currently i am 21 years old, studying in a college, depends on my pocketmoney.

so how could i invest.

wait for few years and my disclosures will change.

3 Likes

Chrys Capital - a highly reputed PE fund has made an investment in Hindustan Media, bought 2.1% stake from the secondary market…

Exclusive: ChrysCap invests in newspaper publisher Hindustan

Read more at:

Disclosure : Not invested

2 Likes

Good results.

Sales 223Cr vs 194Cr YOY

Net profit 45Cr vs 31 Cr

EPS 6.14 VS 4.29

Cash stands at 39Cr

Point to be noted is short term borrowings increased from 98Cr to

128Cr in last 6 months. Why do company require to borrow when they have

so much cash and investments in funds?

Cash is not 39 Crores. Cash is around 630 Crores- you also have to include investments

1 Like

HMVL came out with very good set of numbers. Here is the link

Revenue increased by 13% while net profit up by 43%. Operating margins expanded significantly by 4.7% (24.2% to 28.9%) YoY.

Following are key points from the concall

-

Ad growth at 18.2% while circulation revenue up by 7.6%. Ad revenue growth is more on like to like basis when one considers that some part of festival season was in Q2 (Navratri and Dashera).

-

Most of the advertising growth was on account of volume and marginally contributed through yield. Thus 75% of ad revenue growth came from volume increase while 25% due to yield imporvement.

-

The leader in UP market, last quarter, had offered deep discounting in ad rates for bulk volumes. However, HMVL has not resorted to any discounting. However, it has not been able to improve ad yield as desired due to discounts offered by the market leader. However, company will continue to look for yield improvement going forward

-

Ad growth has been very good across sectors except for real estate and education which remain subdued.

-

In terms of geographical distribution of ad growth- Bihar experienced exceptional growth - 25%+, UP/UT grown by 20%+, In Jharkhand the growth was moderate while in Delhi it was tepid.

-

The political advertising impact in Bihar is very marginal in Q2. However company benefited due to pre election DAVP spending in July/August however it was partially offset by the code of conduct in September and hence reduced activity in tendering/DAVP.

-

There is no visible impact of rural slow down seen by the company.

-

There was very high growth in e-commerce sector advertising, however overall contribution remains low. It currently stands at 1% of the overall ad revenue

-

Amalgmation of HMVL’s digital assets in a separate company- To focus on digital business at group level and bring in greater focus. HMVL will transfer livehindustan.com to the new company. It is valued at around 70 Crore. HMVL will have 44% stake in new SPV formed. The new SPV will have assets from HT Media as well namely ht.com and livemint,com

-

Losses from transfer of assets and amalgamation will not be more than that at HMVL level. The process of valuation is done by investment bankers as required.

-

Company did some very good activation business in UP/UT. Hindustan leadership conclave was one such activation event. It was a hue success in terms of visibility and establishing thought leadership. In its first year it more than break even.

-

Local: national ratio has improved. It was 45:55 and it is now moving towards 50:50. Traction in local market was slightly higher than the national market.

-

In the current year, HMVL is not planning any expansion in other market.

-

Difference in ad rates in UP is 35% between market leader and HMVL which used to be 45% last year. The difference between the Amar Ujala and HMVL is now 15% which used to be 25%. Company expects to close the gap between Amar Ujala and itself by end of this year (suggesting 15% increase in ad rates)

-

Company in the last two years have consistently taken away market share from both Amar Ujala and market leader Dainik Jagran. Even in this year, HMVL continues to take away market share from Amar Ujala in all the months and have taken away market share from Dainik Jagaran in most of the months

-

Company has launched both android and iOS app fro the Hindustan

-

Q2/Q3 for Bihar this years may be exceptional due to pre election spend and election. The underlying volume growth in Bihar is expected to be 8-10% while in UP/UT it is higher by couple of percentage points (10-12%). This will be supplemented by yiled improvement.

-

Company is confident of delivering robust growth in the next two quarters as well.

Overall, the momentum in business performance continue to be excellent (especially when seen in the context of peers , i.e.DB delivered de growth in ad revenue and degrowth in bottom line as well) while the utilization of cash still remain uncertain.

Disclosure: A significant portion of my portfolio and continue to hold from much lower levels of 102-105

6 Likes

Hi dhwanil,

Any idea why increase in debt despite having lots of cash?

