ValuePickr Research

Resources

Basics

ValuePickr Forum

Gulf Oil Lubricants - A low risk way to play the economic cycle?

Stock Opportunities

Untested - but worth a good look

solankidarsh

October 21, 2021, 9:02am

29

image

1920×1040 100 KB

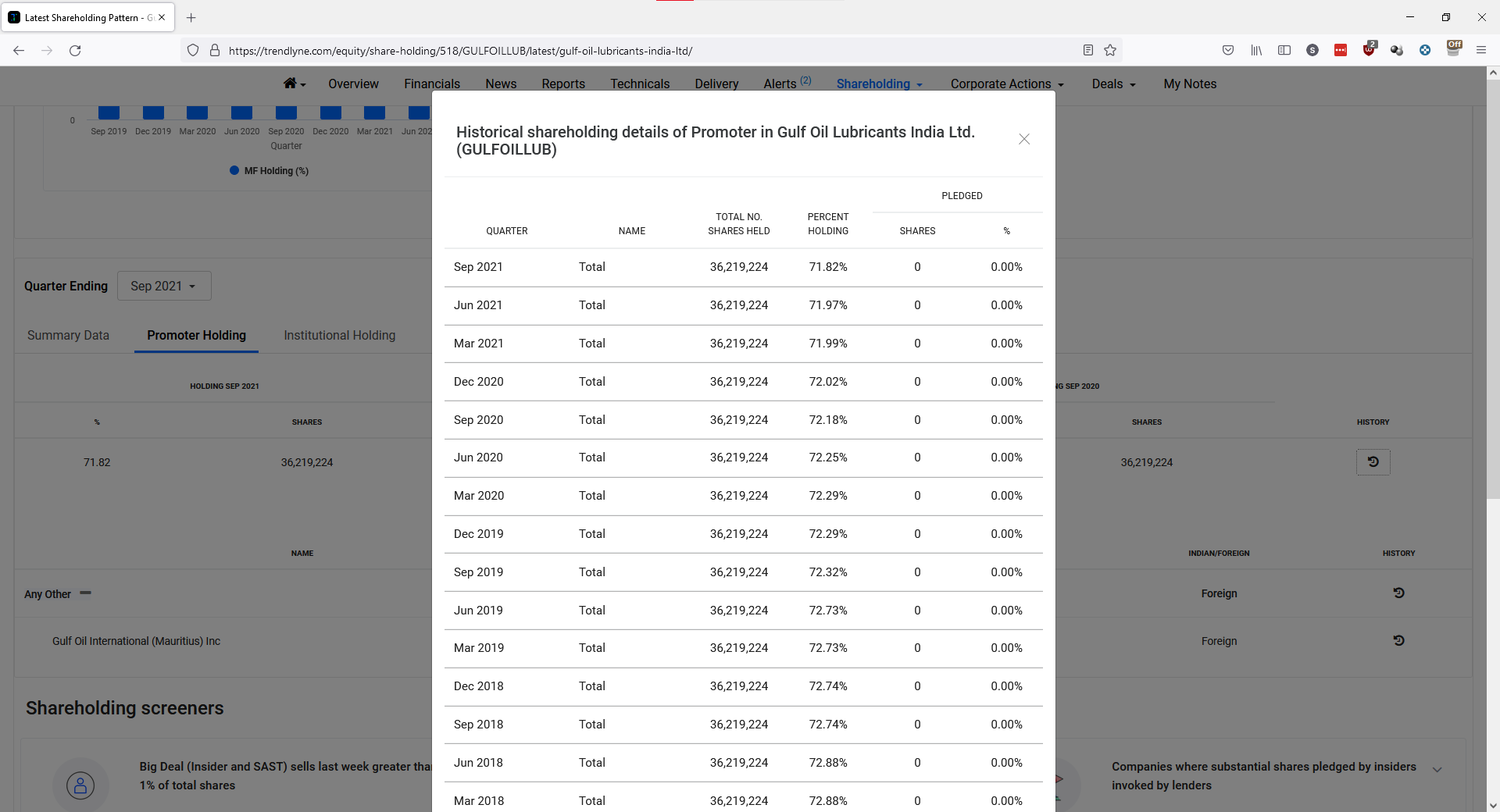

Click on history on the above link

1 Like

show post in topic