Hero may capture some market share but what would be the margins ? how does the contracting work with harley?

That’s the exact thing they haven’t clarified yet. They are yet to announce the royalty structure. Margins for Royal Enfield bikes scale upto Rs 75,000 per bike for Eicher Motors (40% gross) so for Hero too they should be revolving around the same I guess.

In my humble opinion margins won’t be even nearby Eicher. Eicher owns the product/brand/tech. Hero is like a contractor/distributor.

Time for Hero to shine again??

Below a small quarterly and half yearly performance comparison with TVS

HERO: Q2 EPS has shot up from 34.45 2022 to 50+ 2023; 46% growth

TVS: EPS flat at 8.14

H1'24 HeroMoto EBIDTA grew 28% while TVS had 24% growth

While TVS is trading at EV/EBIDTA of 17.5; Hero is trading at a much lower 11.4!

If Hero can start excelling TVS on Ebidta growth levels for a few more quarters, it can be much better on PAT/EPS level — Hero has no debt, while TVS’s balance sheet is stretched with D/E 2.04

Remember Harley Davidson and other new launches are yet to start showing in the P&L from Q3 onwards…

2 Likes

The problem with hero was low margins because of its portfolio comprising of low margin vehicles and rural slowdown due to high prices of their bikes, the management execution on premiumisation will in my opinion lead to rerating they have introduced a lot of products in their portfolio if it reaches good scale valuations whould be much higher as compared to TVS due to no debt, I have invested primarily because of its investments in Ather which I think is growing very fast, I was amongst the first buyers of it in my city in 2020 its really a nice bike and since now they are entering internatinal markets starting Nepal, also if management can deliver on premiumisation front with subsidies now reduced by a lot many substandard EV brands which used to import from China will not be able to survive, also EV prices will increase so only strong players will survive so the trend due to shift in EVs will take time, heromoto corp is in a good position now, only instead of positioning vida as a premium product they could have tried to make a mass market vehicle and dominate that space.

If company delivers on premiumisation will add more.

Disc: Invested and biased.

3 Likes

To make good money earnings has to increase with it if growth comes back then there will be pe expansion, since for the last 5 years there was no growth valuations are undemanding at 20 pe, Ather has production capacity of 420000 vehicles which they are planning to build a new factory outside TN so demand seems to be not a problem considering their capex plans, also they have stopped freebies, free charging at ather grid and paid connection plans to connect phone with scooter so they are although not making a profit due to growth, their margins should be high considering their premium positioning, also hero is available at around USD8bn I am considering Ather atleast at 1bn USD value and their stake in it is around 34% considering the compulsary convertible preference shares issued to hero their stake could be around 50% at 500mn USD atleast.

2 Likes

Hero have already stated that after taking Vida to 100 cities in this fiscal year, they would be launching lower-priced EV products in FY 2025.

1 Like

Recently written a thread on Hero Moto Corp would appreciate any feedback.

https://x.com/rankamoksh/status/1730832601902985570?s=20

2 Likes

Looks like HeroMoto shall rerate soon when market realises the value of its associate company Ather.

2 Likes

Any idea why TVS is valued at a very high PE of 68x despite a debt-to-equity ratio above 2.0 whereas Hero Motocorp is valued at a low PE of 26x with almost no debt? ROCE is also higher for Hero. OPM is similar for both.

Look at price to sales metric, hero is valued at around 87000cr whereas tvs at 99000 + 12000 cr in dents so around 1,11,000cr, although both have similar margins, I think it is because of better product portfolio of TVS and also Hero had some CG issues related to promoters in the past.

It is because of the perception of the market. TVS is growing at a high rate in the premium segment, whereas Hero’s presence there is miniscule. Now, whatever growth is expected in future is majorly from the premium segment. So, that’s the reason.

But the good thing is that Hero is also introducing new products in the premium segment, and as and when they start delivering, I’m hopeful the market will surely give higher valuations to Hero too. Atleast that’s my thinking about buying Hero.

3 Likes

One of the factor for batter valuation is Analysts believe TVS Motor has been doing well since the last few years in terms of sales, especially after it ventured into the electric vehicles (EV) space. On the other hand, its competitor Hero MotoCrop has been late to the EV party. It launched its first electric scooter VIDA V1 October 2022. Meanwhile Hero MotoCop has significant stake (39.7%) in Ather Energy.

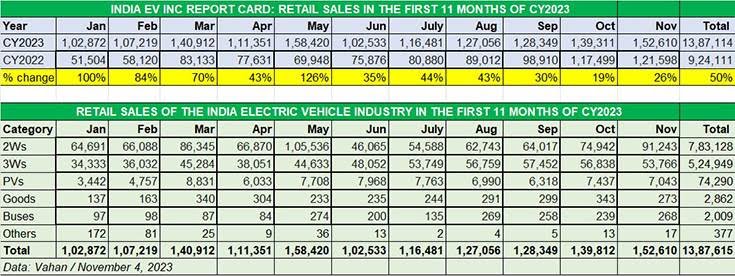

Cumulative EV industry sales, comprising the two- and three-wheeler, passenger vehicle and commercial vehicle sub-segments, for the first 11 months of 2023 are a record 13,87,114 units, which constitutes strong 50% year-on-year growth (January-November 2022: 924,111 units).

The volume drivers for the EV industry are the two ‘low-hanging fruits’ – two- and three-wheelers, which are the more affordable segments compared to electric cars and SUVs, goods carriers.

Look at no.s of vehicle sold by each co. In 2w segment.

An other reason may be Money Laundering Prob. against co and Executive Chairman Pawan Munjal in past.

Disclaimer:- invested. No recommendation to buy or sell.

2 Likes

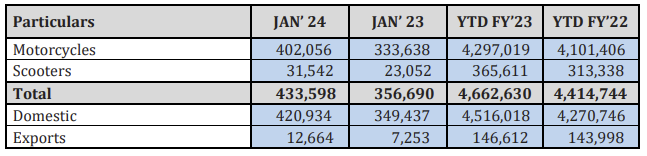

22% growth over Jan 23!!

All round performance across bikes, scooters and exports, all cylinders firing literally! ![]()

6 Likes

Clearly green shoots of recovery can be seen in all segments. On top of that there is an upside of potential rerating of multiple given their foray into electrical scooter business.

Only thing I fear about this company is corporate governance as last year there were a few cases of malpractices found in IT raids. Hope the new CEO can get this sorted.

1 Like

The current multiple is already on the higher side. The electric scooter business may not be as profitable as the ICE business, which means profitability at the consolidated level will be pulled down. Unless EV business improves profits, and scales up meaningfully, there is limited upside potential. Rest we know Mr. Market, the stock can go anywhere based on the mood. There seems to be limited margin of safety at these levels.

Disc: No holdings

2 Likes

Premium segment will definitely see a war for market share with Hero doubling down on their premium strategy (plus partnership with Harley Davidson) and Bajaj increasing focus on domestic market. All of these players have the same advantages (distribution, brand and scale) that you have highlighted. TVS is doing quite well and most of all those positives seem to be priced in (at a lofty P/E of 60) as stock has seen one way rally for last couple of years.

So If in future Ather energy does well in terms of valuation, how it will affect Hero and its share price. My understanding is that Ather’s increased valuation will increase Hero’s Book Value and if Ather pays dividend in future those will be counted as Other Income in Hero’s income which might not be much.