Hi Sunil,

As per the management commentary, the debt is for funding the working capital needs of the company. As they do not want to touch the long term investment that they have made in debt mutual funds, they are borrowing money to fund the same. Whether that is the the most optimal approach or not is debatable. However, personally I do not see that as much of material concern as the financing cost is quite less compared to overall profitability levels.

the approach seems wise as redeeming long term debt mf now have some tax implications

Stock at P/E of 12, with sales growth of 11%, Profit growth of 29% in last 3 years (and ROE 20%)

Investment in MF 550 cr = 3x net profit of FY15.

This looks a safe bate. I am planning to take a small position.

The good part is company is converting about 11% of cash available into other income which somewhat proves this money is for real unless they writeoff bad debts or losses in future.

Check this http://epaper.livehindustan.com/epaper/Delhi/Delhi/2015-10-31/1/Page-2.html

These days the front cover pages are filled with full page ads. With ecommerce companies spending huge in advertisement is good for the company. This will also force store retailers like Chroma, Vijay to increase their advertising spending to compete with online retailers. Coming few quarter should be good for HMVL.

Came across this article on Mint on ‘Why E-commerce companies prefer advertising in print media’ -

It’s an interesting read as it helps understand behavioral patterns of people reading newspapers and why advertisers prefer advertising in newspapers.

Disc: Invested

Disc - Invested & optimistic

This company has a superb balance sheet. It earns about 19% on invested capital. Its Investments ( current & non-current) + Cash total a whopping 587 crores. It has no long term debt. It is no 1 or 2 in the markets it operates in. All for a market cap of 2075 cr (25th Nov 15). On top of it it generated an OCF of 138 cr in March 15.

I think those who have bought it at lower levels are going to be very happy with their purchase.

1 Like

In my view strong brand names have always commanded good valuation, and this one is available for cheap. Another one I like in the media is TVTODAY but it seems a little overvalued at the moment for making an entry.

DISCL:Invested in HMVL sold my TVTODAY holdings recently.

And another party popper is ad difference between english and hindi daily is reducing

Hindistan Media Ventures Limited (HMVL) : A mis-spelt bet

(read the thread topic )

Disc : Invested with 5% of portfolio.

1 Like

One question that always pops up in one’s mind while investing in the newspaper business is how the digital and online space will make newspapers redundant.

Being an ardent reader and supporter of newspapers to me it just doesn’t seem possible. I think newspapers are here to stay and let me stick my neck out and say everywhere in the world (including the west).

Here is an interesting article that I read on Value Research on why newspapers are here to stay (from an India perspective). Good read and helps raise my conviction in being invested in this space / HMVL for a long time to come -

Disc: Invested

Thank you for all the input.

Dhwanil, your commentary has been invaluable. It has provided great insights into the business and the industry.

These are my thoughts…

In this industry once a newspaper has reached a significant scale, it begins to enjoy immense pricing power.

The newspaper creates a network effect that commands a premium from advertisers. Customer stickiness also allows the newspaper to increase cover prices.

Thus establishing a network effect in a large market is very powerful.However HML’s entry in UP, and DB’s entry in Bihar/Jharkhand point to the fact that an incumbent’s network effect can be encroached upon. Thus a players ability sustain a created network effect is extremely important.

Amar Ujala failed in this respect allowing HML to gain market share. While HML has also bled some market share with the entry of DB, it has been more resilient when compared to Amar Ujala. Yet readership has fallen. From 2012-2014, Bihar readership has fallen from 48 lakh to 43.8 lakh, and Jharkhand readership has fallen from 17 lakh to 13.8 lakh.

DB’s launch strategy (known as the Orbit-Shifting Innovation) has won a business process innovation award, and is case study at top B-schools. DB has basically been very successful in entering new markets in the past. You can read about it here: http://www.dainikbhaskargroup.com/pdf/Media-Center-Case-Studies/Making-Breakthrough-Innovation.pdf

What I find extremely puzzling is that DB has not yet made an endeavor to enter UP/UT. In recent times DB has entered Bihar and Jharkhand but the UP/UT market is bigger than the Bihar, Jharkand, and Delhi markets combined.

I would love to hear everyone’s thoughts on

- Why has DB not entered yet, am I missing something?

- What will happen to HML’s market share and growth prospects if DB decides to enter now

A possible reason could be that perhaps DB was unsuccessful in penetrating the Bihar and Jharkhand market, and thus DB management is not confident about going head to head with HML again. If this is the reason, then I think it very strongly reinforces the strength of HML’s moat. This is just a possible reason. I have only recently started to study this industry, I’m far from an expert. Hence feedback is welcome, and much needed.

