would say free cash and not to mention it has a float, it needs no investment into working capital its negative working capital business , it receives advances from customers which in itself is a huge thing not many companies in any industry have a negative working capital.

disclosure invested at lower levels

5 Likes

Any idea why they were reporting losses till FY18? From what I understood, their business model has always been asset light, had the advantage of negative working capital, generating good cash. Why have the accounting profit been negative till close to IPO?

2 Likes

the modell in these type of business usually have bad base rates ( base rates mean the percentage of companies in the sector that survive/ and if survive then are they creating any value ( ROE/ROIC above their cost of capital) , I would say its about 90-95% fail but the ones that make it are super profitable and if you see testla or amazon as an example and some other ones history they follow Reeds law ( https://www.google.co.in/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&cad=rja&uact=8&ved=2ahUKEwiOitrJ6pbnAhVEzzgGHYZIDpMQFjAAegQIARAB&url=https%3A%2F%2Fen.wikipedia.org%2Fwiki%2FReed%27s_law&usg=AOvVaw3Umeiw-UBUXjMzcq7scBpK) . Basically they have something called critical mass , once they cross that point they become incrementally profitable because that initial costs don’t increase in proportion to the sales, but the initial costs on even a very small sales base is large, and as you scale it diminishes as a % of sales, so basically its a race to who can cross it first and India mart has done that by a huge margin . The closest 4 competitor’s are no where close and Private Equity backed companies like "Udaan "are valued at 2.3billion$ and still burning through cash. Hope that answers your question. Not to mention India mart trades at about 7/8 times cash on book, , barley giving any value to the negative working capital business of business and the huge cash it gushes out , wont be surprised if its doing a cash of 600/700 cr in 2 years

4 Likes

IndiaMART InterMESH

Revenues up 23.4%, EBITDA up 58.5%, Net profit up 2.2x

Increase in paying subscribers and higher realization from existing customers aids revenues

Traffic up 9%, Total Business Enquiries down 6%

Some Points in interview give answers to your question

“I want to take the company to the next level. I have been at it for the last 23 years as a private company. We’ve seen multiple ups and downs, been profitable, made losses, and raised a couple of rounds of private capital. I think in the next 23 years, I want to see how a public limited company works."

“The traditional profit and loss mindset also worked well for us. We were not into the valuation game, rather more of a self-sustainable inning. Frankly, I didn’t know the valuation game. I was not exposed to that."

No wonder, for Dinesh, personally, the IPO is more of a fulfillment. “I want to create a long-lasting, forever company. I want it to be the backbone of the Indian economy. Today, about half a percent to one percent of India’s GDP is close to IndiaMart’s. So I am looking at how I can make it 10X, and how I can make IndiaMart a dependable source for small and medium businesses."

4 Likes

Ruanank Onkar Presentation in financial opportunities forum on platforms.

Also relevant for other Listed cos like IEX, Info edge, Fintech NBFC bajaj, Banks, Staffing cos like SIS etc.

1 Like

India mart

From edelweiss report

No longer a classified listing website. IndiaMART is a detail product catalogue website.

Moderation in growth expectation due to deceleration of deferred revenue growth

rate. If the next two quarters also remain subdued, the impact will be visible H2FY21

onwards.

Average revenue per user has grown 5-10% historically.

Marginal decline in business enquiries, but they have been stable over the past

quarters. There has been demand slowdown, which is also impacting the metric.

Higher proportion of outsourced employees. Spread across 75 plus new sales

acquisition offices. For a field sales operation and tele-sales operation (requiring lower

education levels) and given the high attrition, it makes sense to hire outsourced

employees.

SMEs are still not adept to the internet ecosystem of lead generation and they prefer

the dealer distributor system or inbound call/walk-in customers.

Here, IndiaMART comes into the picture and helps them onboard the platform. The

key is to develop the supplier base as the buyer-side demand remains robust. There is

acute shortage of suppliers on the platform.

