I believe people buying the merged entity are buying it as a growth stock and not a dividend paying stock. More likely than not the earnings will be reinvested and dividends will be muted. I have not seen it but a study of past dividend paying record of CAPF would give some idea about future dividend payment policy of merged entity.

On the other hand there will be 40% holding from IDFC and it will have a larger say in the matter. Since it can not off load the shares it holds it will look for dividend income rather than notional profits in its portfolio. Lastly, considering IDFC is selling its other businesses it is quite possible that the IDFC triplets will reverse merge like ICICI and ICICIBank. It will be a good idea to simplify the current 3-tier structure in the IDFC camp. So, lots of possibilities are there.

Disclaimer: My primary objective for investing in IDFCBank is growth.

Hi,

I hold both the Stocks as well in my long term portfolio. Curious to know your view on if one has to add or load up more, which Stock of the two offer better valuations from arbitrage standpoint ?

Buy Capf. Both stocks are ex-dividend now. Just Multiply IDFC bank’s CMP by 13.9 (swap ratio) to know the equivalent Capf price.

RoE(annualized) of Capf increased in 25 quarters from 2% to 16% (In q1 fy19) -

As @vicky_7900 has pointed out CAPF for some unknown reason is available cheaper than 13.9 times IDFCBank. For retail purposes both stocks are liquid so it is better to buy CAPF if it is at discount considering the swap ratio,

Apart from this arbitrage somewhere around Dec and Jan the FO will cease in CAPF so if you rely on monthly option writing or spreads or roll overs then you may miss on some income for a couple of months in CAPF. The IDFCBank FO can be rolled over with no problems.

Lastly, if you want to protect yourself from the remotest chance of the merger being called off then it is better to buy CAPF. Just painting the worst scenario. The possibilities are next to nothing. Regards,

Most analysts prefer not to guage the worth of a bank from the Price Earnings multiple. Earnings are a combination of

1 - Spread

2 - Credit costs

3 - Growth in Advances

4 - Operating Costs and

5 - Leverage

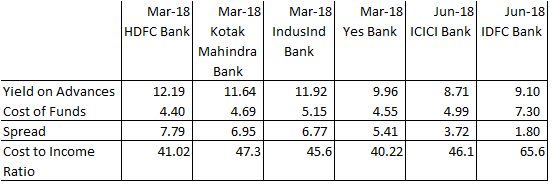

- As far as spread is concerned, IDFC Standalone has miles to go to match HDFC Bank or a Kotak Bank. Mr. Vaidyanathan has stated in the Bloomberg interview few days back that their main focus would be on the liabilities side to reduce the costs of funding.

-

IDFC has some legacy long term borrowings at 8.8% as per Investor presentation which make up around 21% of its deposits. That is a major drag.(Does anyone know when these borrowings would mature?)

-

We have seen in the recent past Banks like Yes and Kotak aggressively increasing CASA by offering 6% interest on savings deposits. I think that would be the most likely recourse for IDFC Bank as well to reduce overall costs of funds.

-

Merger with Cap F may improve Balance Sheet and the Credit Rating.

-

The yield on Retail advances of IDFC Bank dropped to 14.8% in Q1 FY19 from 16.2% in Q1FY18 and from 15.7% in Q4FY18. It is probably so due to increase in Mix with higher share of low yielding Home Loans.

Moreover, increase of spread is a gradual process with things like change of mix of advances, increase in CASA, increase in credit rating etc. taking some time to reach the levels of the other peer banks.

-

Coming to Credit costs, around a 3rd of IDFCs 75k crore loan book is infra loans which might can go through some pains in recovery. Credit costs of Capital First also (Including write offs) are much higher compared to Bajaj Fin. I expect the higher credit costs to continue esp since new management would like to clean up books at the new entity level after takeover. Again on this parameter, there will be some time before they match levels of peers such as HDFC and Bajaj Fin

-

Enough has been written on this thread about advances growth in Retail which is commendable. But if Infra Book has to de-grow or not grow then the blended growth in Advances would take a hit. Moreover. to compete with the likes of HDFC, Kotak, Bajaj Fin who have a PAN india presence, strong relationships with intermediaries, established manpower strength is again a challenge. Can the bank grow its blended loan book at 20% + consistently?

-

Operating costs are high and will increase post merger for things like re-branding, marketing, branch opening, recruitments etc. Moreover, beyond a point i feel scaling up is required to reduce operating costs.

