IOL chem benefitted due to disruption of ibuprofen supply due to problems at BASF. Here one needs to keep track of how long the supply side problems of the molecule persist and act accodingly.

1 Like

PSP Projects i have been invested since ipo and bought big on listing day @190 and 210 in June 17. It beautifully negates the perception that IPO seldom make money for investors. I liked the co as management was first gen technocrat owner entrepreneur driven.he had named the co after himself and wud try utmost not to sully his name and reputation.

Roce was healthy ,free cash flows were ther and good Roce .a little bit of scuttlebutt reaffirmed the view that co takes very good care of its employees and labors.enjoys a great reputation on finishing even complicated projects on time. promoter stake was nearly 73%,gave good div yield,almost all the nos showed it to be a big exception among construction cos.

Moreover it had completed MARQUEE construction projects like Sabarmati riverfront and Gujj sectt which had been left in complete by previous contractors.This enabled it to have a good connect with PM Modi and its also completed the BJP HQ interior work in Delhi.SDB project bagged N EXECUTED wud lead it to next orbit,

Mgmt seemed very confident in last AGM of maintaining 30-40% growth which combined with good ROCE is an ideal combo together with good reputation and execution capabilities of co and opp size increasing , If these characterstics are present in any co all one shud do is to buy and hold it for long .wealth wud be created automatically.

11 Likes

Sir one company from same sector is HIkal which is posting good result for last many quarters but price remaining in a range bound…

Other company is GMM Pfaudler… Valuation wise it seems to be overly priced… it is benefiting from mainly capex in Agro due to china disruption…but how long this will play out …? what should be the exit point from these type of compnaies…?

1 Like

I was about to ask for GMM Pfaulder as well. Given that Speciality Chemicals is benefiting not from China issue but also that India is emerging as alternative or a risk mitigation location, more and more Indian companies are enhancing capacity. Given the latest tax moderation, an additional incentive to quicken capacity enhancement has arisen. The equipment and systems providers like GMM and Swiss Glass operate in a virtual duopoly. Do they stand to have windfall gains?

I am never able to answer the “Valuation” part as this Specialty Chemical story is still emerging and know one really knows how big it can become(or not). Really appreciate if @hitesh2710 can share his views on this.

1 Like

Hikal after being hit due to issues of forex losses due to foreign currency borrowing for a few years, lack of growth etc now since past few quarters has posted very consistent growth numbers. Even the articulation in concalls and annual reports looks bullish about the company’s growth prospects for next few years. The recent tax cut also should help its cause.

I am.invested in hikal. To me it seems on the cusp of few years of consistent growth.

Gmm pfaudler i had discussed some months back. Its a safe way to play the capex theme in speciality chemicals, agrochem and pharma space. After a sharp run up i exited gmm as i felt the current correction offers more attractive alternatives. Swiss glasscoat is a comparable peer.

9 Likes

@hitesh2710 ji,

I have tracking positions in two interesting small caps:

- Himadri Speciality Chemicals

- Apcotex Industries

Both of these seem to have the ingredients mentioned by you. Would like to hear your insights on these companies if possible.

Thanks in advance ![]()

1 Like

thank sir,

good to hear that u too invested in Hikal…One thing i want to ask about it that its avg median PE for last 5-7 years is around 25 when growth was not too high but today when it is consistently growing at 18-21% and growth visibility is also there then why it trading at lower ratio around 15-16 PE multiple…

Second about GMM, i am invested in it so what things i should keep in mind to trigger exit button whether its order book decline, margin contraction, growth falters…

thanks sir

2 Likes

Hi @hitesh2710 . There was a lot of euphoria around 5 trillion economy, corporate tax cut etc. But the situation in financial space is scary. All the PSU banks already had a huge reported NPA. Now we have the same issue in quite few private banks/nbfcs. And these are not small companies. The price action in most of these private financial seems to imply a serious issue. As we know, there is no smoke without fire. For all these companies, there might be further slippages in the future ( In addition to what is already factored in). Considering the size of the companies and the extent of the NPA, it looks very scary to me. What worries me is a possible systemic risk due to these events. Do you see a systemic risk ?. Or can we assume RBI wont let it happen.?

The average median PE you mention was during a roaring small-midcap bull market. Now the situation is different. Currently there is total apathy for small-midcaps and that’s where I feel opportunity lies. There is always reversion to the mean so at some point in the future, there will definitely be market fancy for such companies. All we need to do is select good companies and be patient.

