Any one has recent transcript of Concall? And as per management, radaliasation has made retreading delayed, but in the long run it will benefit retreading. How’s this possible?

The result for this quarter are very poor. I have been noticing that lot of players are getting into the retreading business. Eastern Treads has revived their business GRP has recently entered the re-treading business. The economics of this business are amazing and no wonder people are getting into this business.

With improvement in roads and government curbing the life of CVs it may impact the re-treading industry. On the other hand radialization will benefit the industry

If anyone has the transcript of the con-call - kindly share

Radialization is making people shift to radial tyres in the short run. This is making people shift to new tires who would have otherwise gone for re-treading. The reason why it is good for the re-treading industry in the long run is because radial tyres can be retreaded more.

1 Like

Now, as per management in earlier Concall majority of the retreading is with unorganized sector about 60 to 70 %, with the introduction of GST a large part of this pie can be transferred to listed player. So how big can be this opportunity? And can they have the pricing power if the government decides to support the industry?

Retreading is applied to casings of spent tires. Tyre casings requires to be completely round for retreading. Casings are not damaged if roads are good. Therefore in my view, improvement in roads will be positive for retreading industry.

1 Like

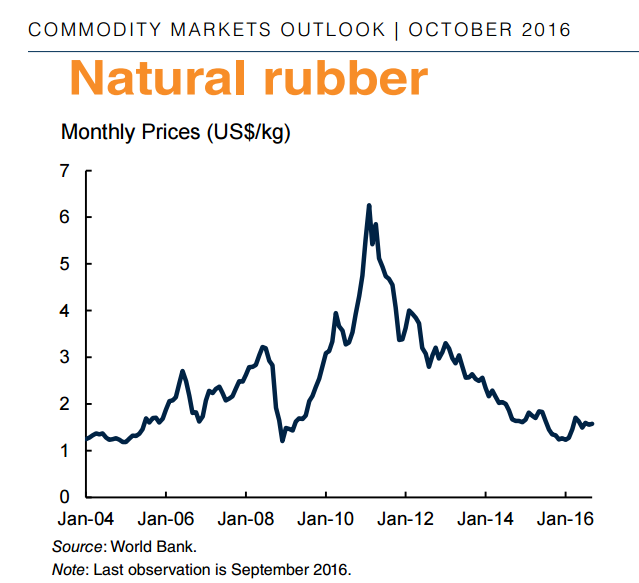

IMO, price of rubber is more important to the industry than radialization. As rubber prices are dropping, cost of new tyre is not too much higher than cost of a retread. Customers would opt for a new tyre than retreading spent tyre.

http://pubdocs.worldbank.org/en/143081476804664222/CMO-October-2016-Full-Report.pdf

3 Likes

Excellent report being share. Appreciate same.

If you have link of current Concall, kindly share.

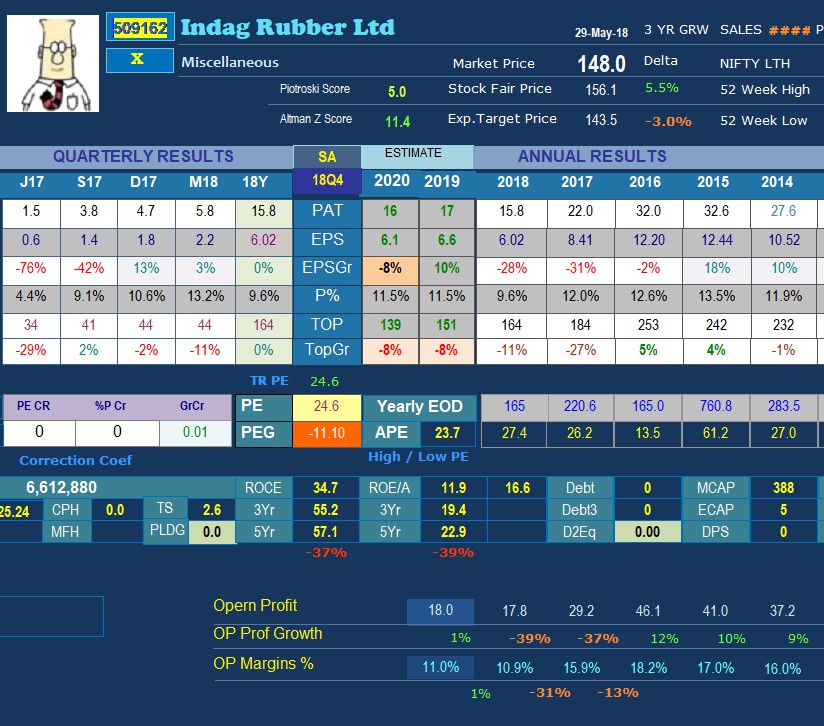

Why the stock price is going down, i did not see much difference in the earning of 2018 and 2017. It is looking normal. No difference in promoter holding and debt as well. Anyone have any idea.

