You bring up a valid point. While employees have the option to sell immediately, they also have the option to hold, which could indicate a long-term investment in the company. Employees might convert ESOPs to equity for reasons unrelated to their perception of the company’s future, such as tax planning. Immediate selling may attract STCG.

It’s crucial to consider the context in which the ESOPs are being converted. If the conversion is happening during a period of strong company performance and growth, it’s more likely to be interpreted positively. Conversely, if the company is underperforming or facing challenges, and there’s a mass conversion and selling of ESOPs, that could be a red flag.

2 Likes

Either way, it’s insignificant as per my opinion. We - active investor are different species vs other people including company’s employee.

I remember hearing ex CFO of shree cement (Mostly chennai investor forum - lecture by mohnish pabrai) - CFO saying, something like, I always feel stock of shree cement is over valued and couldn’t able to invest while I was employee. Just to mention few years ago shree was multibagger.

4 Likes

1 Like

There is a news CVC capital looking for an exit. Did anyone analyze if that would be good or bad for the company?

Source - Healthcare Global soars 5% on reports of CVC Capital looking to sell controlling stake

2 Likes

Interesting question; incidentally no straight answer . Management change is always Binary “0” or “1”.

How in case of HCG this becomes more interesting:

Pro’s for new management:

- Tailwinds in the sector.

- M&A opportunities (outgoing management has initiated the process)

Cons for new management:

- Frequent change in ownership might be demotivating for the staff.

- Technology upgradations might require deep pockets & swift actions.

- Competition from Multi Speciality of hospitals : Most of established players are either opening or expanding Oncology department at their sites.

So no straight answer, trust this gives some insight.

Disc : Existed recently, considering risk / reward in HCG v/s Peers

3 Likes

There is no official announcement I believe by CVC yet but if holds true a lot depends on who is actually the buyer.

Whether it’s a simple financial transaction or strategic buyer taking stake in HCG.

Strategic buyer will bring added advantage and experience and bring more synergies to the table to align with their existing process.

4 Likes

CVC Capital aims to sell its 60.42% stake for over 4000cr. That values the business around 6230cr.

Current Mcap around 5214cr. Lets see how this plays out. Technically strength was visible even during the recent correction in market.

4 Likes

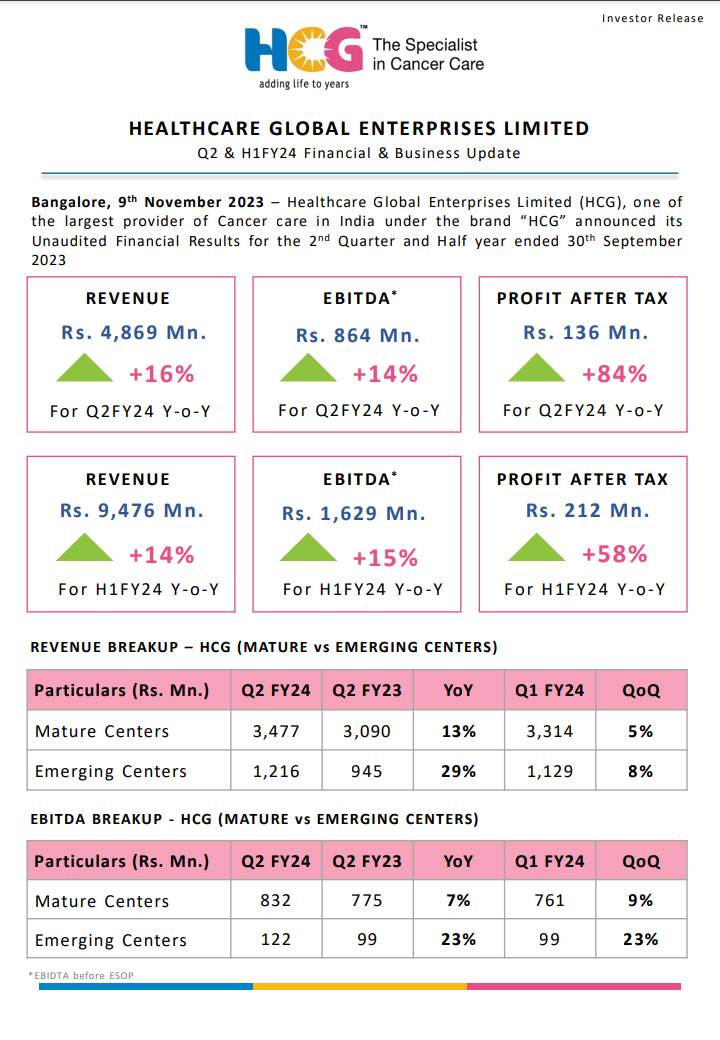

Q2FY24 EPS jump 83% YoY. Looks like operating leverage started playing out.

**HealthCare Global Enterprises Ltd. (HCG) Unveils Strong Q2FY24 Results and Operational Highlights! **

Financial Snapshot:

- Q2FY24 Revenue: ₹4,869 Mn., a substantial 16% YoY growth.