-

The Bank may not want to leverage itself immediately after merger considering that it may borrow at cheaper rates in course of time which a better credit rating, better Balance sheet, greater CASA share. On this front also I feel the bank would lag behind its peers.

To summarize, it will be a long process for IDFC Cap F merged entity to bring its ratios in line with the peer banks. In a long period, many external variables can change for eg: New entrant like Foreign Bank, New Technology, Privatization of PSU Banks. Market forces are the strongest and generally bring the price of a share towards its worth. I feel IDFC certainly offers promise, but in the background of this uncertainty, one has to take a leap of faith to hold it for the next 5-7 years and hope that all goes well. Many would chose to keep hard earned wealth with stocks like HDFC Bank which offer a high degree of predictability of future results.

My personal choice is to keep money in stocks like HDFC Bank and Kotak who are in a far better position to capitalise of the next wave of opportunities v/s someone like an IDFC Bank.

Having heard Mr Vaidyanathan and Mr Avtar monga, it does give a feel that they are on top of new trends and technologies.

Given that the bank started it’s first branch in Feb 2016 (as per Mr. Lal), the need to open more branches, the cost to income ratio would be high at this point. New branch requires 24 months to break even as per Lal. It was an infra lender, and 3 yrs back arnd 12 k crore of the book was stressed, now it is 5000 crore(after taking hits, selling to ARCs, some stressed assets like steel going normal again etc.) PCR on these 5000cr. stressed assets is 77%, and after 600-700 cr additional provisions in Q2, it will be 90%.

Mr. Lal says the book will be squeaky clean after this. One may get confidence in this statement through relative valuations of capf and those of idfc bank. CapF is perhaps trading at 1.8 times fy19 BV , 12 times fy19 earnings, with 25% growth rate, increasing RoE, say 17% RoE for full year fy19. So basically at CMP it is cheap (without merger). They would have thoroughly examined idfc bank’s assets before merging and deciding swap ratios. In fact Mr Vaidya has been saying from may-june that idfc bank has to take 600-700cr prov. as per Mr lal. At that time, Lal had only said publicly that in worst case they will have to take that much provision. The point is that if CapF is cheap at CMP (without merger), the chances are that idfc bank is also reasonably priced at CMP and is not expensive.

- Price = PE * EPS is the basis of my calculation. This is true irrespective of the biz it is and what parameter the sector is valued in.

- The risk factors like foreign banks, technology etc is same for all including the blue eyed boys.

- Frankly, HDFCBank has always been a puzzle to me. I had a salary account with it and I have never understood why would anyone do any business with such an entity. But people do. I asked my friends why on earth do they take a home loan from this bank (or HDFC) and I have never got a clear answer. So, the twins must be doing something better than others as my friends are much smarter than I am. But frankly I have no clue.

- The NIMs of HDFCBank are in fantasy land. It has the most to lose. Where do they raise their money from? All CASA?! Do they have any foreign currency risk? I don’t know and I am not really interested for the simple reason the stock (IMPO) has always been costly to purchase for Indians. Foreigners with near zero interest rates and unlimited liquidity are happy to invest in a biz with a yield (E/P) of 2-3% Indians can not.

- You are most welcome to avoid IDFC Bank. Our financial background, needs, ideas can be different. Regards,

Thanks for your feedback. The worst case scenario you pointed out is precisely the reason I have been adding CAPF Vs IDFC. Both combined is the top holding in my portfolio and currently accounts for 8% of my portfolio.

I am not sure this is a good idea because this will bloat the equity even further. Today the equity plus reserves of IDFC Bank and CapF together is about 18,000 crores. Add another 12,000 crores approx from IDFC and RoE will tank even further. To make even 15% on this capital base, the merged entity will need to generate a profit of 4500 Crores per year! There are some SF banks like Ujjivan and Equitas (which I am invested in) and which have an MCap in that range.

I agree that there could be some dilution. However it will not be as bad as you have mentioned. We need to see that the 40% stock that IDFC owns in IDFC Bank will be extinguished. If all IDFC holds is shares in IDFC Bank and cash from the recently sold businesses then after netting the cash with it’s own NPAs the reverse merger may not be as equity dilutive as you have pointed out. I have not done any calculations as it is still speculation. The resultant entity will be much more free to take its own decisions with a lot less of red tape. That was my reasoning for calling it a good idea. regards,

Interesting point. Had not thought about it. Can anyone please come up with calculations to give an idea of equity dilution if IDFC were to reverse merge itself with IDFCB + CapF?

