The promoters do siphon the money. Just check the related party transactions. They are giving loans to other group company of the promoter. There are other doubtful assets on the balance sheet. The salary of the top management is also increasing without increase in profits.

I entered the stock one year back. Made some 30% gain and exited. I was an inexperienced investor back then. Otherwise I wouldn’t invest in such companies.

Disclosure: Not a buy and sell recommandation.

The Q2 numbers are out. Yoy, operational revenues have grown from Rs. 163.3 cr to Rs. 175.6 r. Previous quarter, operational revenues were at Rs. 168 cr. So growth is picking up marginally.

Net loss is at Rs. 30.7 cr compared to net loss of 21 cr last quarter and net profit of 32 cr last year.

Optically, the net loss looks really bad but it has to be looked at in the proper context. They are presumably burning 31 cr this quarter (As reported under Segment reporting) in funding startups under HT Labs. Finally, the promoters have found a way to utilise the huge pile of cash that the company owns. Some of the startups under HT labs are OTT play, Slurrp, Mint Genie, Upublish and HT Schools. These are the well known ones and as per Avinash Mudaliar the head of HT labs, there are more on the pipeline. We may agree or disagree on whether this is the right usage of cash reserves but I think it’s a step in the right direction.

Former Pepsi India head Praveen Someshwar is heading the company so I trust him to lead the company towards being digital and future ready.

The legacy print business has shown marginal improvement. Segment loss has come down to 8 cr compared to 14 cr in previous quarter. The loss is mainly attributed to the rise in newsprint costs.

Current market cap stands at around 380 Cr and latest book value stands at close to 1500 cr. Most of the book value is made up of mutual fund investments in debt instruments. It is baffling to say the least why such a cash rich company is being priced for bankruptcy. It just shows negative sentiment regarding the stock is overwhelming. Many investors looked at the cash reserves in the previous cycle and burned their fingers as the stock price consistently declined from 250 to 50.

Most institutional investors have fled the company. The question is whether the worst has been priced in or is there more pain to go?

Disclaimer: After studying the company, I feel that the stock has been hammered down too much. So its one of the largest holding in my pf at an average of 65. Let’s see what the future holds for HMVL. Interesting times are ahead for sure.

I agree corporate governance standards have been poor. Especially with regards to excess cash reserves which ideally should have been distributed to shareholders. So far, they have not addressed the interests of minority shareholders convincingly.

These are legitimate concerns but are these concerns overblown? Is it rational to discount cash to such an extent. After all, cash is money in the bank.

They also have investments in tech companies like Mobikwik, Oyo and Snapdeal among other startups. Management has stated that they are not long term holders and they will sell out during liquidity events. They have invested 81 Cr in Mobikwik, 44 Cr in Oyo and 31 Cr in Snapdeal which totals upto 156 Cr. As per FY 22 balance sheet, the company has financial investments worth Rs. 1514 Cr.

So the question is does questionable corporate governance standards warrant such a huge discount on financial assets? Book value mostly consists of liquid investments amounting to 1,500 cr but it’s market cap is less than 380 Cr. Is there any merit to such a steep discount? What am I missing??

The Cash available with the Company is a known fact for all of us and there are smarter people in the market who are ignoring this fact. FII and DII have reduced there stake…I presume that there are many things which I may not be aware of but market is and for that reason the stock is available at discount.

They are siphoning off the money in terms of intercorporate debts very high top mgmt salary. On the top of that they don’t give any dividend also. so it’s about doubt that is the cash on balance sheet is really true.

Disclosure: Invested 1.5 yr back and sold after 5-6 months.

Siphoning off of funds is a serious claim. Can you share any link or publicly available information which throws more light on this. As far as Management salary goes, Praveen Someshwar the Md is being paid a salary of close to 7 Cr per annum. For someone who was previously Head of Pepsi Asia Pacific region this kind of salary is in the right ballpark.

With the pile of cash that HMVL has they are foraying into new age tech businesses. The company cannot afford to pay peanuts to someone and fritter away the cash reserves. They need the right person for this strategy.