- Q2FY24 EBITDA: ₹864 Mn., a robust 14% YoY increase.

- Q2FY24 PAT: ₹136 Mn., showing significant growth.

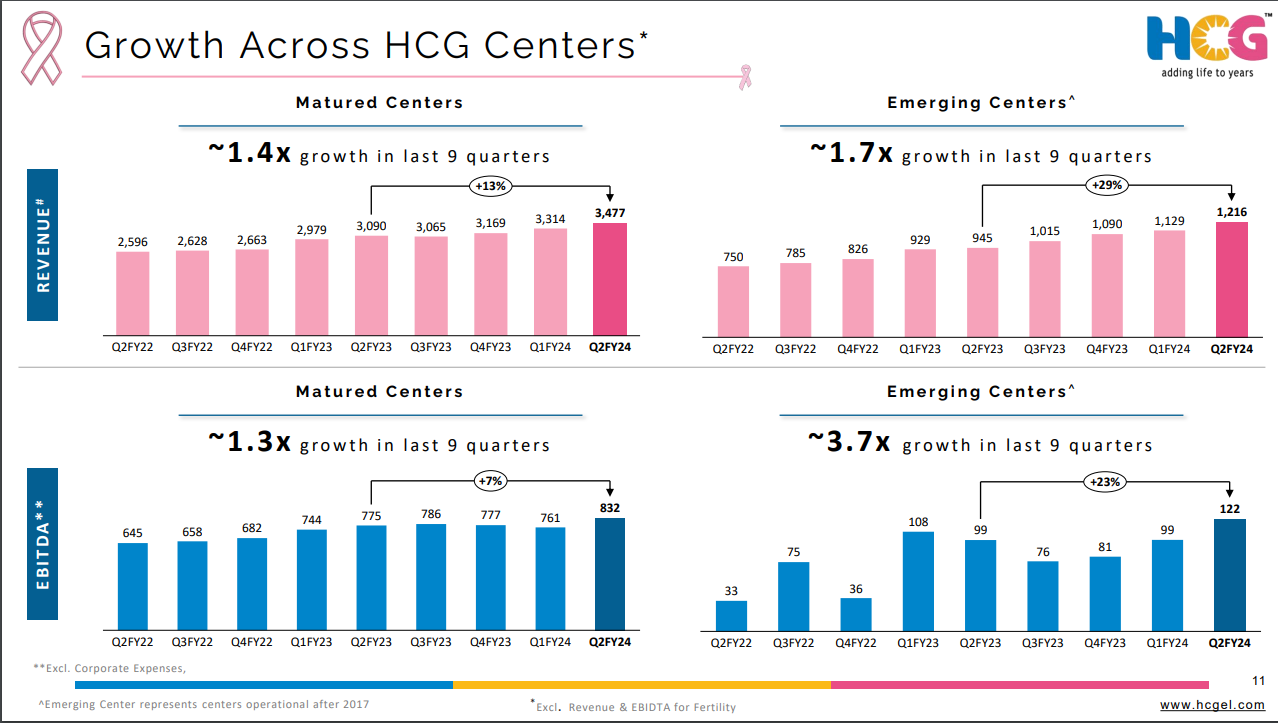

- Revenue Breakup: Mature Centers - ₹3,477 Mn. (13% YoY), Emerging Centers - ₹1,216 Mn. (29% YoY).

- EBITDA Breakup: Mature Centers - ₹832 Mn. (7% YoY), Emerging Centers - ₹122 Mn. (23% YoY).