Regarding GMM, I think one needs to keep a close watch on order book and capex announcements from the client companies. But one has to be quite clear that it is not a buy and hold forever kind of company.

7 Likes

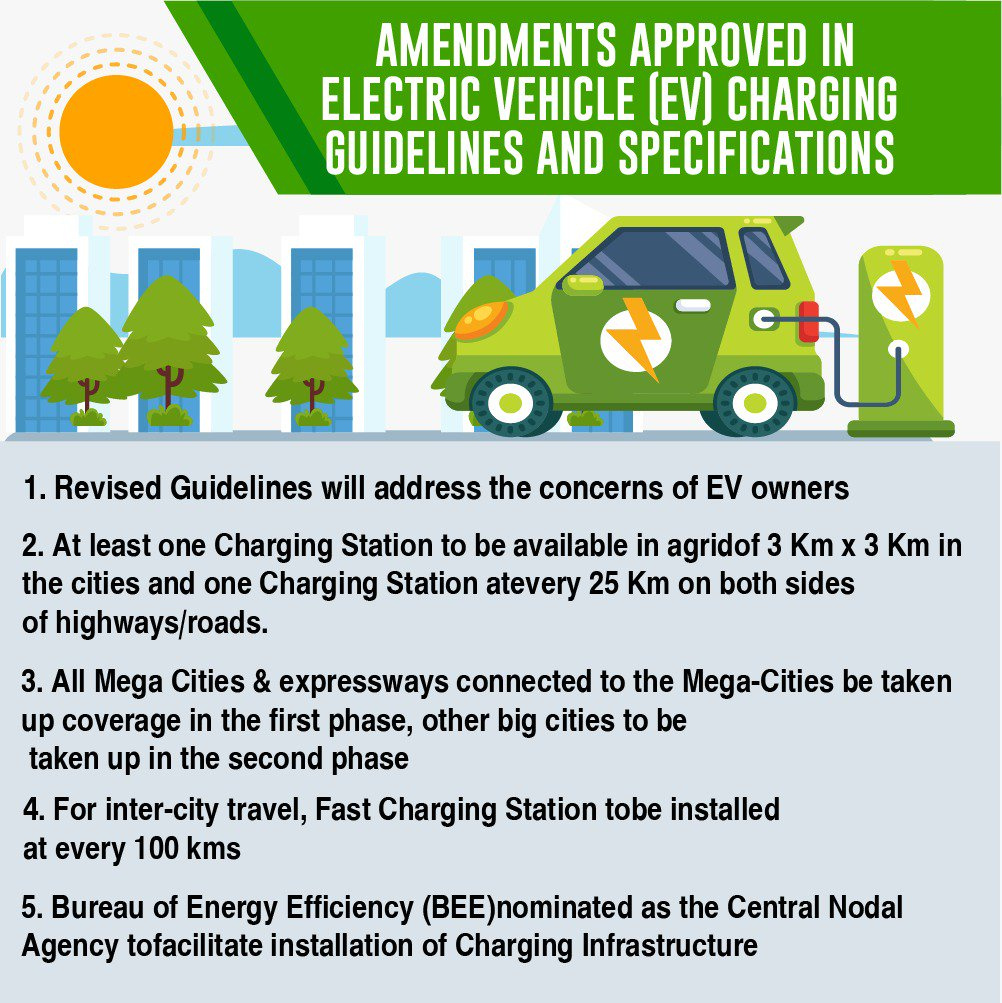

Hi @hitesh2710 sir!

The electric vehicles seem to be getting their traction and govt planning to implement the following amendments to improve the EV infra.

source: Press Information Bureau

Although some of these are very ambitious, to be practical 5yrs down the line, at least we can expect to see charging stations in 50-100KMs range in highways. This should benefit the power companies, some companies like Adani power, Adani transmission, Torrent power, power grid are trading at their near 5yrs high even in this carnage, but most of other PSUs like NTPC, NHPC, SJVN, PTC are languishing, even other beneficiaries like BHEL are languishing (Guess, the market doesn’t want to touch the PSUs, not even with bargepole ![]() ).

).

- Generally, your opinion on ICE to EV transition?

- What’s your view on the private companies like Adni group, Torrent, Tata and Powergrid, IEX, REC from PSU pack?

