Adding to the discussion:

I feel this company is promising because this is a Zero Debt company.

Their profit Margin is High :

The price realized is government mandated $2.48 per million British thermal unit. The production cost is usually ~60 cents per million British thermal units.

(Source http://www.4-traders.com/HINDUSTAN-OIL-EXPLORATION-9060045/news/Hindustan-Oil-Exploration-gas-drill-25034559/)

The commodity Price Of Natural Gas (futures) is on the rise as Per Investing.com

I also have a small question for the other Boarders:

There is Not much record for the alliance “HOEC Bardahl India Limited” , Did this fail ?

Disc: I have started investing in small numbers from 1st Nov.

current market price is 133 from just 33

Mr.Ajitji, Is it valuable price? at current level …

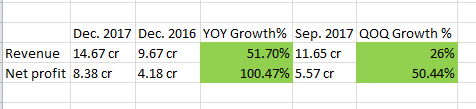

HOEC result on 20th Jan.

Great quarter. Looks like management is delivering on their promises.

Exclude the other income of 4cr in Q3Fy17. Revenue from opeartions looks very impressive with 13.3cr in q3fy18 v/s 5.4cr which indicates significant increase in revenue from Assam block as guided by management during concalls.

The outlook from management is quite positive for next FY. With oil prices expected to remain in the range of £60 - 75, Is stock a reasonable bet at the prices of Rs. 121. Views invited.

I think it’s a great bet. My investment thesis:

- Strong management: They are experienced and are delivering in the given time frames.

- As per the below article, they are expecting 100 crore profit by March, 2019. This translates to an EPS of 7.3

- 150 crore cash. They want to use it and are open for inorganic opportunities as well. If it happens it will increase the earnings further.

- Though oil companies are not valued at P/E basis but irrespective of the valuation method it seems there is a lot of potential in the stock.

https://www.bloombergquint.com/markets/2018/01/22/hindustan-oil-exploration-bets-on-higher-output-to-boost-growth

HOEC’s field development plan for Mumbai B-80 region got approval.

"We aim to start production during the April– June, 2020. Production from B80 is expected to add ₹100 crore per year to the bottom line of HOEC,” P Elango, Chief Executive Officer, HOEC, told BusinessLine.

Extreme focus on costs:

Elango said, “We have got an in-principle approval from ONGC for connecting to their pipeline. It’s just 4 km away from our block. We had taken this into consideration while bidding. If it weren’t there, we would have to set up a pipeline for 150 km to reach consumers.”

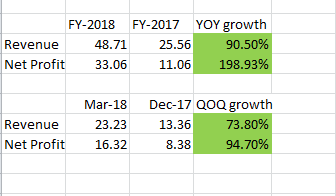

Great set of results.

I have only considered the revenue from operations. I have also removed the exceptional item of 28.94 cr from FY-2017 Net profit and 4.48 crore exceptional item from Dec-2017 quarter.

Board has also decided to issue stock options for the management.

With reference to the intimation submitted to the stock exchange on January 20,

2018, Board has approved the vesting of 10,00,000 stock options to Mr. P. Elango,

Managing Director and 7,50,000 stock options to Mr. R. Jeevanandam, Whole-time

Director &CFO. No further payment of cash compensation towards performancebased

cash incentive as set out in their respective earlier Employment Agreements

will be payable, post exercise of the stock options vested.

Very detailed information on their existing operation and planned explorations.

Disc - invested, will be increasing my exposure

Certainly these are very positive developments for the company.

I had a small doubt: Any idea what the Oil price or gas price assumption has been used to arrive at these projections of 100crs PAT by FY19 and additional 100crs PAT from the B80 Mumbai offshore fields in FY20?

Hi MK,

I have no idea the price assumption used for this projection.

You can listen to the latest conference call for related information. Though I couldn’t attend it completely, they have mentioned that these estimates are on the conservative side. Hopefully they will deliver more than these numbers. They will share the revised estimates after Q1 results. Also, they have not included the results for the currently acquired Geopetrol International.

Negatives:

They are not able to sell the gas produced in Dirok. Hence, there is some delay in the expansion of the pipeline. It will be completed by June. Though management has promised that this problem will be solved soon, but it needs to be monitored. It can have negative effects on the sale.

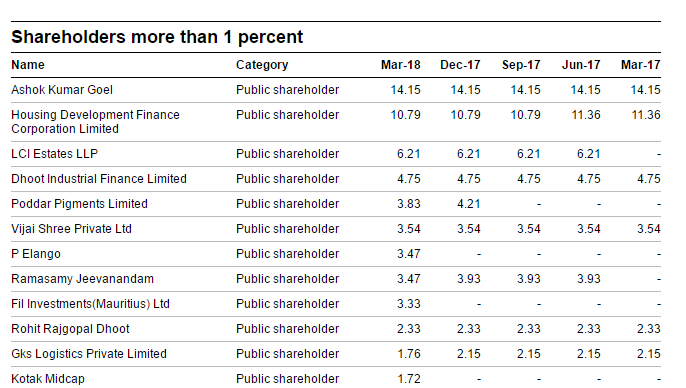

There is a significant holding acquired by CEO - Mr. Elango (3.47%), Fil Investment(3.33%) and Kotak Midcap(1.72%) during Jan-Mar’18 quarter.

Disc - Invested

Super. Which site gives this information?