PY III oilfield (21 % HOEC Stake) will begin its production by the end of year , lets see when it fructifies

nos out. good nos

1 Like

[HOEC Q4 FY23presentation.pdf|attachment] Updated Earning Presentation (upload://pORcZlYsYgqhC2IxguiiBfid3xo.pdf) (1.8 MB)

HOEC Q4 FY23presentation.pdf (1.8 MB)

2 Likes

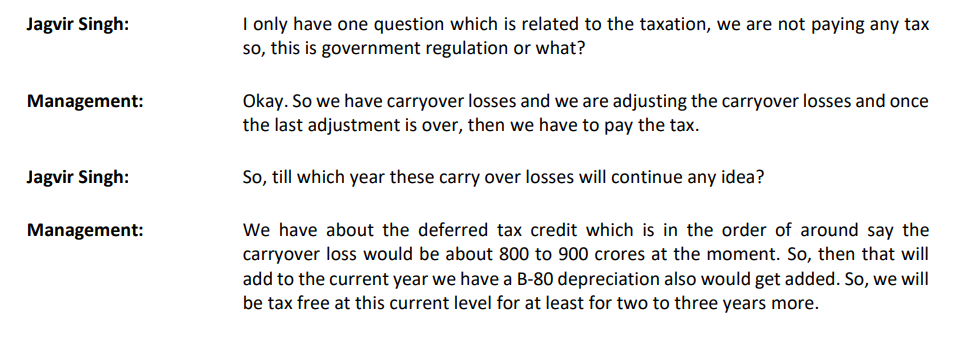

Loss carry forward is completed ( as loss recognition happended in 2015 )? if yes, all PAT will be taxable from coming quater…

1 Like

5 Likes

Good to hear that as a share holder… Thanks

Thinking, how it is possible as 8 yrears completed ?

There is a difference between the way Profit/Loss is calculated in the books of accounts and Income Tax return, of a business assessee. Just one example is: a company may charge depreciation in its books as per straight line method (SLM) or written down value (WDV) method. Under Income Tax Act, only WDV is recognized.

1 Like

What could be reason for such negative reaction today ( almost LC with 20% down)

Elango retirement / B-80 preventive maintanance or any other issue ?

Elango retirement and Q1 results below expectations may be the reasons. I am also taken aback by Elango’s retirement. Guess we’ll have to wait till Friday to find out more details.

1 Like

Elango resigning after 8+ years with the company is a big negative since its professionally managed. However Jeeva is still at the helm and has similar experience in both Oil & Gas as well as HOEC and is a technical person as well. But Jeeva is older than Elango so market sees this as a big negative perhaps.

IMO, Elango retiring post bringing online B80 is a respectable finish to his career and I always believe in ending on a high, so wouldn’t wish anything else to others. Since the wells are now running and even the pending hose repairs appear to have been completed, this shouldn’t affect the long-term value of the company.

The numbers being below par should get clarified in the call. Going by Note #3, offtake was lower from Dirok due to maintenance at customer’s end. Value of an oil-field is done based on long-term projection like 10 or 15 yrs and numbers of a single-quarter means nothing, unless there is some serious technical issue affecting long-term value, which I doubt could be the case here.

I could be wrong

Disc: Invested, no recent transactions

17 Likes

I also believe that the selling could have been by HDFC. As far as I know by regulation HDFC can’t hold any shares of another company post the merger. In the last quarter HDFC sold some shares which may have intensified in this quarter.

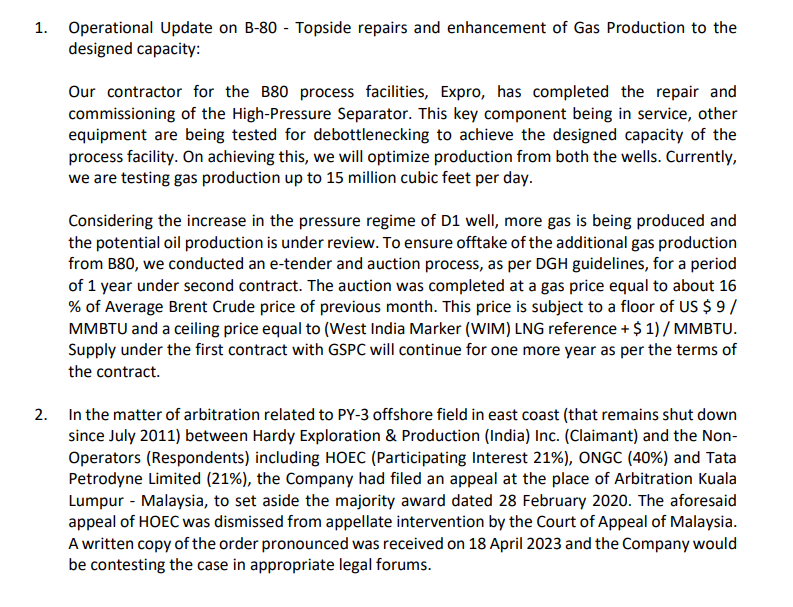

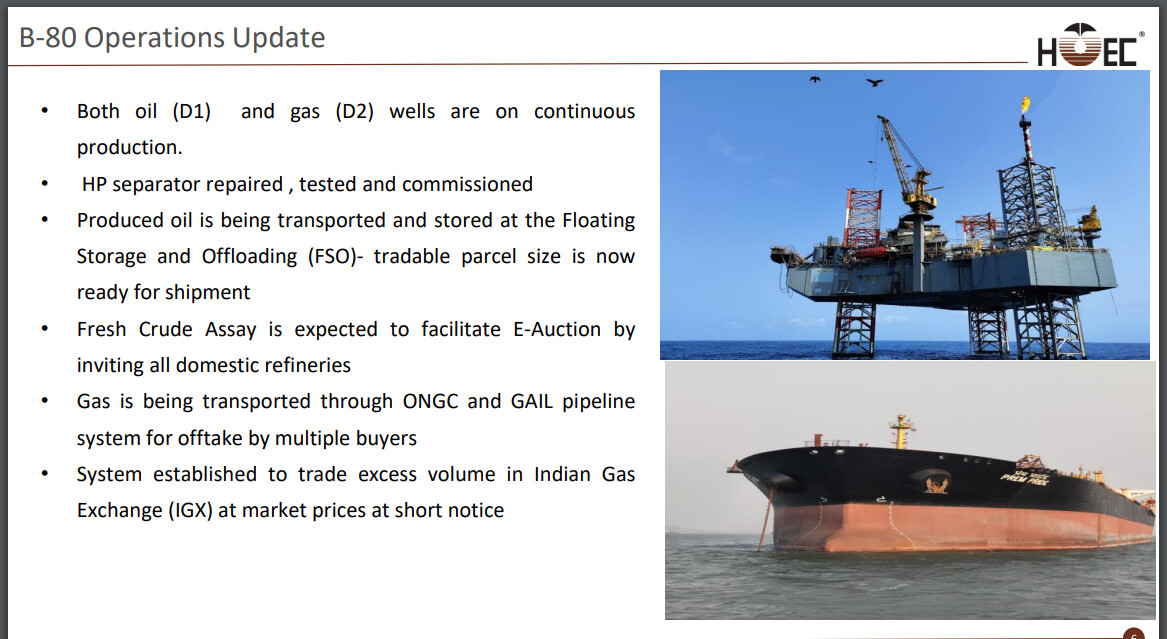

B80 shut from 2nd july to 15th august

Revenues should be lower than last 2 quarters and so should PAT. The volatility in earnings makes it unlikely candidate for rerating in my opinion.

3 Likes