Thanks!

2 Likes

thank you sir,

Yes GMM is not a buy and hold type of stock…will keep watch on its order book…

Hitesh Ji,

I wanted to ask you, regarding usage of technicals to book profits from your long term holdings. For eg:- if you are holding some stock from last 2-3 years and it has given you decent returns (90-100% in absolute terms) and is showing some bearish signs on the technical charts. Will it be good to book profits in such cases ?

I am talking from the perspective where we still believe in the long term story of that stock but the signs of bearishness are signaling us to take profits and after some time stock resumes the upward journey. How can we tackle this scenario ?

I wanted to share a real-time example #Vinati Organics, I was holding the stock from Rs 1000 levels and sold at 1900 levels, the logic for selling was simple. The stock had run-up quite and it broke the recent swing high (DOW Theory), but it resumed its journey again.

So either one needs to take a bit more risk of loosing on profits and follow some strategy looking at the weekly charts instead of daily, since the fundamental research is done and the share-holder believes in the long term story of the stock or use something like 200Day moving average and wait for the stock to stay below 200DMA for a week or so and then take an exit or something which you follows or advice us to follow.

Attaching the chart for your reference. Also it was a pure luck I got in the stock at such levels.

Disc:- Don’t hold this stock anymore, looking to re-enter if given an opportunity.

2 Likes

@hitesh2710 sir, Just an hind sight view from a lame man. If HDFC AMC seems expensive in terms of valuation, is it not advisable to invest in HDFC where not only there seems to be valuation comfort but at the same time we may become partial owners of HDFC AMC as well through stake.

1 Like

@hitesh2710 Hi Hiteshbhai,

1 Last couple of years have seen great growth in Nestle which is not seen in FMCG generally

They have changed strategy from pricing and profitability led growth to volume led growth and divided countrywide sales regions into clusters to focus individually on . Lots of new products are introduced and there was a talk of 3 dozen products being introduced some time back . Another thing that i observed is that their product is priced costlier than Britannia moo milkshake (Brittania at 25 rs and Nestle hazelnut coffee tetrapack at 35 rs still seems to be in demand so it shows that volume led growth is also with pricing power and the company doesnt resort to aggressive price cuts which seems a good thing despite focus on volume )

Is this level of growth that has happened in past couple of years a one off (due to lower base on account of Maggi issue ) or is it sustainable ?

2 What’s the reason that Trent has such high pe ratio like dmart inspite of much lower growth and lower ROCE ?

Many Thanks in advance, Hitesh bhai

2 Likes

When one has bought a company based on fundamentals, it makes sense to stick around with it as long as the fundamental thesis continues to play out. But if one is using technicals as an add on tool, I think one can reduce the position on signs of weakness rather than having a complete exit. Its easier said than done because sticking to technicals too stringently would cause premature selling in a lot of cases. Hence one has to be judicious in using technicals to handle long term positions in the PF.

And besides this, one has to have the discipline to re enter the position if charts start showing strength again even if the stock price has gone up after selling out.

Coming specifically to vinati organics, it seems management has been trying to reduce investors expectations and still stock price kept going up. It looks like a case where investors are more bullish than management. ![]()

21 Likes

Buying HDFC Ltd in the hope of owning part of HDFC AMC wont make too much sense as the holding of HDFC in HDFC AMC will suffer from holding company discount and besides that one needs to figure out how much it holds and how much difference to the overall valuations of HDFC does the stake in HDFC AMC make. HDFC Itself is a pretty big business and it holds a lot of subsidiaries in its fold. The valuations of all these subsidiaries will contribute partially to the SOTP valuations of HDFC, but the overall value of HDFC will come from the core business.

6 Likes

For nestle the main investing argument is the longevity of its business. And during the journey it will have periods of comparatively faster growth for some time and mediocre growth for some more time. Its difficult to predict how long this faster growth phase is going to last. Sometimes one can make some guesses from the annual report articulation or some other form of management articulation like concalls, agm talks etc. I personally think the faster growth phase could last some more time. It can keep on introducing newer products and/or brand extensions of existing products.

The kind of valuations Trent commands is something which beats me. Esp if one compares it to dmart. But of late since past few quarters, there has been steady growth in trent numbers. I recently visited a trent store in my city and found a lot of private labels from the company itself at fairly competitive prices and of good quality. So maybe the company has something going for it and seems to be on a strong wicket. Need to monitor the numbers more closely to see how the growth continues.

