What is the advantage of creating such content company? Is company planning to sell it’s content to other media companies? If so why they can’t keep it separate for Hindi and English?

I too had similar concerns over 60 crore transfer fee and the only rationale given that valuations are done by one of big 4.Raises doubts when company is sitting on so much cash and not doing anything .disc :invested at 270

We expect sentiment to improve on the back of a good monsoon and implementation of the Seventh Pay Commission recommendations.This will drive advertising revenue growth in the second half of the year.

Hi, can someone elaborate on the 13 crore expenses related to digital business for the quarter ended 30 june 2016? Is this the expense which will be transferred to HT digital media (new company when it is formed)?

This items appears in the notes of the quarterly results

Hi,

Been noticing that Patanjali & Baba Ramdev are advertising big time on Fever104 FM , could be a huge revenue stream going forward with the kind of sales Patanjali is clocking.

HMVL trades at P/E 10 and since last 3 years company has compounded profit at approximately 30%. ROE is decent at 20%. I think the market is taking this as granted. When should we expect market to notice this moderate growth stock with cheap valuation?

What if the growth falls before market realize the potential?

Does anyone have any insight into the breakup or trend of the income generated from the digital medium?

The company results presentation doesnt provide this breakup. The only mention for digital medium is that it operates a website called www.livehindustan.com.

Comission to distribution : Same for every company

Govt., fmcg , auto did well. BFSI, e-commerce and entertainment didnot do well. education was flat.

Gross Debt : 119 crore

Why no increase in dividend : No dividend as exploring M&A discussion but somehow it did not materialize

Can not tell anything on large dividend in case there is no acquisition in plan

Expecting good business in second half of year : UP elections/festive season;

In UP , more margin expansion expected. Currently at good double digit margin. good margins at 35% in stable state

Entering in new geography not happening this quarter and can not confirm future, so, that use of cash is also not sure

Growth is circulation based as due to competition, realizations are flat

Cover price reduction in Bihar, not in Patna but in areas where DB is entering

Avg. daily circulation : 2.8 m daily

In UP, ad yield ~55-60% of the market leadeR, may go to 75-80% of the market leader

Cash on books is Rs660 and total investments : 740 crore . Borrowing is 190 crore. Get cheaper money for working capital as cost of borrowing money is lesser than return on cash in various instruments

Rs 20-25 (corrected from earlier mentioned Rs 200-225 core, Thanks @Surender for highlighting) crore maintenance capex

Other income should be maintained at 20 crores

Board is aware of cash hoding and if nothiinghappens in next few quarter but can not say when but board is aware and will take call

HT media and HMVL will be holding digital company and details have been discussed in previous conference calls.

app launched on both ios and android and revenues flowing in

Does anyone know that in the proposed digital legal entity, what would be holding of HMVL and other details. In which quarter concall, this was discussed?

Disc: Invested with 2.5% allocation to portfolio. This is not a recommendation by any means

Thanks Surender for highlighting the mistake. Looks like while noting the nos on excel, i did some goof-up and did not realize while typing. Yes, maintenance capex cant be so high and considering the nos are matching with motilal oswal update by reducing one zero, should be Rs 20-25 crore. Due to office work, I do not get time to attend AGM/investor conference and try to go through researchbyte/company web site concall transcript and try to note down key information. By the way any idea if management has earlier given details of new company holding structure?

Appreciate for your efforts. Typos do creep in. Highlighted the Typo for the benefit of us all as I was going through report/concall.

Regarding new company, I never cared much about it as that was not the key thesis to be interested in HMVL. Thanks for probing and here is what I gathered from Q2 and Q4 FY16 Concall -

HT Digital Information: A content company valued at around 170 Cr, Houses the digital assets of HMVL and HT Media. HMVL holds around 43% and rest 57% by HT Media. HMVL’s Digital assets - valued at 70 Cr - were transferred to HT Digital Information whereas HT Media clubbed it’s digital assets HindustanTimes.com, livemint.com, and livehindustan.com.

Purpose of doing so : Create a centre of excellence to focus on digital content businesses, promote best practices sharing among these businesses & get some synergies.