Slowdown in paying subscribers is on account of slowdown in economy as SMEs tend

to delay advertising expenses on one hand, while some SMEs run out of business as

well.

3 Likes

I dont know why it is trading higher, when a pandemic virus is hurting global trade. If trade is hurted indiamart will be the biggest looser

I just went to one of the vendors who provide water purification solutions to our hospital and asked him if his supplies got affected due to corona virus. He said almost 60/70 % of raw material comes from China so yeah they are definitely affected but they are trying to cover up by local sourcing. It has increased costs by around 10/15% but atleast they have an option. May be that throws some light that this corona virus thing may be beneficial to IndiaMART.

2 Likes

I was reading through reports about Shopify this weekend, it has created multiple billion dollar plus businesses. Its great model and enabler for small businesses , but Shopify is very expensive.

Indiamart has some similarity in nature to Shopify, also Indiamart by itslef is a marketplace. The addressable market is very large, and eCommerce , B2B/direct to customer with growing economy/digital India has a great prospect.

But so far, the promoter didnt comeout as impressive with little bit of reading I did. I could be wrong.

Amazon/Shopify/Etsy/Thetradedesk have been successful largely because the promoters are great leaders and had a great vision.

Has anybody had any chance to meet the promoters of Indiamart or have done detailed research?

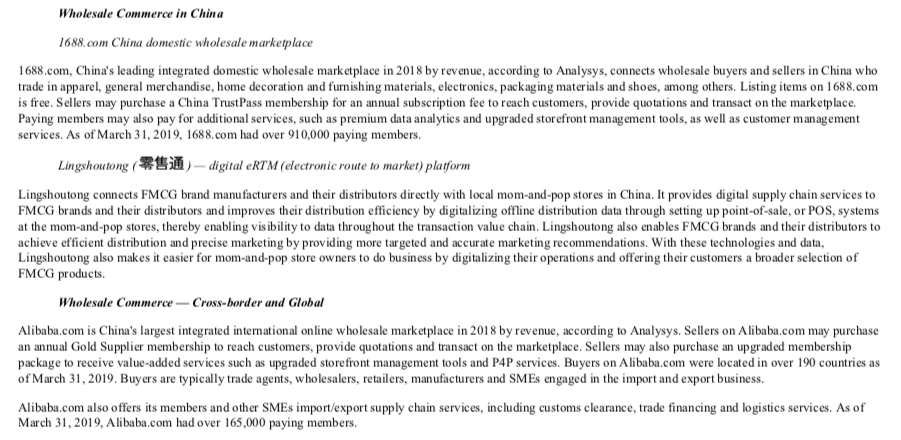

Summary of Alibaba’s B2B commerce.

Source: Alibaba 2019 Annual Report.

9.1 lakh paying suppliers in domestic B2B through 1688.com

IndiaMART has 1.42 lakh such suppliers after Q3FY20.

Alibaba’s China Domestic B2B e-commerce is still growing at 20%+, 30%+ kind of growth rates, but growth is mainly driven by ARPU, but not through growth of supplier base.

EBITDA margins of all kinds of commerce of Alibaba (Retail + Wholesale) is very high at 40%-50%.

Couldn’t find margins of only B2B e-commerce.

IndiaMART has the first mover advantage. Only question to me is if the management will capture the opportunity and execute it properly.

Discl: No holdings, considering to start to take a position.

2 Likes

Conf Call Q3FY20 Notes:

- Traffic grew to 188 million in Q3FY20 from 173 million in Q3FY19, an increase of 19% YoY, however total business enquiries delivered witnessed marginal decline to 112 million from 120 million, a de-growth of 6%.

- Supplier storefronts grew to 5.9 million in Q3FY20, an increase of 8% YoY and paying subscription suppliers grew to 141.6k, a growth of 15%.

- As we can see the economic environment is weaker which is impacting our performance, our net customer add has been slightly lower than our longer-term average of approximately 5000+ customers per quarter and the growth in deferred revenue has also slowed down considerably from 38% in the last year same quarter to 26% on YoY this quarter.

