Some may want capital safety and FD type returns. These investors are only happy to always be invested in Gruh, knowing that the company won’t go bust, and past performance assures them much more than FD returns. Even if some of the returns are shredded back, its no problem. They are just happy people. Mediocre expectations are easily fulfilled by powerful companies.

This is just one perspective.

However, another type of investor, who is an expert and is in the habit of extracting 25% CAGR from the markets. He would probably be most interested in exiting and waiting for the next opportunity.

You are absolutely right. Time and again it happens. Gruh has consistently surprised on the upside.Just when everybody was thinking it was hugely over-valued, bang it goes another 25% in 3 days. Clearly the whole HDFC group is galloping away after the fund raising news. Sanity will prevail and prices will come down but not what we expect. The whole India story is at an elevated level now with Budget,Davos etc.Sooner or later corrections will happen time wise or price wise.If we look at Gruh’s past behaviour-patterns are same.

It is a myth that HOLD is different from FRESH BUY, except for irrational emotional reasons or to avoid Short Term Capital Gains Tax.

The price I purchased at more than a year back is of no consequence except for self-gloating or self-loathing.

If I cannot buy at current price , why should I hold? Except for the lack of any other possible opportunity in any asset class/ stock.

So if I have Gruh and it is quoting at 700 and if even if I purchased it 5 year back, it makes no sense if it is going to be only 750 by Dec 2018 in my assessment.

Only current or yesterday’s quote is my real purchase price.

Let us focus on business. Has Gruh potential to become Rs 300000 Cr company like parent HDFC in next 15 -20 years ? How much dividend GRuh might be paying after 15 years ?

I knew someone was going to tell this. Yes technically you are right. But its very difficult to buy the stock again. Because these kind of look overvalued all the time.

Using the sale proceeds to buy something new is also not easy, especially in a market like this.

220 means around 2 yrs back. I would continue holding it.

My funda is this:

I buy a company if I think its stock will give in a certain “Future CAGR”.

After buying it, if the company suddenly rallies by, say, 30% in a month then my “future CAGR” will be less. But that does not mean I will sell it. Because I HAVE TO consider my “Total CAGR”. Total CAGR is the returns the company has given me till now AND future returns.

If I ONLY consider the “Future CAGR” in my decision making (and ignore the “Total CAGR”) then I will perpetually be selling my winners and will perpetually be looking for new companies to invest in!

In fact, the point that I am making in this comment is: HOLD is different from FRESH BUY and can be considered as a response to what @Yatharth said few comments back (“It is a myth that HOLD is different from FRESH BUY”)

Thanks Chirag. I hold a small qty of Bosch, when it went to 28k, I wanted to hold it forever… now it is at <20k. Similar is the story with Crisil & may be Eicher!

Along with my fundamental analysis, I have been reading up about technical analysis (link to the book that I like) too.

One thing that I learnt from reading the technical analysis is, it is NORMAL for stocks to retrace 30% to 60% of their last rally.

To take example of GRUH. Its last rally was from 500 to 720 i.e. around 220 points. It would be a normal move if GRUH re-traces back to 600-620 level before Q4 results.

My main rule is I will not accumulate at the top. I will not chase the momentum. Stock price should be between its 30 and 100 day moving averages for me to buy/accumulate. Basically, I will accumulate only after a “correction + consolidation” OR “just consolidation”.

