Interesting development.

Lets roll back to FY2106:

• HMVL Paid 60 Crore to HT Media to purchase Hindustan brand.

• HMVL pays royalty (amount of which cannot be disclosed publicly) to Parent company (HT Media).

• Effective Apr-2016, a new entity/content company named as HTDSL was formed and valued @ 175 Crore. Stated reasoning was that digital business needs focused attention in order to exploit the synergies of the groups digital business. HMVL stake of 43% was valued at 75 Crore. Newspaper Content would be bought by both HMVL and HT Media.

In FY17, HMVL paid 71 Cr. to HTDSL as News Content Sourcing Fees. Also, HMVL booked 41 crore losses in the P&L under Share of Profit/(loss) on Associate (HTDSL) losses. Per say conference call of Q2_FY2017, Content company breaks even at EBITDA level. Per say conference call of Q3_FY2017: Going forward, HMVL will be able to participate in the value creation journey of HTDSL.

Voila, Q2_FY2018……After saddling the losses of the business for 6 quarters, HMVL has sold the HTDSL ownership at valuation similar to the one assigned an year and half back. Also, disclosed the buying of an unrelated business (IESPL demerger into HMVL) stating it as “strategic fit”.

28 Sept 2017: CEO resigned.

16 Oct 2017: CFO resigned.

Bladder theory of finance is at work.Money always finds a way out. I think I have a case study at hand in order to read and understand the book “Financial Shenanigans”. Disc. (No holding as of now.) Prepared the note as a learning exercise. Whenever listing of HTDSL comes up, I would be keenly watching for the demanded valuation .

Where did you read about the listing? All I can see from the FY2018Q2 results is that HTDSL will be sold to the newly created subsidiary of HT Media, HT Digital Ventures.

With respect to financial shenanigans, I would be watching who subscribes to the Rs. 400CR debt issue of HT Media very closely.

When all this digital unit was being formed , I had sensed some hanky panky. I think I was little confused and had asked Hitesh Jee for his views on his page I think. Was not comfortable from the beginning with this set up. Anyway exited long back due to capital allocation issues but this is academically interesting now

@sambandham82 Latest value of net cash is 868Cr…As I mentioned in my earlier note, Cash is already going out . In future, I anticipate that more and more content will be bought by HMVL from HTDSL. Also, this unrelated B2C business might be one more way to mask the cash usage.

@RICHAJ…Listing, I just anticipated as I wrote WHENEVER, but Just heard the conference call (Q2FY18)…HTDSL would be auto-listed…HT Media share holders would get the shares but HMVL share holders are bought out.Now, the best part that I liked in the conf call was when management commented that shareholders of HMVL should be really happy as they got around 3.5Cr more than what they invested a year back…Also, HMVL will benefit from this as they are going to source the content from HTDSL besides the fact that digital strategy is quite risky and HMVL has been kept pristine by taking away that risk.

This was bound to happen as for years the cash pile was getting larger and larger and they didnt have any proper answers to it, from what i remember they first said they will wait till 600cr to pay out a higher dividend then cash piled till 1000cr and they didnt even pay any kind of dividend rather kept on accumulating cash. In HMVL’s case too much cash they holded was the only negative reason in my view for exiting the stock as It was almost evident they are not at all in mood to pay anything to the minority shareholders.

net result being promoters have managed to increase their stake in the company without spending a penny from their pocket in return for a completely worthless (personal opinion) and unrelated (by no means a ‘strategic fit’) business. very poor move.

Came across the following sentence today in William Thorndike’s excellent book ‘The Outsiders’: “Be wary of the adjective strategic – it is often corporate code for low returns”. And my mind went back to HMVL’s “strategic fit” !

HMVL has significant institutional shareholding and it is a tragedy that even they become mute spectators to such larceny. SEBI should test such actions against proposed regulations like the Uday Kotak Committee recommendations to assess their efficacy. Meanwhile, an important learning for investors from this is that just because a company holds quarterly analyst concalls, it should not be assumed to be investor friendly. Actions speak louder than words.

I have been tracking HMVL and HT Media for three years, liked HMVL more all the way. But never got confidence on usage of cash, and never bought. Got lucky, you can say !!..

The part that irks me the most is,that they kept saying they will pay dividend once cash pile crosses a threshold,but now the money is being used to buy content from a company,which was until a year back a part of HMVL.

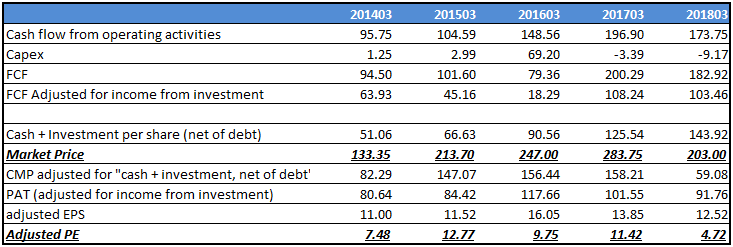

@Ravichand08… good idea to value business by modified PE…

at price of 250, you have calculated modified PE of 9.30… which it is trading at 4.72 now… lowest in 5 years… Very attractive bet at this point of time… check the Image below… trading at lowest adjusted PE…

As long as the accumulated cash is used the market wont value the stock , the cash with the company is huge and thats what the minority shareholders have to worry about.

Agreed, main point is deployment of cash… either they should use it for growth or should return to shareholders… but even after outside pressure about cash, looks like management is waiting for the right opportunity (which indicates that management choose to wait instead of buying something overpriced) … and at current, company is earning 8 to 9% on that investment without tax which is within acceptable limits… we can even value this investment as separate business and value using DCF method… cashflows at 8% for 5 years, 3% after that and cost of equity at 9.50% (HMVL has low cost of equity as it has low beta)… This will tell you that you are getting print media business for free…

at ~Rs.150 per share of cash and cash equivalent (+investments) & earning of 8 to 9% on that… this itself protects downside… Looking from qualitative perspective… management is good… there are very less chance that they will destroy wealth by improper deployment of cash.