Your claim that the cash is non existent is difficult to believe. The books of accounts are audited by BSR and Co which is an associate firm of KPMG. So unless the auditors are in cahoots with promoters, we need not doubt the cash in the balance sheet. Anyhow, the credit rating agencies also check the books of accounts and HT media has AA rating for it’s long term debt.

It’s not that the management is blameless. But the criticism has to be valid and not unfounded.

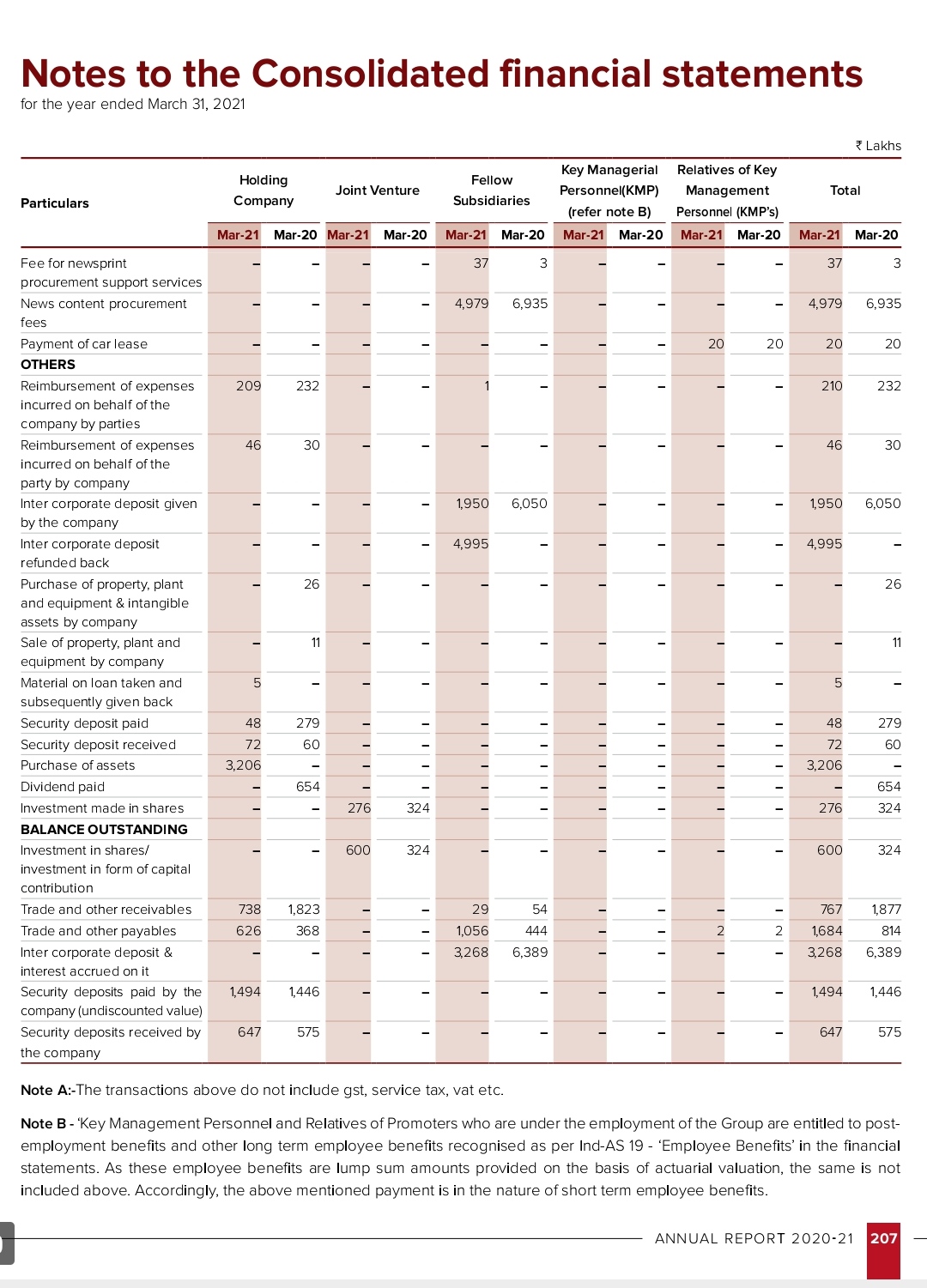

I did not find intercorporate deposit in HMVL Annual Report. I think you are referring to Ht Media’s 80 odd cr loan to Digicontent.