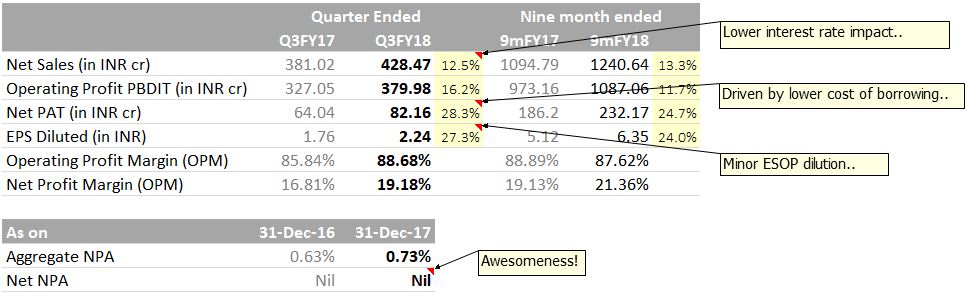

People in this forum are busy debating on valuation. I have not seen a single comment that Gruh has come out with its Q3 result today. Looks Bull Market in its primeGruh -Q3-2017-18-Result.pdf (620.2 KB)

If we hold stocks forever, we only get dividends. We never sell and hence we never get the price appreciation. I hope that when we say that we are going to hold forever, we are sure that we are investing only for the dividends.

This is similar to buying a house, you don’t save monthly rentals you pay rather you get appreciation on the investment (we buy thinking its forever except a few who are in the business of buying / selling property & sometimes we move to other cities and end up selling it)… here when you buy GRUH forever, its not only for dividend but appreciation on investment… although I understand that dividend yield for GRUH is not attractive which forces anyone to buy it only for dividend

This sounds like a new theory of real estate investing. I thought that the deal while buying a house for the long term was that we make an investment and earn/save rent for as long as the house is livable. Also, add the worth of the nice feeling of owning a house to arrive at its value.

If I am not going to sell a stock forever, then its appreciation will only give me a happy feeling and no money apart from the dividends. This is what the friend boarder pointed out and I further emphasized. I think that when people say that they will hold an investment forever they actually mean that they do not intend to sell it in a very short period of time.

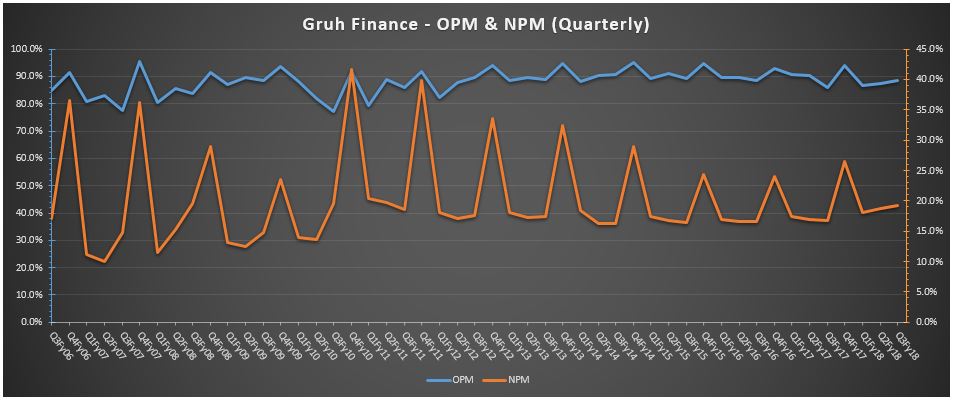

Gruh has reported >25% PAT growth in three of the last four quarters. Start of up trend. Market is expecting this to continue (and probably accelerate) in quarters to come. Expecting >25% NPM in Q4Fy18 (co’s strongest qtr).

“If the growth rate is so good that in another ten years the company might well have quadrupled, is it really of such great concern whether at the moment the stock might or might not be 35% overpriced?”

“If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never. ”

PHILIP FISHER (Guru of Warren Buffet)

With Gruh, it will always test your patience and will never tell you before it makes it big moves.

I bought Gruh at 221 and have been buying Gruh for over 7 years.

I feel sometimes a 20% in gruh is too much to ask for and someone can offload a bit.

But make no mistake to allocate that capital to other stock thinking that you are smart.

I have myself failed to sell the stock on Friday at 713 but in hindsight I feel it is a mistake.

Having said that I am super bullish on another two decades on Gruh. But these one time opportunities should be expoited and sold into to buy it back at lower price. (And making no mistake to allocate in other companies).