Assuming the market cap (stock price) does not increase for next 2-3 yrs, the cash on book = market cap and whole business is available for free. Can such a scenario happen? or management will find a way to erode this cash?

I had a look at it 2 years back. Tracked 3 quarters of rant that we will see on cash which actually meant we do not know n then the digital subsidary set up n my sense was it was to divert some cash. Good time to do some analysis hoe cash on books has moved since then.

That is the concern by most of the investor community I guess…

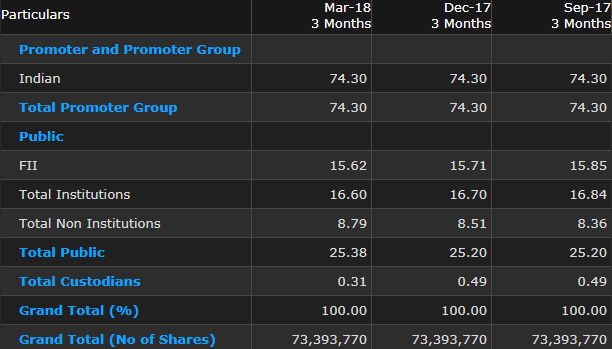

Management may erode this cash on books. But as much as management is concern, they have link to Birla group and Jubilant group… Great roots… and on quality of management, they score well…and if there would have been a real concern about the cash, management would have brought down the promoters holding… which has not happened… even Institutions has considerable amount of holding from the remaining shares… here is the holding from last three years…

(Source - Cogencis)

Public has the least holding…

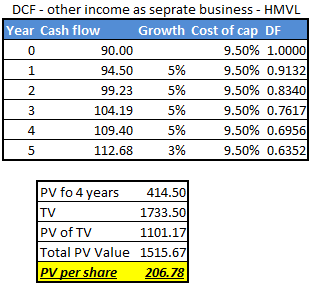

Apart from this… as I have said earlier… considering other income as a separate business we should do DCF separately …

find the DCF valuation below…It shows the present value of future cash flow from cash is 206 per share… CMP is 203… which tells us that we are getting print business for free…

My assumption is… management continues to earn return (post tax) on cash and investment of 5% for 4 years and 3% thereafter…

or

They deploy the cash in a business… where they earn return after tax of 5% CAGR for 4 years and 3% there after…

This assumptions are fair enough (Views welcome)

Now… Even if you consider 5% degrowth at terminal… you will get valuation of 145 for cash business… which still makes sense for HMVL…

Does anybody has anything to say through qualitative perspective of management?

I guess numbers are attractive and only quality perspective are to be checked…

Management kept the dividend constant in last few years even after sitting on huge cash pile… they are accumulating this cash and then investing it in the market including debt fund and EQUITIES. They have even faced loss in 2018 in debt funds…

So my doubt is… are they more of an investor in the market than management of business…

What is happening from last 3 to 4 years is

they make profit in print business

bring down that earnings in to market in the form of investments which is huge now (almost 65-70% of market cap)

tell investor community that they are looking for the opportunity but fails to provide timeline for that…

Next year, repeat the process…

Hindustan Hindi news paper even failed to show good numbers compare to their own parent companies Hindustan Times English news paper… this may point that HMVL lacks somewhere…

So, are they shifting their focus from their core business?

It seems that it has going to use that surplus cash to give an Exit to B2C business of India Education Services Private Limited whose parent company is HT Media. Interesting article on the demerger transaction happening for HMVL.

In this falling market, Investor should approach the value investing instead of growth… I strongly feel HMVL is the best value investment opportunity in this market. Results were not good for HMVL for Q1FY19, but looking at the past records, it seems they will manage to post a moderate growth compare to Q1 on account of election in CY19.

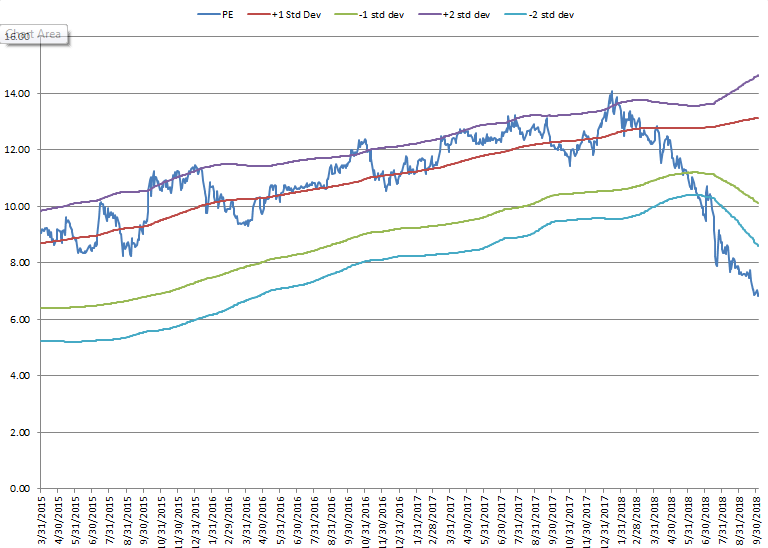

Currently, I found a very interesting thing, I have plotted the 1 year forward P/E chart and it is trading below 2 standard deviation… to plot the 1 year forward P/E I have forecasted FY19 P/E at Rs.18.00 against 23.33 in FY18…

.

.