for those who are worried about “Increasing physical infrastructure by 4x and reducing cost almost by half”

one must discount the fact that

bank also got an additional 200 branches of capital first

so, they can even convert them to bank branches & it will far cheaper than, making branches from the ground up like other banks.

This surely give them cost benefits

Disclaimer: Invested 70% of portfolio as it a potential turn around

You are adding extreme business risk to market risk. While we have no control on market risk, we can certainly avoid business risk. I made the mistake of putting little too many apples in one basket and I repent doing it as the risk is unwarranted.

Yes sir i fully understand the risk . i believe in very focus portfolio not in diworsification/diversification.(i mostly keep 4-5 stocks at max at a time).

im here for very long term in this counter if things turn around and this increase at-least by 15% CAGR. regardless of stock price. (cause Bank are unique business & can have growth story of even like 100 years) .Also my Buying price is around current book value try Rs 33.6 ,so i have 1-2 quarters to decide the turnaround max.or can fine tune the portfolio as story unfold.

This is a “head i win huge, tail i loose very little” type tactical bet

I have counted total number of branches of IDFC bank from bank website and the number is 271. It means bank have added 29 new branches in first quarter. Correct me if I am wrong

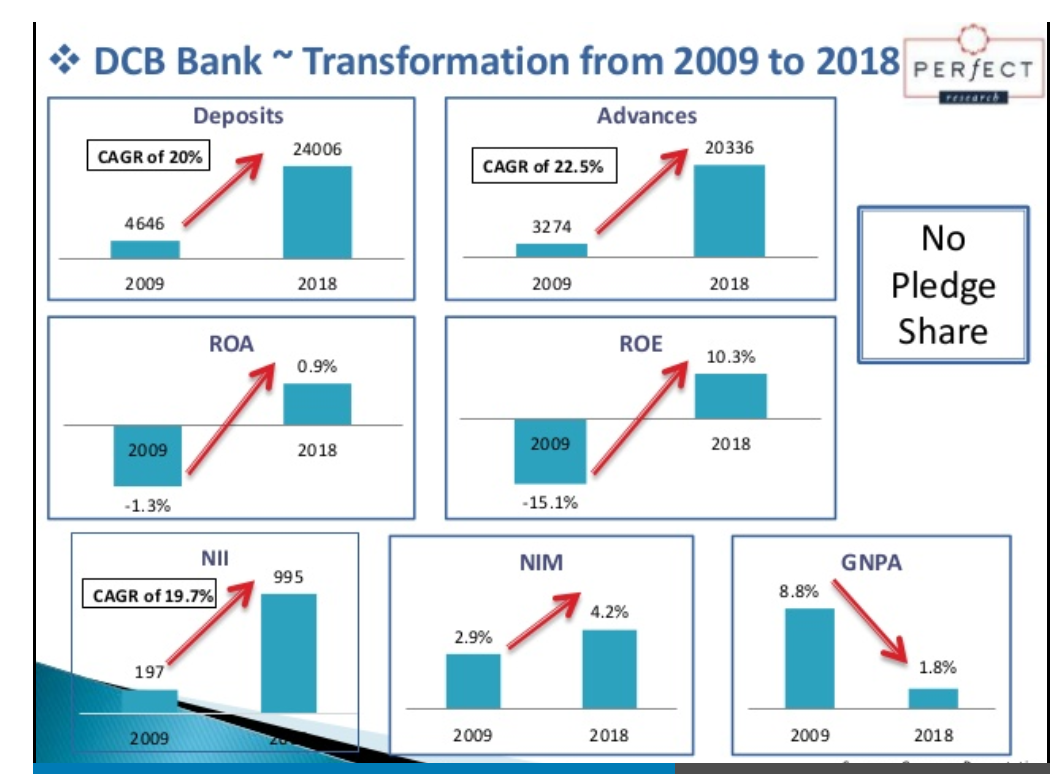

Interesting read about DCB bank… Few years ago management decided to expand branches and increase retail banking… Market downgraded it and stock price tanked. What happened afterwards is a history…

Will history be repeated in IDFC bank? Well time will tell but even interesting thing is DCB bank had 8% NPA at that time while idfc first has below 3%

O.K. I understand. In my opinion 2009 is not comparable to IDFC Bank. DCB Bank is a turn around story. After 2009 they closed many branches to reduce cost. They stopped all types of risky loans like corporate loan. Started building granular assets with mortgage. Once cost and NPAs reduced, they started opening small small branches to run on reduced cost.

In 2015, they decided to expand fast as the company was enough strong to bear the stress of cost increase. It was done to occupy the space as first or second mover in tier 2,3,4 cities to be able to face competition. Company doubled branches in 2 years. This time NPA s were less than 2 %. DCB Bank management always say that they don’t care if GNPA is less than 2% and NPA less than 1 %.

Disclosure - Invested in DCB Bank and watching the progress/execution in IDFC Bank.

Is not the expansion story n then the market reaction came in 2016 where as the NPA issues are much older. Both happened at different point of time if I remember ? Dr Malik’s blog captures all this in detail in one of his blog

Looks like the bank has finally started charging customers for not maintaining AMB.

I closed my account around a month back in June but received a SMS yesterday saying I will be charged for not maintaining AMB for May. While I am not sure how they’ll do the same since account is already closed, it’s good to see that they have started applying AMB charges.

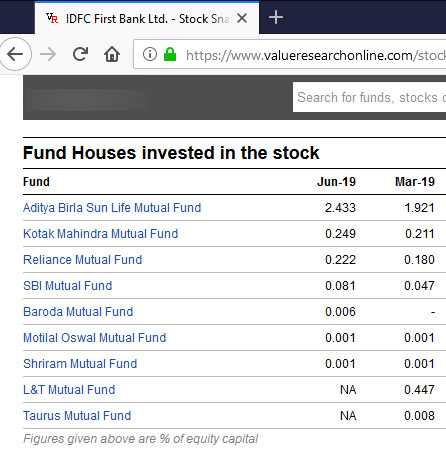

Although I don’t read too much in these selling or buying of the MFs (which they can do if they feel better opportunity has emerged, not always because the exiting opportunity has gotten worse), I wonder why there is discrepancy in these two sources! Whom to trust?

Very keen to know, @hitesh2710 sir, what is your current technical value of IDFC first? it has been on a tail spin and now about to breach support at 40

I have observed one thing which many investors might have already identified.

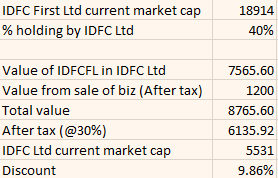

IDFC First Ltd Vs IDFC Ltd.

I am interested in IDFC First bank. But I am confused if I should invest through IDFC Ltd or directly in to IDFC First Bank as IDFC Ltd is providing extra margin of safety.

I would like to know why there is a difference in their pricing (Even after considering the tax effect).

Please comment your view as I want to know more about the same…

Find details below:

Rs. in crore

Discount of ~10% and I have not even considered value of AMC biz yet. At the moment, this discount rate is just 10% (~40% before tax) but many times it becomes more than 25% (55% before tax) and that too before considering AMC Biz.

Now, I need help on the following things:

If anyone has knoledge about the AMC biz, can they help me value that biz?

What should be the effective tax rate for holding co?

If they consider to transfer the benefit of asset sale of Rs.1200 crore through buybacks then there will be lesser effective tax rate to be applied. Is that understanding correct?