Firstly, shareholders of HMVL are not affected by HT Media’s loan to Digicontent.

Secondly, Digicontent has digital assets like Livemint.com, Livehindustan.com and hindustan times.com. They also have content sharing agreement with HMVL for which they charge close to 55 cr. Given this situation, they are in a reasonably sufficient position to service the debt of HT Media.

From my perspective, the management of HMVL have gone wrong in 4 areas.

They did not have a capital allocation framework for a long time. They allowed investors to get frustrated and lost their credibility in the process

Now that they are finally utilising their cash reserves, they have fallen short in disclosure norms. Most investors have no idea about HT labs and the startups contained there in. In Q2, the company made a net loss of 30 Cr and the burn rate in startups is presumably 31 Cr. Instead of me diving deep and figuring this out, they should have put it across in a better way rather than dumping it in unallocated expenses under Segment reporting.

Thirdly, they are bundling two different organisations under the same corporate structure. A hundred year old legacy vernacular printing firm is held under the same corporate structure as a bunch of new age tech startups.

In what way does this make any sense. They should consolidate HT labs under a wholly owned subsidiary so that its results are not combined with the newspaper business.

Finally, they have failed in articulating their change in Strategy. Essentially, they are following the Info Edge model wherein Naukri.com would be the cash cow which funds in-house startups like Jeevansathi and 99acres while also participating in growth stories like Zomato and Policybazaar through equity infusion. There is nothing inherently wrong with this strategy. The management should come up with a decent communication strategy and convey it to shareholders. They should leave it to the judgement of shareholders whether they believe in the vision and execution capabilities of the management. But non-communication is not a great idea.

In revenue terms, the HT Group is the second largest media conglomerate after the Times group. They have the brains, bandwidth and werewithal to manage the media resources. The fact that they have failed for so long in Investor Relations is appalling.

There is still time for them to recover and stage a turnaround. They need to instrospect on why the Investor community has lost faith in the group and come up with right solutions soon to salvage the situation.