- We will remain cautious about the current economic scenario and will focus to maintain our margin while we are trying to find levers of further growth into our business.

- The revenue flows from the deferred revenue, which is approximately 60% current in nature, i.e. to be recognized in next 12 months and 40% is beyond that.

- Internally, when we calculate we see that the average age / period of our deferred revenue is about 20-21 months. Now that means that the revenue that you see is a 20-month moving average, which is reported in the quarterly financials. Now if you see the leading indicator of that is the collection or billings which can be computed by calculating the difference in defered revenue and revenue recognized for the quarter. Collections / billings are also part of our detailed financials. So as compared to the last year where our collections used to grow at approximately 30% on YoY basis, for nine months, our collections have only grown 15% or so in the past nine months i.e. past three quarters, which is resulting into slowing down of growth in our deferred revenue. So if you see last year same quarter our deferred revenue grew by 38%, but this year same quarter, the deferred revenue could only grow by 26%, which is quite a sharp decline from 38% to 26%, and which will further show up in the actual revenue from operation.

- Even in the revenue from operations if you see three quarters ago Q1 we were at 30% growth rate, Q2 we were at 28% growth rate and now Q3 we are at 23% growth rate, so it is declining. But that decline will not happen in one single quarter or immediate coming quarter since it is approx 20-22 months moving average.

- So in case we see a couple of more quarters continuing to be below 20% collection growth rate then obviously the revenue would start to trend on the similar lines.

- Typically in Q4 what we see is that our billings are the highest amongst the quarters in the year and since our expenses also are in proportion to the billing that is where our expenses also increases.

- As Dinesh just explained that the revenue increase is always a moving average of the last 20-22 months of billings so therefore there is no such increase in the revenues; however, because of the billings increase or expenses increasing slightly, this is typically a quarter where we see the highest cash from operations.

- However, as the revenue increases only over a period of 20-22 months, we see margin declining in this quarter that is a pretty seasonal impact that we see every year.

- I’m not too bothered about the buyer inquiries in the short run because if you see we are sitting on a very heavy growth base over the last FY16 to FY19 where our buyer base and traffic and inquiries typically grew by 80-100% kind of growth rate. I think given that we get about 6 crore visits on our platform every month, I’m not really bothered about short-term in terms of buyers.

- Yes, in the longer run if there is a fundamental shift from the way IndiaMART is used or the way other services are used then there could be issue, but given that the economy has seen significant slowdown, many sectors like automobile and others are at 20%-30% slowdown, even the FMCG, the machinery etc are down.

- Our 90 day repeat rate, which we have been publishing regularly hovers at around 54%-55%, if you see the Daily unique inquiries that again remains at 18 million - 19 million per quarter and which automatically translates into about 30 million 12 month active.

- If you see our sales and service representative are about 4000 people and another 500 odd people in the tele based sales, so about 4500 people totally working on helping these suppliers come onboard on IndiaMART and depending upon how well we can service and how fast is the adoption versus their propensity to leave the platform that is the net customer addition.

- So I think if you compare worldwide, for most of the classified sites, 2% to 3% is the common penetration. But that 2% to 3% penetration is on all India basis for Indiamart. If you really look at our penetration in the top 8 metros, and since approximately 60% of our customers now come from top 8 metros, there the penetration would be much higher.

- Our top 10% customers account for 40% revenue. So if you see the data they continue to remain in line with the previous quarters, no change has been observed there because top 10% customer means approximately 14000 customers (basically platinum customers), which means more or less same, we are able to maintain that.

- IndiaMART is a pretty long tail of categories, we have more than 1 lakh product categories where we deal into. Now Udaan or Walmart wholesale or METRO Cash & Carry or Amazon business, these people generally are focusing on the specific product categories, which are typically FMCG or dealer distribution product category. They are building warehouses, logistics and transportation. I do not feel unlike in B2C where home delivery is a new concept, B2B deliveries has been happening for ages by way of sea, by way of train, by way of surface and I do not see a large value add by our experimentation that we did in Tolexo in B2B logistics, so we are not currently interested in the space. I think they are doing some interesting experiments with credit, which is interesting item to look at, we continue to study and experiment to see if anything like that can be built in IndiaMART.

