Old report but it is in detail…worth to read it…

http://www.hdfcsec.com/Research/ResearchDetails.aspx?report_id=3018476

Old report but it is in detail…worth to read it…

http://www.hdfcsec.com/Research/ResearchDetails.aspx?report_id=3018476

few years back company embarked on a journey to change its product mix bringing asbestos mix to 60%. Successfully they also introduced pipes, expanded blocks capacity. Any idea whats the revenue mix of pipes, boards, and blocks as of today? Also is company expanding into any of these non-asbestos categories?

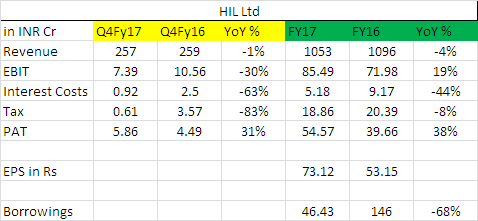

HIL declared its numbers yesterday. YoY there is a decline in borrowings by 68% and EBIT up by 20% while topline degrew by 4%.

Notes from HIL AGM held on July 18 2017

Q) Have any States banned asbestos

A) No …however one gentleman (after AGM) mentioned that in Kerala there is some case going on to ban asbestos use in schools

Q) Even tho net profit has gone up in latest qtr (compared with prev yr) with eps of 49.5 in qtr, the topline is flat

A) Turnover flat due to impact of GST …reasonably confident on year ahead. However do not see much top line growth in asbestos

products. Will be focusing more on pipes and fittungs (CPVC & UPVC) going ahead.

Q) Since 3 out of 4 units have been moved out from Sanathnagar …any plans to use the said land

A) No plans as of yet …own some of the land and some of the land is leasehold in Sanathnagar

Q) Co has strong balance Sheet …but is very conservative

A) Agree …will not become aggressive in future but plan to be less conservative

The Charminar brand is strong and has good customer recall …now plan to grow the Aercon brand as well …the future capex will be

around growing this brand and investing in the pipes and fittings (CPVC & UPVC) business.

FYI

HIL Annual Report for FY 2016-17 (2.9 MB)

Thanks for the notes. HIL (and every other player in asbestos sheets industry) has been trying to increase share of non-asbestos products in revenues from last 3-4 years. But HIL still is largely dependent (~75%) on asbestos products for its topline. Did you get to speak to management on changing revenue mix, what does management say about it?

Thanks

Rajat

Management mentioned that the focus in future would be on pipes and fitting (CPVC & UPVC) but did not give any specifics. on revenue mix…the MD is new and they have not yet frozen their strategy

sure, thanks.

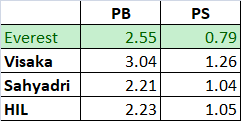

Have you analysed any other company in this space - Ramco, Visaka or everest?

What is your view on the valuation of HIL and others (if you have followed them too)?

thanks

Valuation wise - Everest Industries seem to be reasonable at this price.

Increase in product awareness and adoption of higher margin Fibre Cement Boards (FCBs) lead to recent run-up in Indian roofing businesses. I dug deeper to find whether FCB has potential to be a game-changer in construction building material industry. If you are interested to read what I put together, please click here. I am looking forward to any questions/comments.

Disc: not holding HIL.

Came across this 2016 documentary which points towards HIL… do we know if Asbestos is still used ?

Company has come out with solid set of numbers for Q4 FY18.

Good growth in revenues leading to substantial increase in margins in turn leading to high growth in profit.

Link to results

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=bb2b643a-b1fd-4c9b-a2ba-71aa372b9254

Latest Presentation

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=6e79911e-05d2-4e96-978b-1012dd8a0a18

Key highlights -

d/e of 0.12

Debut as CSK sponsor in peak season leading to higher brand recall. Q1 is historically the best quarter. The company might surprise us on the positive side in coming Q1 results.

Has setup new plants keeping in view the increasing demand for SWR pipes.

Has launched non-asbestos green roofing under charminar brand and has also setup plant for same.

Working capital has come down from 12% of net revenue to 4% of net revenue

Overall a lot of positives can be seen.