If its true, the implications are very favorable. Due to correlation between readership and pricing power, as HML continues to increase its readership in UP/UT, FCF will grow incrementally. FCF has quadrupled in the last 5 years (29% CAGR), and that trend may continue.

I look forward to some feedback. Thanks guys.

Disc: Not invested but looking to make a position

5 Likes

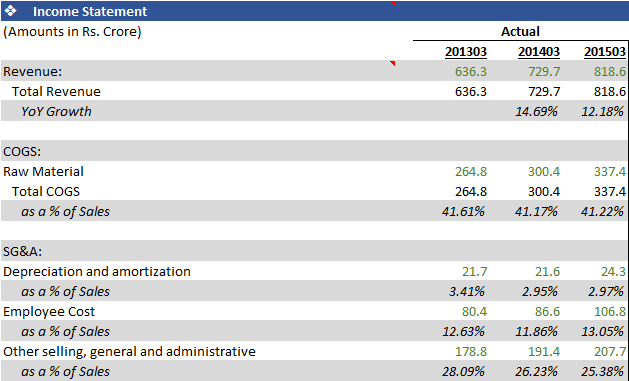

After doing some more research I would like to add the expansion in margins has been account of both pricing power (which flows to the bottom line) and their fixed cots being spread over a larger volume. The second factor illustrates the operating leverage that the business enjoys.

As you can see from the table below, raw material cost as a % of sales has declined marginally. But SG&A (advertising, repairs, rent, etc.) and depreciation have declined as well. Infact they have declined more significantly.

I would also like to add that DB does actually have a presence in Uttarkhand. They still don’t have a presence in UP however, which I still find very puzzling.

As an outsider, it is very difficult to make guesses as to why DB gave a pass to UP market. However, we may look at the decisions along with industry dynamics/characteristics and their company’s own peculiar circumstances

-

DB Corp from 2003 onwards have launched it’s edition in Gujarat, Rajasthan, Punjab, Jharkhand, Maharashtra and Bihar. If we carefully look at it in most of the markets ( except Bihar) they have chosen where the competition is prima-facie local or regional. Be it Gujarat Samachar in Gujarat, Rajasthan Partika in Rajasthan, Punjab Kesari in Punjab, Lokmat in Maharashtra or hindustan/Prabhat Khabar in Jharkahnd. They have refrained from or have not agressively entered the markets where much larger players such as Dainik Jagran is leading the market. It may be a coincidence or a calibrated strategy

-

Another interesting thing is that DB Corp has first focused on markets that are relatively well urbanized (Gujarat/Maharashtra/Punjab/Rajasthan) and have higher prosperity and hence are large ad markets. This is a very smart strategy. In fact, DB Corp always position itself as first choice of urban readers/ SECA/SEC B category of readers.

-

Now considering this strategy to focus on more urbanized markets and the typical break even time of 5 years for a news paper business, DB corp had hardly any room to look at any other market till 2010/11.

-

However, after capitalizing on the Urban market, it has in last 4 years started to focus on more Rurban/rural focused markets like Jharkhand/Bihar. However, by 2010/11, HMVL had entered UP/UT markets and hence they may have decided against entering that market as typically it is difficult to sustain more than 3 players in a market and new entrants always face tough time.

-

Only lately, in last 5-7 years, advertisers have woken up to the aspiring market of rural/rurban area and increasing their ad spend. While this happened, DB Corp, due to its strategic priority may have missed the UP market.

Again, this is nothing more than best guess and as I said earlier, it is very difficult to pin point exact reason for not entering UP earlier.

- On your question of entry of DB in UP: I feel it may not happen for 3-4 years at least. Reason is simple. Their Maharashtra business has only recently come out of investment mode while Bihar business will bleed for 2-3 more years. Also, the will first want to consolidate their position in Bihar. Frankly, Jharkhand would have been the most disappointing entry for DB as they haven’t been able to make much headway there. So, logically, they may want to wait and watch how they are able to fare in Bihar to gauge whether their entry in rural/rurban market can be as successfull as it has been in urban markets.

In 3-4 years, at the pace at which HMVL is moving, it will consolidate it’s position in UP well and entry of DB Corp may have less pronounced impact.

Again, all this is intelligent guesses and logical reasoning and reality may pan out very differently than what we anticipate.

Hope this helps

4 Likes

Here is a research report from firstcall which recommends a buy at CMP http://www.moneycontrol.com/mccode/news/article/article_pdf.php?autono=4464701&num=0