Or it just the fluctuation impact?

Have analyzing the price decline since last one year and found the reasons :

1: sales is continuously decreasing since last 4 years due to competition from big players like J.K Tyre and Chinese import of low cost tyre.

2: The cost of raw materiel is increased from 2017. but now it is stable in 2019 at somewhat low cost. It may help in 2019 and 2020 numbers. I am positive on it.

3: Due to GST and demagnetization, the market is disturbed and it impacted the IRL. As the dealers are not keeping stock with them, and it causes the IRL inventory to increase and the dealers also hold the payment of IRL it causes the debtors days to increase. SO overall the money is stuck in the inventory and with debtors. GST affected the state transport unit business, that also one cause of reduction in sales and less profit.

4: The cost increase in raw material is not passed to the customer as there is no MOAT in the business. The unorganized market of retreading industry is huge. Only the positive aspect is IRL have more than 25 depo all over the country and PAN india network present and 180+ patterns. Anyone, have better idea on MOAT, can out his point here. Debt is 0, that + sign.

From the above points, i concluded, that the stock is costly at p/e 21.58 and by the raw material nature the profitability depends on the raw material cost. No MOAT in business. It’s looks for me a short term stock for 2-3 years. For me the fair value of the stock is below 100. I am already invested but will add more below 100 for next 3 years, as the raw material prices are stable on ok ok levels and GST and demonetization effect also over in the market now. The election may play a big role but i am hopeful of modi government.

Share your insight of the stock, if i miss anything.

Disclosure: Invested and will add more

Bumping the thread.

Does this look very attractive to others for the following reasons:

- fall in crude prices => increase in margins

- continued demand sluggishness in auto sector,especially the CV segment looks unlikely to revive this calendar year due to Covid and BS6 disruptions => more retreading needed?

need to watch :

a) unorganised to organised shift in the sector

b)choice between new tyre and retreading when rubber prices fall

Does this look like an interesting cyclical bet for next 6-8 months?

Any inputs @jitenp ji

Respected Forum Members,

As per the discussion on Indag Rubber in this forum, i would like to ask if anyone has come across : http://www.elgirubber.com/ ?

This came to my notice today, so if anyone has some ideas about elgirubber can you share your thoughts on this?

Company Description :

Elgi Rubber Company Limited is engaged in providing solutions to rubber industry. It is engaged in the business of manufacture of reclaimed rubber, retreading machinery and retread rubber. It also manufactures a range of raw material, equipment, tools and accessories used in the rubber industry. Its sells its products in various brands, including Jet, Pincott, Armonas, Midwest Rubber, Carbrasive, Ecorr and CRS. Its Jet brand includes a range of tire and tube repairs, and retreading and repair equipment. Its Pincott offers rasp, blades, hubs and spacers. Its Armonas brand manufactures retread process equipment, such as envelop expander, tire cleaner unit, cement booth, tire repair and skiving stations, and exhaust and extraction systems. Its Midwest Rubber brand supplies liquids, and calendared and extruded rubber used for repairing and retreading tires. Its Carbrasive offers brazed carbide tools. Its Ecorr brand offers reclaimed rubber. Its CRS brand offers Cincinnati Retread Systems.

my take on indag

INDAG RUBBER

About

Indag Rubber is engaged in the manufacturing and selling of Precured Tread Rubber and allied products.

In September 2020, the company announced the disinvestment of a 100% stake in Samyama Jyothi Solar Energy. The management declared that they want to remain focused on the core business of manufacturing Precured Tread Rubber.

The company pioneered the cold retreading technology in India.

The products

Read the marked circles

The retreaded tire’s life is 75-80% of a new tire on average, it can also be 100% if used under optimal conditions.

The customers are truck fleet owners, who own several trucks and are in the business of logistics, transport, supplying any and all types of goods among other things.

The customer reviews are impressive.

the key competitors to Indag in the retreading industry.

Midas Treads,

Vamshi Rubber,

Elgi Rubber International,

MRF Ltd and

Jk tires

Approximately half the total market is organized, and Indag has a 20 to 25% market share within the organized sector.

Have a loyalty program consisting of around 3 thousand retreaders.

Have a tie-up with Continental and Delhivery, for retreading their tires and providing other services.

A few years back (2016-17) the ROCE was around 30%, this was due to excise duty benefits, some other tax benefits, and lastly cheaper raw materials.

The raw materials are natural rubber, synthetic rubber, and carbon black.The

company can pass on raw material costs.

