I would like to continue writing on this topic while slightly digressing away from the initial objective of valuations and maybe more towards the business/process aspect, and post that creating a set of factors/observations that repeat in successful playouts.

It should be done by moving a bit backwards and understanding the whole process of CIRP/IBC along with several case studies, with the motive of explaining everyone as to how one can play this style.

I am myself discovering my way through this style as a new entrant, and unable to come in contact with people who do this in depth and can teach me, so my knowledge should be very rough around the edges ofcourse.

The previous replies in the topic got very stock specific and thus not insightful in terms of understanding this process/style, i would like to get more truer to the primary topic of IBC/CIRP, started by @dd1474. Ofcourse there would be company names, but only with the motive of synthesizing the key pointers from it that need to be followed while following this style of investing, and maybe take up the business in its own individual topic if needed rather than discussing in detail on it in this topic.

So first of all what is CIRP/IBC/Insolvency

Basically firm A took some debt from firm B to grow its operations, for any and every reason these funds couldnt be used in the best way and yielded nothing for A. As A didnt make any money off of the borrowed amount, they couldnt pay the interest costs to firm B.

Now B first tries to settle the amount through OTS (one time settlement)/any other way at a reduced amount and gives more time to A (this may not happen every time, and A can directly go under insolvency before these other measures), but A still hasnt been able to payback B.

Finally B goes to NCLT to lodge a case, A is then declared under insolvency.

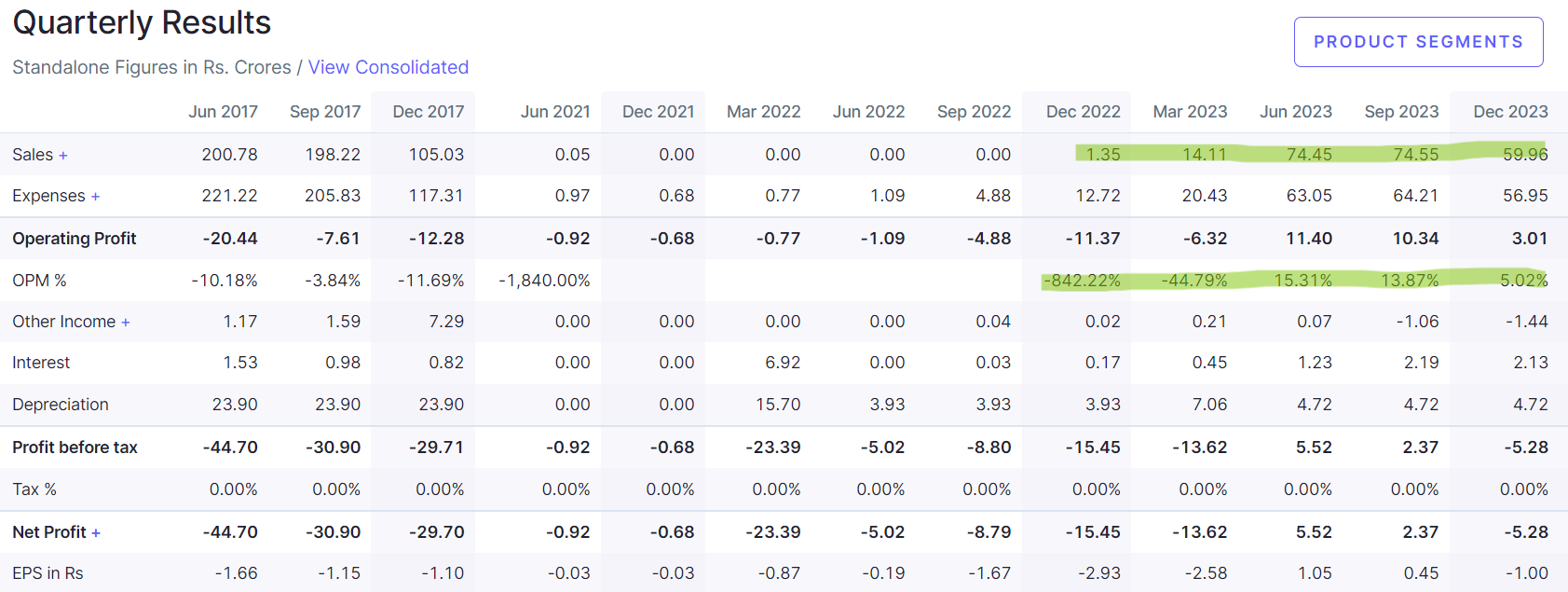

While being declared as insolvent most of the firms are loss making and some even do not have any sales. So no need to get alarmed by seeing that, as these firms do now have access to funds (wc), they are unable to carry on operations.

The next thing that happens is that the NCLT in unison with B brings in a resolution professional (RP) to helm the ongoing operations (while the previous management loses control over the company) and come to a solution.

The solution the RP can come to is to either liquidate the firm or bring in a new management (resolution applicant/RA) who infuses funds to pay back B and revive the operations.

Now if there is no resolution applicant, the firm goes under liquidation, we investors dont even need to look at it as it does no benefit us in any way.

The game is to be played if a decent/capable RA comes in.

The steps

-

B lodges a case in NCLT against A

-

Appointment of RP

-

Meeting of committee of creditors (B and other entities like B)

- Mind it, there are several meetings before they come to a decision, and this whole process is very long

-

Announcements in newspapers and other mediums by A, in order to invite bids (expression of interest- EOIs) from RAs

-

Then EOIs comes in from RAs

-

Then few more meetings of committee of creditors (coc) takes place in order to select a SRA (successful resolution applicant) and their rp (resolution plan) submitted by the SRA

-

Finally after a RA is approved from coc, it then needs approval from the NCLT

-

Post approval an implementation and monitoring committee (IMC) is formed, consisting of the RP and the RA, who take over the board and keep watch on the progress of the rp submittee by the RA.

-

Finally after some time IMC leaves and the whole control is given to the RA, and the RA starts bringing in new board members

-

While submitting the rp, there is also a clause of reduction in capital.

- This means that majorly (90%+ usually) of the shareholding is diluted and the whole control is given to the new management.

-

Now since 90%+ shareholding is with the new mgmt, according to the sebi rules they need to bring it to 75% ans below, now to do this they either get in an investor or OFS it to the public.

Thats the basic summary of the whole process.

If anyone uses this style extensively please share the granular points and learnings.

Will share case studies soon, the idea behind sharing case studies would be to understand the space better along with achieving the ability to gauging the future outcomes more accurately.