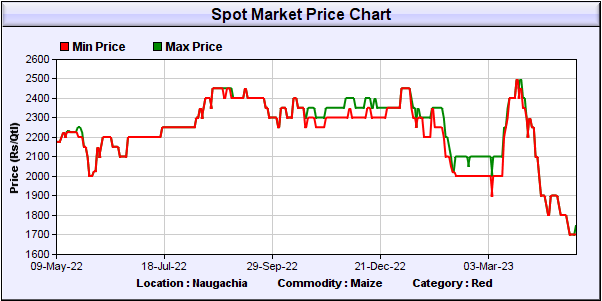

Dissapointing margin for Maize segement. I believe this was mainly because of higher maize prices in Q2 and Q3. In Q4 prices seems to be fluctuating but lower in April. Hope margins to increase in the FY24Q1 & Q2 if company grabs the opportunity of buying maize at lower prices. GAEL should be able to buy at opportunity considering their past record.

Do we have any other reason for the loss in margin by 4%?

When doe we expect revenue increase after Malda plant being started?

Maize is also being proposed to be used for ethanol production. If this picks up, will boost maize price realisation, impacting margins for GAEL. Any thoughts on this? Refer this on Agriwatch.

Attended the AGM today. Here are my notes from the meeting:

Expansion –

Malda Plant commissioned in March 2023 and is operating at 50% capacity utilization which is expected to be ramped up to 75% by year end.

Would spend 700 Cr for reaching 6000 TPD capacity on the following plants:

Started construction at Sitarganj for 1000 TPD. Commissioning in January 2024.

Himmatnagar – Would start construction and Commissioning in Q3 2025

On schedule to reach 6000 TPD by 2025

Expansion to be funded by internal accruals

Sales Target of 10,000 Cr for FY25 is largely on track

Payback for New Projects – GAEL looks at 5 year pay back period.

Exports

GAEL is exporting to more than 100 countries. Focussing on North and South America now.

Committed to increase our market share in International markets.

Export realization – keeps on changing basis the international corn prices and competitive scenario.

GAEL has required approvals from MNCs giving consistency in exports and therefore better able to export vis-à-vis competitors (both domestic and outside).

Industry is allowed to import corn duty free for production of starch.

China + 1 helping exports

China is not as strong in exports as earlier; neither exporting aggressively nor importing.

Target to keep increasing exports.

Not much of a difference in maize prices between domestic and international markets.

Corn prices are competitive wrt China. In China, the prices are regulated.

One plant being setup in North while other in South India.

This would be an import substitution business.

Requires large amount of power – as far as power costs go, there is not much of a difference between India and China. Our power cost is comparable to that of China.

Incorporated subsidiary for this business.

Ethanol Update – Two ethanol projects are on hold due to Raw Material uncertainty and one not started yet. Final decision would taken in few months.

Raw Material fluctuations –

Most critical part for the industry.

Procure raw material on time.

Be connected to farmers directly.

India gets two maize crops (Rabi and Kharif) and Purchase is spread throughout the year.

GAEL has a large storage capacity equivalent to 3-6 months of grind capacity.

Pricing depends not only on the Raw Material prices but also on the demand-supply scenario.

Maize derivative capacity – 32-35%. Target is for 45% of grind capacity.

Buyback and increase in dividends – no such plans in near future as company is on growth trajectory.

Increase in power cost for FY23 was mainly attributable to fuel price increase.

Spinning division – Have converted cotton yarn to polyester. If the profitability does not turn then a decision would be taken in this financial year.

Operate at 5-6% margins for own brands [Total sale of 1000 Cr for edible oil branded business]

Agro division expected to do better in this Financial year.

Renewable Energy Capacity – 25%

Import Duty on products manufactured by GAEL – 10 to 40%

Impact of Malda plant on revenue would be seen in the next 3 quarters.

Market Share

Sorbitol – 30%

Glucose – 40%

Dextrose – 45%

Starch 5 MT industry and our share is 25-28%. Expect industry to increase to 6 MT in next 2 years.

Capital Allocation for next 5 years:

Maize – 1700 Cr

Expansion of Grind capacity – 700 Cr

Fermentation – 1000 Cr

Disclaimer: There may be some mistakes in these notes

Any idea about their volume growth over the years? Do you have these details for GAEL or its competitors ? I can see that the revenue growth is a respectable 13-14%. It would be great to separate it into pricing & volumes.

They are expanding capacities 2x in 3 years. What is the industry growth and whether it can absorb this expansion? Can there be a risk of price war at least in the commodity products in the medium term?

Is there a threat to the industry from imports? I believe their business to domestic FMCG/Pharma would have an approval process and therefore more sustainable and less threat from imports. However for the rest of the business with industries, can imports make a dent?

Are there more details on export products ? Is this similar to domestic FMCG/Pharma business or being sold through traders? Need to understand the quality & sustainability of these exports? Also, who are they gaining market share from & Why?