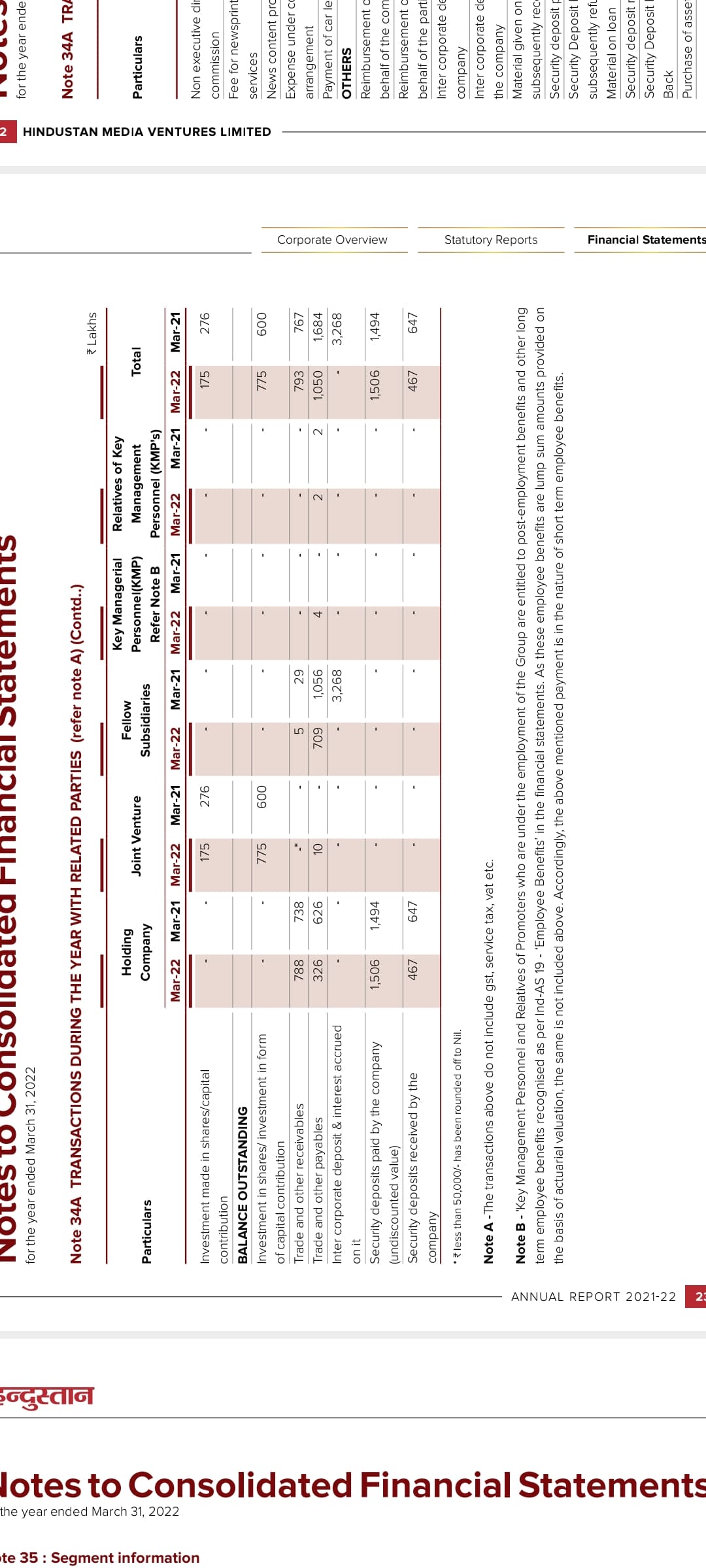

I invested back in 2020. Here take a look at the snapshot from annual report of fy21 and fy22. looks like the intercorporate deposit is repaid. But the money on their balance sheet is there for long time. Market doesn’t like idle money on balance sheet (source: the thoughtful Investor by basant maheswari). It’s evident from the low price to book value ratio market is giving it for long time.

Yes. There was a 30 Cr loan given to Next Radio Limited which is a fellow subsidiary. It has been repaid in full.

Another 16 cr inter corporate loan is given to HT Noida which is a subsidiary. It is quite common to provide loan to direct subsidiary and should not be construed as corporate misgovernance.

As can be seen, there is no evidence that HMVL is siphoning off money from accounts or anything of that sort. The overwhelming negative perception is mostly due to the price action. The bad news has been priced in but the optionality of positive triggers is being overlooked.

If and when there is a shift of sentiment, HMVL can get rerated significantly. It needs a catalyst or positive trigger to enforce that shift in perception.

The last remaining institutional investor Steinberg has sold its stake at Market price of 51. Mathew Cyriac connection, Mathew Elizabeth has purchased the Steinberg stake.

Fundamental Valuation for HMVL makes little sense, as it belongs to a dying industry. HMVL, with its flagship Hindi newspaper is still better placed than the English dailies, but the performance has been on the way down pre-covid and has got further exacerbated during and post-Covid. The main revenue earner for the newspapers is the Ad Rev, and this is moving away to digital space. Circulation is static and they have little to no pricing power.

There are a few positives that might play out in FY24 for HMVL; 1) Reduction in newsprint prices may reduce the cash burn (losses), 2) Improved ad spends by corporates in some sectors that target the rural landscape, 3) Uptick in GoI and State Govt. ad spends in view of the upcoming general and state elections, 4) Improvement in their new digital venture subscriptions, OTT Play.

However, HMVL is still an asset play with a large cache of Investments and Cash in its pockets; against a Market Cap of ~550 cr, HMVL’s Investments, Cash and Cash Eq. are worth 1400 cr as per AR FY23.

What is missing is the catalyst to spark market participant’s interest and unfortunately the sub-par transparency and communication skills of the management doesn’t help either. If and when it plays out, it might see some upward movement towards its Intrinsic Value. Note that the stock price has increased by 42% in the last year, but this could just be the result of the general exuberance in small and micro cap stocks in the market.