8 Likes

Hitesh Sir,

One query bothers me which you may find silly - I am asking with example of HDFC.

HDFC has got many subsidiaries and they are contributing well to the parent co. as long as they are subsidiaries of parent. In turn, shareholders of parent get benefited due to higher dividends and appreciated stock price.

But how the shareholders of parent co. (HDFC) get benefited when the parent comes out with IPO of these subsidiaries ?? (As has been done by HDFC for its subsidiaries HDFC AMC and HDFC life recently). Of course, the IPO proceeds straight away goes to Parent’s kitty but is there any other benefit which parent’s shareholders are likely to get ?? Pl. clarify.

I would also like to know your opinion about taking exposure in AB Capital and L&T Finance Holdings - The 2 beaten down stocks with reputed pedigree from highly beaten down sector ??

Ramesh Patel

3 Likes

Just to continue with the example of HDFC on how listing of the subsidiaries benefit the parent. First of all as you mentioned, diluting the stake through IPO provides money straighaway to the parent. This money could be used in many ways but for financial institutions where money is the main raw material, it means a lot.

Secondly, as long as the listing of subsidiaries has not happened, the market determined value of the subsidiary is not ascertained. Once listing happens, price discovery on the bourses takes place and an approximate value can be ascribed to the holding value in the subsidiary. One can also go further and calculate the sum of the parts valuation by applying valuations to the core business and valuations of subsidiaries (after applying appropriate holding company discount).

Another optionality for listed subsidiaries is (not relevant to hdfc as I dont see this happening) that if the management feels it appropriate it can sell off the subsidiary and realise some value out of it. Especially if the subsidiary doesn’t fit into the long term vision of the parent company.

Regarding the NBFC sector, I have always maintained that once the story is over for a particular sector it takes a long long time to make a comeback. There will be few exceptions to this but the base rate for finding big winners in such sectors which have recently lost market fancy is low. If one buys at a huge discount, there might be some money to be made but making multibaggers out of such situations is difficult. Cheap stocks keep getting cheaper.

The usual investor psychology in sectors which have lost market fancy is to find out stocks which have not participated in the sectoral bull run or stocks which on conventional valuation parameters appear very cheap due to excessive correction and try to ride them. The only problem with this is that the sector keeps getting plagued by a slew of negative newsflow and sectoral headwinds and after brief rallies these stocks keep giving up more than they gain. AB Cap and LTFH may appear cheap on conventional P/B or P/E basis but we are not too sure when the sector is going to regain market fancy and hence better avoided. Or else if we buy it extremely cheap we have to have an exit plan ready.

Just to recap,

Real estate and Infra stocks took a pounding in 2008-09 after having created a lot of wealth due to market fancy (and some strong sectoral tailwinds). Post the correction at every fall stocks like ivrcl, jp associates, suzlon etc have appeared very lucrative at some point of time but look where they are now.

Pharma stocks had a strong run up from 2011-15 or even 2016 in some stocks but post that most of them started correcting and kept going down. Even market leaders like sun pharma and lupin labs are currently at a third of their respective tops. Not to mention the second and third rung stocks. And all along the way down these appeared cheap if compared to valuations at the peak.

What we need to know is that the (hypothetical ) valuations accorded by markets to these companies at peak consist almost 50% or more of froth and rest due to real business valuations. (just an example about valuations at peak) If we use these as benchmark to compare valuations when stocks have corrected post achieving the peak, these will obviously appear cheap but can still become cheaper because the business environment keeps getting tougher and earlier growth trajectories are hard to achieve. Peak margins and growth rates are difficult to regain and after a long long time of correction/sideways movements, some sort of equilibrium in the business is achieved. This equilibrium often is achieved after the sector goes through catharsis where a lot of companies suffer large doses of pain and defaults/closures/bankrupticies etc. This process takes a few years to many years. In the meanwhile new sector/sectors emerge as market favourites and these start creating wealth. We need to focus on these to make decent money.

77 Likes

Hitesh Sir,

Thanks a lot for very prompt & elaborate response.

Not only it has clear many doubts of mine but I am sure it has helped many fellow boarders of the forum !

Hats off to your knowledge, clarity of thoughts and last but not the least your writing skills !!

Regards,

Ramesh patel

1 Like