Also a terrible AMC like IDBI which had 50% of AUM in liquid funds got valued at 4.5% of its AUM. Based on that and listed comps IDFC which is growing its AUM by 50% YOY and only has 10% of AUM in liquid funds (both HDFC and RNAM have 30%) should easily be valued atleast at 6-7% of AUM.

IDFC seems like a real no brainer, see the attached detailed analysis from a user on VIC.

IDFC.pdf (61.5 KB)

2 Likes

Can someone please give negative viewpoints on the stock.

I am super bullish and would love opposing viewpoints.

1 Like

In lending it is never a great idea to grow very fast… quality of loans may suffer… lot of scope for things to go wrong

Now with DDT gone expecting a Rs 4.5 dividend in the next few months

DDT is gone, but the dividend received will now be fully taxed in the hands of the shareholder. Thus as dividend gets streamed up every entity will have to pay tax at corporate tax rates on the dividend received.

In effect the net outflow will actually be slightly higher than in the DDT scenario.

No that’s not correct, holding companies receiving dividend will be allowed a deduction on that income.

“The government has allowed deduction for the dividend received by holding companies from their subsidiary to remove the cascading effect.”

1 Like

Also idfc is up streaming 700cr of cash from sale of subsidiaries using capital reduction anyways, not via payment of dividend. Please see their latest presentation for details.

You are absolutely right, I missed this bit. Thank you for correcting me.

Anyone know about when they will be conducting the conference call for the 3rd Quarter Earnings.

2 Likes

Now that IDFC First bank is raising money, will IDFC be forced to keep stake at 40%?

What if it is not able to do that?

Yes IDFC cannot trim its stake until October 2020,they will have to subscribe to the issue if it happens before that.

That would be bad for shareholders of IDFC because then IDFC may suspend the payment of Rs 640 Crores dividend partially or fully to infuse capital into IDFC Bank.

The sad part is that this capital would most likely be used by the bank for provisioning rather than growth,not to add that the bank’s stock is trading below book value and any capital raising below the book value will be value destructive for its existing shareholders including IDFC.

Let’s wait for May 1 to see how much money they are raising and consequent dilution.

1 Like

If you think about it not the worst outcome, if holdco is subscribing to shares at such a low valuation then it might make more sense than paying out a dividend which gets taxed at 20%!

It is not a good outcome,when the assets were monetized they were done so with the stated intention of distribution to the shareholders of IDFC limited.

Dividend income is taxable in receiver’s hands, DDT has been abolished recently.

Yes but you need to pay tax on it now and not the Company. Infact if you are in the 20%+ tax bracket you are worse off now than when DDT was there. Yes ideally assets should have been distributed and they were on track but Coronavirus changed the situation, unfortunate and beyond anyones control I guess.