Disclosure - 10% of portfolio. No transaction in last 6 months.

Highlights of the Q4 concall (source: capital market)

Roofing would constitute around 65% of total sales and grew by around 10% in FY 18 in value terms and by 6% in volume terms.

Building product segment which constitute around 30% of total sales grew by around 15% in value terms and 11% in volume terms in FY 18. Within Building product segment, Boards and Panels segment grew by around 33% in FY 18.

Pipes and fittings which form a part of Other segment account for around 5% of total sales and grew by around 23% YoY in FY 18.

The company has started its sales to institutional side in roofing segment in FY 18. The company has started dealing with real estate builders, dealers, contractors and has stated supplies of its roofing solutions. Green roofing which has been launched in FY 18, received a strong response.

The company has commercialized commercial production of pipes and fitting segment in Andhra Pradesh in FY 18. Of the total capex planned of around Rs 100 crore for this segment, around Rs 40 crore is spent in FY 18 and rest will be incurred in FY 19.

Company is very bullish for its pipes and fitting solutions. It has started offering SWR pipes and fittings, pipes with heat resistance, fire sprinkler facilities etc in FY 18.

The company expects to present entire new package of pipes and fittings products to the market. Expects the sales from pipes and fittings to increase to 10 times from current FY 17 levels in next 4-5 years.

The company has partnered with CSK team in IPL which has led to higher spend in brand awareness.

Management has attributed the Mar 18 quarter strong performance to brand recognition and increase in reach.

Company is confident of delivering strong operating performance going forward as well.

Company’s Charminar brand is very strong in roofing segment and expects to benefit significantly going forward on upgradation of rural housing and infrastructure spending. Company’s market share as on Mar 18 stood at 21% in roofing segment.

Opportunity is large given deficit of housing in rural and semi-rural areas. Multiple government programs will aid further growth.

I was checking this company for investment as recently it has produced very good quarters. March quarter is also very good.

But I am stuck here:

Recently in Mar, 2018 quarter, HIL Ltd has not declared the consolidated result. It says that JV is not in its control and asked for exemption from Ministry. It has received the exemption.

Again after that, it has given notice on 7th June, 2018 for the investment for Rs 1000 cr which is a very big amount. They mention the intention for this amount as below:

This line is not clear to me. If it was investment then it was easier to understand. If it is going into those JVs for which company has not given Consolidated statement this quarter then what is going with those heavy investment can remain unknown to us. Rs 1000 Cr is not a small amount for this company’s size.

To make investments or to give loans or to give guarantee(ies) or to provide security(ies) to other companies or body corporate.

I read it like this: It is going to do anything with that big amount of money. and they may not tell us clearly.

Therefore, I dropped further checking in it and ignored it as an investment stock.

Disc: Not Invested.

Acquisition looks like good for HIL and may help them double the revenue. Any views from seniors will help.

Parador is a leading flooring brand in Europe. HIL has the right intentions of growing Parador’s business in Indian and other asian markets. Parador is mainly into Laminates. So this acquisition HIL into a newer territory. So now the company has 4 brands (once the acquisition is completed):

Charminar: Roofing

Aerocon: Walls n plumbing

Hysil: Insulation

Parador: Flooring

So this acquisition adds another dimension to their business. They expect the topline to grow by 100%, if the same margins are maintained (8-10%), their profits will be handsome in the coming years.

Info about Parador:

Parador laminate flooring is designed and manufactured by a German company. Parador was founded back in 1977, with the first laminate designs available from 1995. Today, Parador offer their customers the choice of more than 2000 products, which are sold in 65 countries all across the world. Parador have two locations in Europe: they started in Coesfeld, Germany, before expanding and opening a further plant in Güssing, Austria, in order to meet the high demand for their flooring products. We import all of our Parador products directly from Germany, and we place an order for this every Thursday. With this in mind, it could take up to 14 days to get your order to you.

Disc: Invested

With new acquisition in tough time by HIL, rating agency put its rating on watch -

https://www.icra.in/Rationale/ShowRationaleReport/?Id=71671