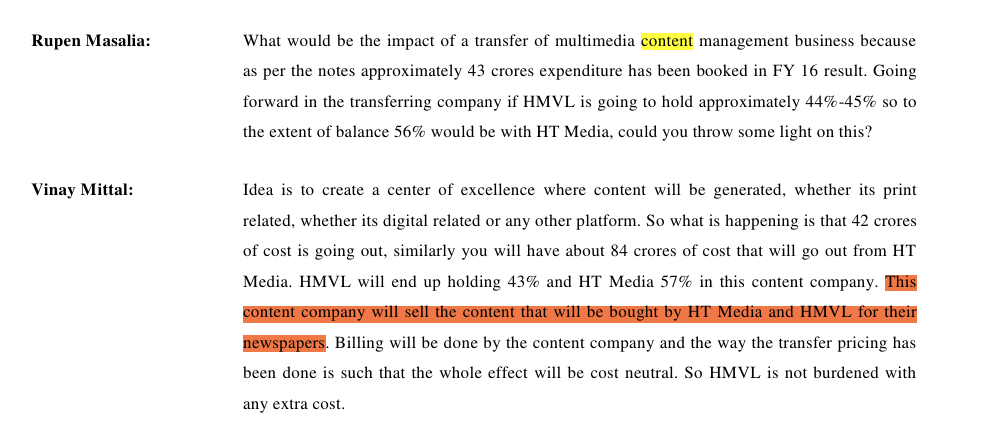

Impact on HMVL: Should be cost neutral. Certain costs will move from HMVL to digital entity (HMVL - realized loss of 20 Cr for half year - due to digital business) along with certain revenue which is currently negligible. HMVL will buy content/services from the new entity by making payments.This content company will sell the content that will be bought by HT Media and HMVL for their newspapers. Billing will be done by the content company and the way the transfer pricing has been done is such that the whole effect will be cost neutral. So HMVL is not burdened with any extra cost. It can sell content to third-parties apart from HMVL and HTML.

In my opinion impact on HMVL should be positive than being cost neutral. The arguments being

Depreciation of digital media assets will be absorbed by HT Digital

Synergies of operation

Ability to expand HT Digital business

Once this business grows substantially, this entity could be spun off to realise better valuations.

Although HMVL has a good management team, it suffers from oligarchy. The promoters seem to be more focused on family ties to business rather than looking at from an investment perspective to ensure as to how one can grow capital.

The best example of capital deployment is that of Mr Ajay Piramal who sold the pharma business to Abbott at a very good price and later deployed the acquired capital into numerous businesses. Every transaction since the sale to Abbott has contributed an average of 25% returns to the group. Piramal Enterprises still continues significant business in pharma and at the same time ventures into other businesses that have made money to all shareholders.

For a small time investor, the key to success is finding managements who are astute in deploying capital and have integrity.

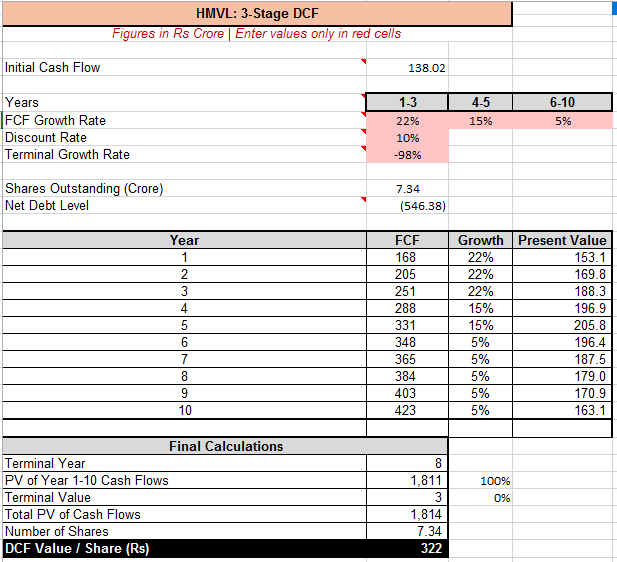

As I have been rebuilding my portfolio, I had picked 40-50 stocks and taken some minimum position to have further motivation to study them. Now, I am doing a methodological performance evaluation and also some basic DCF/Similar level valuation to get a sense of price. Tried to do the same or HMVL. As I highly doubt business longivity of print newspaper business, allocated almost 0 value to terminal value post 10 years and tried to build a very conservative estimate (assuming management would be honst enough on wahtever value business will generate). Here are the numbers. In worst case scenario too, I am getting a value of 322 which is approx. 20% higher than current price. Would like to know that how all of you cover valuation part? Anythin different required to be done. I understand as per valuepickr, it should be a screaming buy but many of us depend on monthly salary for investment as SIP and we do not get attractuve valuations everytime,so, some , sense of valuation while buying is important. Seeking comments to improve valuation model for HMVL.

I second your opinion that impact might be +ve. Here are the excerpts from 2015-2016 AR related to Digital business (copied as is from AR) -

A rapid increase in the number of mobile users, and improved digital infrastructure has encouraged a shift towards mobile and video advertising. This is expected to support digital advertising to grow at a CAGR of 33.5%.By 2020, digital advertising would potentially be worth 255 billion and is expected to contribute 25.7% of the total advertising revenues of the M&E sector

SCHEME OF ARRANGEMENT With a view to create a separate entity focused on the emerging opportunities in the digital media space, your Directors had approved a Scheme of Arrangement u/s391-394 of the Companies Act, 1956 between the Company and HT Digital Streams Limited, a wholly-owned subsidiary of HT Media Limited (holding company), for transfer and vesting of the Multi-media Content Management Undertaking of the Company to and in HT Digital Streams Limited.

P.S - As far as I could see, AR does not mention anything on usage of cash or revision of Dividend policy…Wait continues to see something on this front.