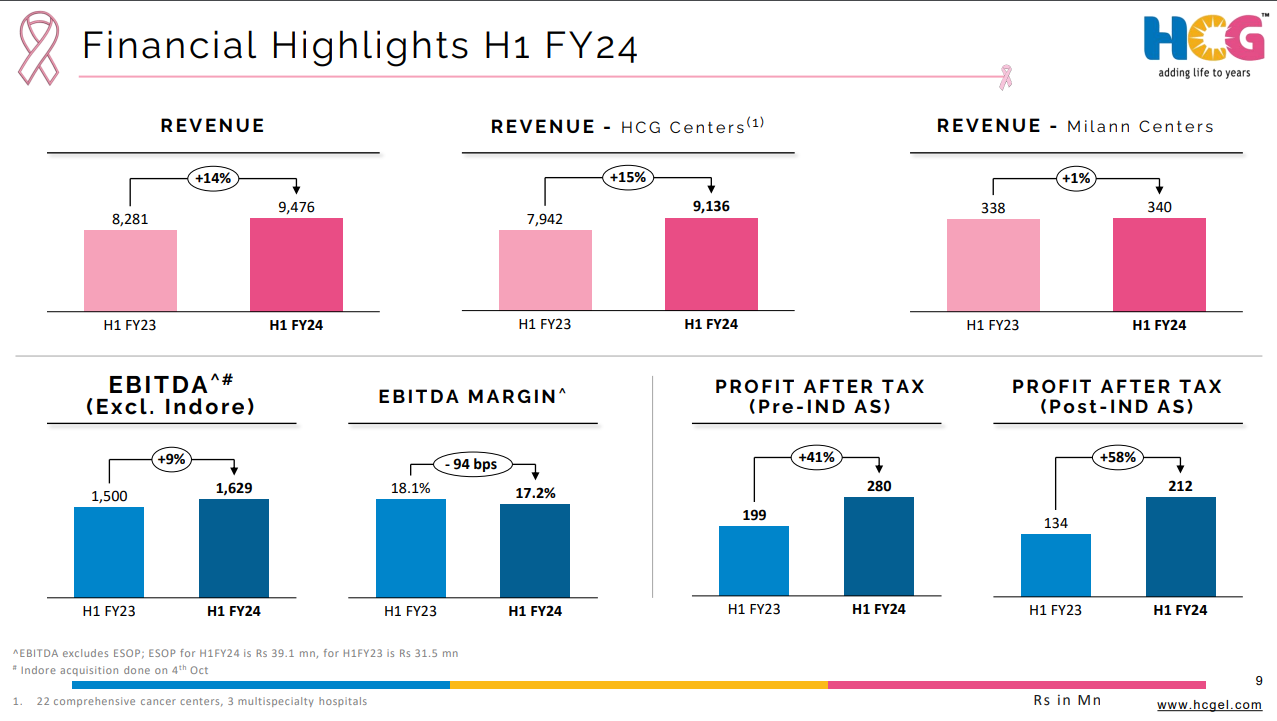

Half-Yearly Performance (H1FY24):

- H1FY24 Revenue: ₹9,476 Mn., a strong 14% YoY growth.

- H1FY24 EBITDA: ₹1,629 Mn., reflecting a 15% YoY increase.

- H1FY24 PAT: ₹212 Mn., a remarkable 58% YoY growth.

Operational Highlights for Q2FY24:

- ARPOB: ₹42,054, up from ₹36,914 in Q2 FY23.

- AOR: 63.6%, maintaining strong operational efficiency.

-

RoCE (Q2FY24 Annualized):

- Mature Centers: 21.2%, RoCE pre-corporate allocations at 25.5%.

- Emerging Centers: -3.9%, RoCE pre-corporate allocations at -0.8%.

- High Double-Digit Growth: Key markets like Kolkata and Mumbai grew by 42% and 41% YoY.

- International Operations: Witnesses robust growth at 175% YoY.

Infrastructure Enhancement (Q2FY24):

- New Additions: 3 LINAC machines, 3 Robotics surgery machines in Mumbai, Kolkata & Baroda.

Leadership Insights:

- Dr. B.S. Ajaikumar, Executive Chairman: Highlights strides in outcome-driven cancer care, groundbreaking studies, and the acquisition of SRJ CBCC Cancer Hospital in Indore.

- Mr. Raj Gore, CEO: Emphasizes the commitment to patient outreach, capacity enhancement, and integration of acquired hospitals to extend cancer care services.

11 Likes

2024 Feb - Q3FY24 Concall:

Floods in Chennai & Strategic decision of coming out of ‘shop-in-shop’ model led to a scale-back of operations in M S Ramaiah Bengaluru, affected revenue growth by 2-3% and also EBITDA by 30 bps for the quarter

Decline in Q-o-Q PAT is on account of depreciation for acquisitions of Nagpur and Indore

Q3 is generally a seasonally muted quarter

Overall ARPROB is increased to 42.8K INR, a15% Y-o-Y growth

Centers of excellence delivers 30% margins and ARPOB is above 70K INR

Increased 59 beds during Q3

Current total no. beds: 2000, occupancy at 65-70%

Adding a new 100-bedded hospital, a comprehensive cancer care in North Bangalore, Capital outlay about 90Crs, expected to be operational in 15-18 months

Going to add 350 beds over next 3 yrs with capex of 130 Cr (48Cr is already spent)

Net debt stood at INR367 crores as on Dec’23. Very comfortable with the current debt levels and project a better cash flow in the coming quarter

Decided to divest Milann division, will be done at max. value possible, more info to come

No comments made on CVC exit plans (no denial, at least)

Moving to a new facility in Ahmedabad due to capacity constraints

May not achieve earlier guidance of 20% Ebidta margin by Q1, Q2 FY25, due to drawdown coming from Indore acquisition, Whitefield project being functional and also increasing Govt. functions.

Generally, need for expansion arises once occupancy reaches late 70%, to keep remaining beds for day care.

Expecting ARPOB to grow at 5-7% Y-o-Y in coming years, lever are combination of high-end treatment, faster turnaround, lower ALOS.

Aiming to grow higher than market which is at 10-11%

List item

2 Likes

They have mentioned debt as 367Cr here but in screener.in debt is shown as 980Cr. Since there is not much change in the interest paid between quarters I dont think they have taken any fresh debt. Do you know why there is a discreprancy?

Also if any of the voard members can please shed light on how they plan to pare their debts down, it would be great. They are paying close to 110Cr as interest every year.