The raw material is purchased on a spot basis.

Triggers

Operating costs for fleet owners have increased by 30% to 60% due to higher fuel costs, inflation, and some other reasons. They will be looking to save costs wherever they can, this is where Indag comes in with their retreading products to help them save 70-80% on tires.

The cost for a new tire is 25-30 thousand, whereas the cost for a retreaded tire is 5-6 thousand.

To benefit from electric vehicle penetration, the company has a JV (Sun Mobility EV Infra), involved in the business of swapping stations and smart batteries.

While IC engines will become redundant over time, tires will not.

Hence there will be no impact on Indag caused by the transition to EV.

The organized retreading industry is expected to grow due to

- increasing demand for sustainable and cost-effective tires,

- expansion of the logistics industry,

- rising freight demand combined with improvements in road infrastructure resulting in faster movement of goods.

- Lastly, as commercial vehicle sales continue to recover, the market size is poised to expand in the next few years, creating strong growth prospects in the medium to long term.

The opportunities and things that will help INDAG.

Retreading is easier and more efficiently done on tires that are good quality and are used optimally, as the quality of roads is getting better, the damage to tires will be reduced significantly and thus retreading can be done more optimally and easily.

Looking at new products and chemistries which even exceed the life of new tires.

Radial tires are a type of tire that is structurally stronger and support more retreads.

The number of these tires being used is increasing and can therefore benefit Indag.

Tied up with a company called E-FLEET to collect data on how much money in total is retreading saving for its users. Data for 3500 tires were collected last year. Aiming to track data of 10 thousand tires this year.

This can help them in educating people more about retreading and its benefits, which would help them gain customers in the end.

Also provides consulting services, as retreading is a very complex process. This is an added benefit for the customers which would help Indag gain more customers. Only retreading company to provide both product and service.

The company has till now grown without any marketing, the plan is to increase spending in this area.

Out of the total 8 lakhs retreaded tires, 4 lahks were done by unorganized players. A lot of room is available to grow by taking over unorganized market share.

Cash transaction reduction is what will increase market share for organized players. The smaller fleet owners (lesser number of trucks) prefer the unorganized retreaders, as they are cheaper and ready to take cash. As these small fleet owners get most payments in cash they preferred to also do their payments in cash and therefore went for unorganized retreaders. But after demonetization, these transactions have reduced, and several other policies have been brought in which should help further. Now these people have no option but to do business with branded players, who also have a better quality and longer life cycle than an unorganized seller.

Indag has a total capacity of 18 thousand tons p.a., but the capacity currently being utilized is around 10-12 thousand tons p.a. Indicating that there can be operating leverage in the future.

As capacity utilization goes up the ROCE and margins should go up.

Aims to get 11-12% EBITDA margins, as volumes increase the efficiencies will increase, leading to higher cost savings.

The Exports are currently at an infant stage, expected to grow.

Financials

Q4FY23 revenues increased by 45% from ₹46Cr in Q4FY22 to ₹67 Cr, while their FY23 revenues reached ₹252Cr, up by 46% YoY from ₹173 Cr in FY22. Their growth during the year was largely driven by an increase in volumes.

The gross profit margin was close to 39% in FY2021, which has come down to 30% now.

Ebitda margins have increased from 4% in FY22 to 8% in FY23.

Pat margins have increased from 1.6% to 5.2% from FY21 to FY23.

Lease liabilities of 6cr suddenly hit the balance sheet in FY23.

Trade payables have significantly increased (indicating supply-side dominance?).

An interesting thing to note is that the 20 crore cwip (their current netblock is a bit higher than 20cr) in 2021 was used to buy an investment property, which is leased for 9 and a half years to an MRO center.

Now we don’t know whether it is leased to a third party or a part of their business entity.

But why would a business involved in tire retreading try to earn money through leasing?

Does the management not expect sufficient demand?

They could have invested this money to double their fixed assets and therefore resulting in the doubling of the financials. But instead bought land, maybe for future expansion? A big question.

The operating cash flows, although increased in 2023 compared to last year, have halved compared to 2021. This increase was majorly due to better working capital and higher noncash items.

Consistent dividend payout.

They had a working capital days target of, reducing it from 108 to 90 days and they brought it down to 80 days this year. The next target is 70-75 days.

Another interesting thing is that Indag didn’t grow from 2012 to 2022, instead, it degrew both topline and net profits. But suddenly the sales increased in 2023 (a bit higher than that of 2012) but the margins are still low at close to 6%.

What needs to be seen is whether they can sustain the growth they showed in 2023, or was it just a one-off.

5 Likes

Sir, they are guiding for an EBITDA Margin of 10% -12%. Also, crude price is falling, so do you think it will give some benefit to them??