From concall:

1st branch started operations in feb 2016

Highest retail-CASA branches are contributing 200-300cr of retail CASA

There’s 136 urban branches, 70 semi urban branches [total 136+70=206 branches ] plus 325 Idfc bharat branches.

Median Urban branch is expected to contribute 100-120cr CASA in 3 years. 136 urban branches are expected to contribute 15000 cr of casa in 3 years.

Retail CASA 2100cr. Expected to reach 5000 cr in fy19. Retail TD 5300cr. Wholesale CASA is currently 4000cr. Total CASA in fy19 expected to cross 9000cr.

Other information -

Capital first’s 60 odd branches will act as limited liability branches and full-scale asset branches.

New management plans to open 200+ new branches in fy20 as per my information.

Saving bank interest rate for idfc bank is 4%, but FD interest rates and other benefits are amongst the most competitive.

Increasing visibility - advertisements, new branches (15 each) in Mumbai, NCR, IDFC bank booths in public parks etc. (was served cold drink in one such booth)

Disclosure : invested, views may be biased. Not a financial advisor.

I only have one thing to say compare IDFC Bank to Bandhan Bank both received Banking licence on same day… both have different backgrounds… but see the difference… believe in Rajiv Lall the story teller… he kept on telling stories… ended in wealth destruction… see bandhan bank…

To further your argument about competitiveness of Lall, the reason BL was given to IDFC in the first place was because of their special status as Infra lender. Now they are saying they don’t want to lend to infra but build retail assets. So why should the BL not be taken back from them? Just a thought.

As per my calculations and today’s disclosures, IDFC has purchased 8Cr 75L shares in IDFC Bank. So its stake in the merged entity is now 39.43% It needs to take it to 40% for which it needs to buy 27,201,972 (2Cr 72L shares) more shares.

Actually initially I had thought that purchasing 11Cr 47L shares from open market would move the IDFCBank share price significantly. I was wrong. FPI selling was so intense that the price has not moved much from where it started although there has been a swing. The shares were purchased at an average of 41.20 per share with min-max of 36.82 and 44.18 per share. regards,

-

25k-30k-35k crore, whatever the CASA is after 3 years, would directly replace the borrowing done at 8.5% to 8.9%. One can make out the additional profits. In addition, there would be retail term deposits too which will reduce cost of funds.

-

Having heard a dozen+ bank/NBFC managements on concalls/interviews, I think there is none more passionate/committed than Vaidya. nice read https://www.capitalfirst.com/pdfs/v-vaidyanathan-secret-diary-of-an-entrepreneur.pdf

Leads me to believe that since idfc bank + capF is 1.1 times combined BV, and very few FIIs, MFs own it, there’s scope of very fast appreciation as well as massive long term potential as soon as people start to realize the opportunity.

Disc: invested in CapF, views are biased.

There’s a flipside to this, there are also crores of retail shareholders who have been stuck in the counter for years. Don’t forget the massive equity base, which, as you said, is not held by institutions. I wouldn’t be surprised that it will take a lot for the stock to have “fast appreciation”, a couple of quarters of good performance will not do it. Hoping that one fine day the sentiment will change universally and you will have “fast appreciation” is pure speculation and hope.

I have never understood this argument of large equity base hampering price appreciation. Merger is immediately EPS accretive (see prev posts) so new shares are bringing in more good biz than they are paying for. On top of it 15-20% CAGR is expected by Vaidya. The PE is suppressed and can see a re-rating.

Price = Earnings x PE so where is the question of large equity base? It is just a fashionable excuse / a myth spread knowingly or unknowingly, every time the stock makes an up move. If you believe earnings can not grow or PE remains half the average of private sector banks even after 4-6 quarters then that is your opinion.

RIL has larger equity base, more debt, and lower margins than a bank (obviously) and still it has no problem in appreciating when the big guys want it to be. Besides what is he free float post merger? 40% by IDFC, 10% by Warberg, 3% Vaidya, 7% Govt of India, another 10% Goldman Sachs, Govt of Singapore - so close to 70% is not coming in market at all.

Equity expansion will happen and it is not bad. you are right in saying that it should looked from business growth and EPS perceptive. There are so many examples of companies with huge equity base & they have given decent returns … RIL is one of them … Mr. Vaidya has time & again proved that he can turn things around, with 3% equity he is committed too. I don’t see any reason why IDFC bank can’t grow, if economy can grow @ 7-8% & public sector bank continue to lose business.