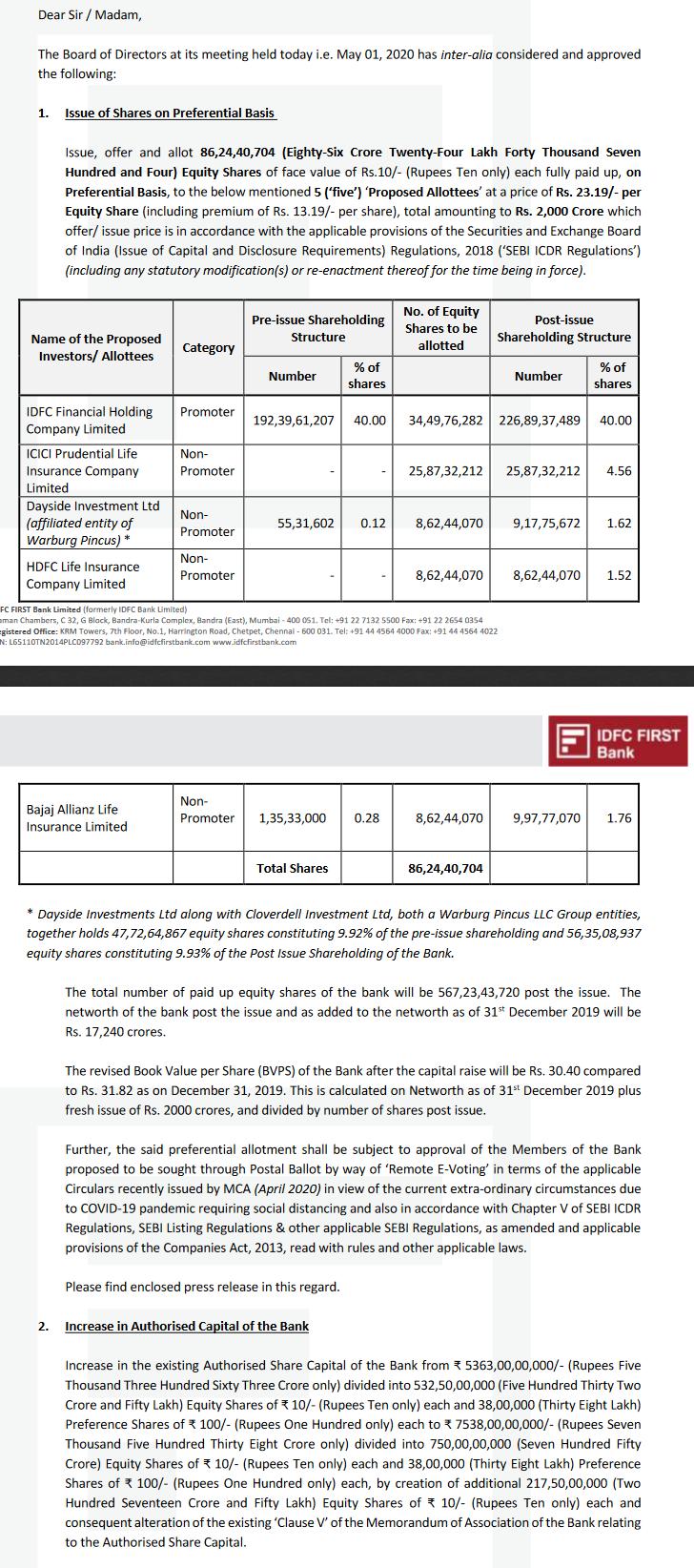

As you can see in the above release by IDFC Bank,it has decided to raise capital(Rs 2000 Crores) by way of preference issue at Rs. 23.19 per share which will dilute the bank’s book value from Rs. 31.82 per share to Rs. 30.40 per share.

It is not a good outcome for IDFC Ltd. shareholders,when the assets were monetized they were done so with the stated intention of distribution of the proceeds to the shareholders of IDFC limited.

Was the situation so dire that the bank could not survive another five months when IDFC Ltd. will no longer be obligated to maintain their holding in the bank.

Now the bank has taken another Rs 800 Crores of capital form IDFC limited,the money that belongs to the shareholders of IDFC Ltd.

Why was the bank so desperate to raise funds at this juncture when the share price was trading below book value,if the bank was confident of delivering on its performance it should have waited for the markets to recover and then raised growth capital on favorable terms,especially when the management had made tall claims about how resilient their retail book had been over the past few years.

This has altered the risk reward for shareholders significantly with no dividend likely and now returns will depend on how well the bank and AMC business does until there is any corporate action with demerger or sale.

3 Likes

Not sure many were buying for the dividend.

If I have 100Rs that I invest and get 10-15 Rs back as dividend(depending on buying price), I end paying tax on my recently invested money.

That doesn’t make sense. Good that the promoter has supported the bank which is the main asset of IDFC Ltd.

True that the intention was to give it back as dividend but nobody could have predicted the Coronavirus.

I would not comment on how many people were buying for dividend,the money belongs to shareholders of IDFC Ltd.

I think in the interest of transparency and good corporate governance IDFC Ltd. management should take shareholders approval before committing more capital to the bank.

The dividend of Rs 640 Crore works out to Rs 4 per share,which works out to 27.5% yield at the current market price,this is very significant and cannot be dismissed by rationalization that tax is payable.

On the question of promoter’s support,why does the bank need more support now?

As of last quarter the bank had Tier 1 capital adequacy of 13.28% and what was the rush to dilute at such a low price?

The bank’s MD Mr. Vaidyanathan had said in March that retail NPA’s had come down when he had sold shares to repay his esop loan.

1 Like

The dividend was a major consideration when I bought IDFC.

I thought 30% is covered by the dividend and remaining is the valuation of IDFC AMC itself and hence even if the bank goes down the drain, I am covered. I did not consider that this dividend money also would be put in IDFC First Bank. This Googly has made the risk reward ratio unfavorable…

I am considering booking losses and exiting. No confidence in VV as he has been overly positive forever while making continuous provisions and selling off a chunk of his Esops also. It is easy to lend money but when recovering only you know whether u lent it to the right people. Considering the aggressive lending happening here, I feel it could be risky.

1 Like