- Ever since the economic environment has changed, we have seen a marginal decline across all segments like platinum, gold, silver annual and silver monthly. However, the platinum segment continues to be very strong.

- As we said in gold and platinum typically, we have less than 1% churn per month and annual churn of about 10% to 12%. On the overall annual base, we now have about 20% churn. On the monthly as I said always that is a volatime item and on the monthly basis trial keeps on happening. Also if you see our total customer base, we have one third of the 1.42 lakh customers on the monthly side and most of the other customers are in the annual side and about top 10% of our customers are in platinum segment.

- Though we do not specifically publish collections as a KPI, but if you see them in the detailed financial you can find there is a section note where it is available and it can also be calculated very easily by way of opening deferred revenue and closing deferred revenue and the revenue.

For this particular call, I will give you the collections number. Collection for the current quarter was Rs 183 crores and previous quarter was Rs 177 crores. - Somewhere around 2015-16 onwards we found two, three good innovations that started to work for us. One was the price on the product and two was the detailed product specifications. We migrated from being a classified listing website to a product catalog website. You can find the detailed product photos, videos, detailed specification item-by-item. Third, we started to use behavioral based algorithmic matchmaking where we started to use suppliers RFQ consumption behaviour to assess his preferred location and product category over his stated location and stated product category. All three of these initiatives helped us increase our buyer fulfillment rates from 20% to almost 40% from 2015-16 onwards. If you see the macros also, there have been big changes in the mobile adoption and in the data speed and data cost both and there has been forced adoption of the internet also by way of compulsory income tax filing, compulsory GSTN filing, demonetisation which led to a lot of people learning how to use internet and payment methodology.

- There are so many B2B platforms being tried currently but none of them have gained any significant traction to say that IndiaMART is losing out to them.

- Lot of people who come from Tier-2, Tier-3, Tier-4 places do not read much, but they have a very good habit of watching videos so we can do product videos. We have taken some initiatives on these directions, but they won’t be immediately visible. As I said the price initiative and specification initiative and alogrithmic matchmaking initiatives taken in 2015-16 actually started to pan out in the next two, three years. As we have taken some initiative on Hindi language and videos, over the next three to five years they should start to pan out.

- Secondly earlier we were only generating leads now we help buyer and seller talk to each other using IndiaMART lead management system or IndiaMART message section as a platform.

In FY17-FY19 period we have not done any advertising, it is now going to be four financial years where we have not done any significant advertising. - Every year we do budget for Rs 20-25 crores for the purpose of advertising and as and when we feel there is a need for advertising we will go ahead and do that.

- The margin expansions will slow down due to slowing collections, but we are confident that we should be able to maintain the margin at these levels for sure.

- When we hire people for the client servicing or for the purpose of product and technology or operations we do not hire for that particular role, we hire people so that they can grow in the ranks of management and over the period of time as a senior manager also. However not everybody who has done that kind of an education is interested in doing SME sales and so typically we find that for a field sales or tele sales operation the kind of people that you need, and the attrition that you have is pretty high, which actually unnecessarily strains our own payroll systems, so that was the purpose for increasing outsourced headcount. In fact, they actually cost slightly more than if they were onroll.

We had taken the decision about three years ago and will evaluate going forward if that makes sense even continuing forward. We wanted to be doubly sure that we report these people as a headcount because they are not visible in the statutory financials. - Almost 99% of our customers start at the silver monthly or silver annual subscriptions. At the acquisition level 80% of them are on a monthly subscription and 20% of them on an annual subscription and then they are upgraded as they try the service or as they become comfortable with service. They are upgraded in two ways. One they are upgraded into the tier from silver to a gold tier, we have multiple tiers in platinum. Two they are upgraded into a multiyear service. Three, sometimes there is a combination of gold plus multiyear, which is one of our most popular packages.

- Generally, you will see that the ARPU at the blended level, which we have been reporting is about Rs 44000 or Rs 45000 per annum. As I said the entry level is about Rs 30000 and if you calculate the top 10% contributing 40% of the revenue that works out to be a little upwards of Rs 1.6 lakhs per customer.

- Every buyer will see a very different supplier depending upon where is he logging from and every supplier will see very different set of RFQs depending upon his past behaviour and depending upon his tier of subscription.

- From our point of view we want the buyer to be satisfied, whether or not I made money from that supplier, that is a secondary objective. If a buyer has come to IndiaMART he must be satisfied and every buyer who is satisfied with the free supplier becomes a sales lead for us. That is how we go and talk to that seller and say that since you have received ex number of leads already being a free customer imagine what you can do by being a paid customer and many of them want to pay up and show up higher up in that category or location while at the same time some will continue to enjoy the services for free.

- We were trying to do a differential pricing because currently the entire pricing on our platform is in standard price irrespective of the location or irrespective of the value of the category in which you deal in, though we were trying to move to the differential pricing; however, given the current economic scenario we may take slightly longer time in terms of launching that differential pricing all across.

- If we see certainly the churn rates have increased on an annual and multiyear customers. From 16% to 18% churn, it has gone up to more like approximately 20% churn annually now and similarly on the monthly customers, which is one third of our database our churn rates were around 3% or 4% per month, which have gone up to more approximately 5% per month.

- If we are adding almost 5000 customers there would be some 50 to 100 people that we would be adding on the servicing side every quarter, but that is pretty much it and the annual increments will be effective every June.

- About 20% of our expenditure remains in the product and technology side we have about 500 people in the product technology data and we have pretty seasoned set of people new as well as old as 15-20 years with me. So I’m pretty confident that we have a team, which is very good in the product and technology and at part with the industry standards anywhere in the world.

- We also keep taking consultancy from various sources so for example we are constantly looking at innovation in artificial intelligence and machine learning and I myself am a software engineer, so I think we have enough number of product and technology people here.

- Since we are not a transaction based model, the discounting led incentive may not work for VCs / Startups to enter my business. Also we have a copyright on all our information that has been accumulated over the period of time.

Discl: Same as above.

10 Likes

Attaching my Deep Dive Notes.

IndiaMART.pdf (169.6 KB)

Discl: I don’t have IndiaMART on my portfolio. Need to study more. I’m not an investment advisor and you are responsible for your investments.

12 Likes

Thanks @lingalarahul7. Quite detailed report and very valid Qs on missing/further deep dive parts.

If we were to have hypothesis of post corona world and roles that tech platform will have - adding some pointers

-

B2B events and mktg activities with traditional ways will change and lean toward Digital- a big positive for Indiamart - not only digitization accelerate but will get larger budget allocation( bigger paying base + higher ARPU+ value adds)- would love to see innovation like virtual industry events on platform and let industries see outcomes

-

In entire Corona situations- media is portraying China on negative end - both from public perception and supply chain failure risk for western countries - India and other low cost mfg countries will benefit- larger base for Indiamart to target and in return offer them quick go to market and scale.

-

While operating leverage is well understood, a network effect is equally at play ( more suppliers leading to more demand …) and may scale better than their expectations with social distancing- here to stay - next 2 qtrs can validate

-

In some recent con call/interview - Promoter did mention of having tried credit facilities- didnt find it attractive and hence stepped back and focus on core discovery biz - probably want PEs backed Udaan(?) To burn some money and learn from it.

-

Their major demand gen( new customer)is based on tele calling - the only model that Corona couldn’t have disrupted

I have some tracking positions and watching closely to get some good entry price. Recent pull back in prices also demonstrated strength in price action( didn’t go in LC or UC frenzy unlike Affle or IRCTC)

4 Likes