yes, they will sell this portfolio before losses emerge like they do with other businesses. Thank god they can’t do same in IT or pharma.

1 Like

Govt allows 41 more housing finance cos to use SARFAESI law. Can any of the broaders throw more light on it.does gruh repco are already under sarfaesi law

results today - expect it to be tepid - my eps no for FY 17 is 9 . If they continue to perform below expectations PE can constrict to 20 levels ? no positions

Results announced http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/FFBF919D_7E8B_48E7_805E_3D569D44B6F9_141149.pdf

Attached is the presentation for Q3 FY16.

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/BA4DD75E_1652_4F53_905C_6DF667A60A86_132908.pdf

Thing to notice is CAR.

Risk weights have changed dramatically CAR now stands at 19.7%

Dear Friends,

Can you guys share some PDF, Links to get sectoral understanding of HFCs, Its SWOT, long outlook , driving factors, market size & industry cagr, threat from banks & NBFCs, etc. Seems every ace investors are betting on HFCs. Now there must me some tailwind in the sector for sure, otherwise why it would come up in RF, Microwave & Mixed Signal Solutions | Mercury Systems ![]() On a lighter note, I am bit afraid, I read some where " The moment your stock or sector is making TOI Headline, its nearing a crash "

On a lighter note, I am bit afraid, I read some where " The moment your stock or sector is making TOI Headline, its nearing a crash "

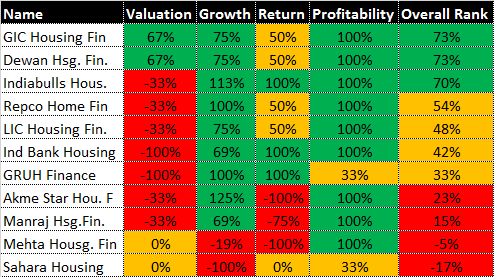

However I tried my best to do a fundamental analysis & relative valuation on HFCs, interestingly GRUH Finance is not among the top - from entering perspective. Need views on whether the analysis makes sense. Clearly valuations are not attractive & margin contraction is happening, thus rank has gone down compared to peers. However its also true that paying up for quality is not bad. Bit confused ? ![]()

Also why all Realty stocks are beaten down to death, property brokers are jobless, Metro cities home prices have corrected by 30%- Delhi/NCR but HFCs are doing quite good / continue to do good. Isnt there a disconnect.

If you really look at the housing finance market, the two biggest lenders are SBI and HDFC. They finance houses constructed by big builders in metro cities. That end of the market is definitely under pressure. But India has huge population and the need for housing is pretty large. The demand at the lower end of the market will never go out of fashion. Houses that cost 50 lakh+ are feeling the heat while the houses that cost less than 50 lakh are still getting sold and purchased in large numbers.Most of the companies in your list finance such purchases.

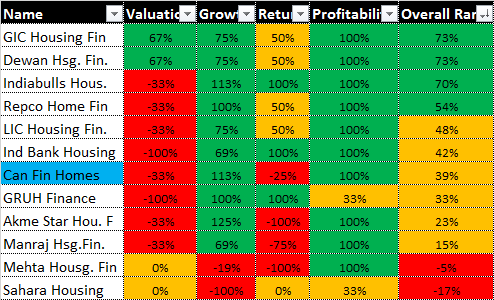

BTW, you are missing canfin homes from your list. That could be another interesting company to compare.

Hi Gyan,

Thanks for pointing out Can Fin Homes- I didnot know. Updated canfin.

SBI has nearly 16000 branches in India presently, of which 9,851 (66%) were in Rural and Semi-urban areas is a Behemoth- Wikipedia Take financial inclusion into account. Why will tier 2/3/4 people pay 12% interest to HFC & not 9.5% to SBI. Also include SBI subsidaries. May be I am missing something. ![]()

May be HFCs are playing aggressive, May be First mover & Fast mover strategy. So far so good…but whats the future like, I am still not clear.

Hello Anupam,

Thanks for the good analysis.I have started investing from this new year and learning the value investing.

Your spread sheet looks great so can i know how you have calculated valuation and overall ranks.Also many people are talking about P/B for NFC so any thought on calculations.

Sorry if its simple questions :).

thanks

satish

1 Like

No offence to your analysis but have you incorporated corp. governance in your overall rating? This IB group at 3rd rank is completely avoidable.

Disc: invested in Repco

1 Like

Only past history analysis. Taken various ratios & rated as per standards & ranked. It only shows history.

Future outlook, Corp Gov, Industry evolution etc not taken into account- For which VP forum is the best place.

anupam this way of looking at companies (valuations only) for investment is not prudent and advisable . if it was so easy to get pe ratio , div yeild and valuation matrix than everybody on dalal street would be millionaire.

when ever you analyze company look at business matrix (ROE, May be book value and NPA in finance firms and most important is to look for future growth drivers with respect to size of market and potential , ability and credentials of management) valuation comes at later stage thats why smart investor dont want to look at price first , before analyzing business.

now coming to banks competing against HFC, it is already there and still HFC guys are growing. This branches of SBI and other banks were there. but problem / opportunity for HFC is that banks dont lend to individual with small ticket size and if some one goes to PSU banks for loan they have more reasons to refuse Housing loans than give (no incentives for staff to lend).

now more importantly competition for HFC is increasing as more and more players want to have stake in growing and easy looking business like housing finance.

future is always and will be uncertain , our job is to buy risk adjusted good , great companies that pay 3 to 1 and have odds of fifty fifty .

Happy investing

3 Likes

Good analysis as far as numbers are concerned. However most of the HFCs have varied business models and strategies.

- Dewan/Indiabulls seems to have huge construction finance book (loans to developers considered as housing exposure as per NHB) these loans have inherent risk which these guys are managing somehow

- Gruh/Repco are banking more on the non banked/non salaried class (pan walas, Barbers, etc kinds business community) where spread is high and predominantly retail book.

- Gruh has derived a variable interest charge model depending upon risk and has expertise in those credit( you can check this from the consistency of their numbers)

- Their rural play and diversified retail book combined with huge rural push by Govt of India on housing for all has still huge opportunity to play.

- Banks like SBI and PSUs are giving good fight though they have difficulty competiting as

- Focus( they have way too many products and focus only on housing expertise lacks

- rural landscape and clear title is problem for banks and focused house credit lacks expretise.

- TAT is pathetic, please try SBI for rural housing loan once and try with Gruh or repco!!

most of the finance business is on TAT than on rate sensitivity as theres hardly any change in EMI with change of rate to 2%

regards

As PSU Banks have been hit hard on corporate loans, they are becoming aggressive with housing loans. e.g. A lot of PSU banks are advertising housing loans. SBI has become largest HFC company.

As @Jinushah explained, companies like SBI and HDFC mostly lend to salaried people. On top of that, they have a top class documentation verification process. That works really well in metros as you do a thorough documentation check for an apartment complex and then they do quick approvals for individual flats. That kind of check in the rural areas and smaller cities for a small loan will simply not work. That end of business is too small and extremely ineffective for the kind of thorough check that biggies do. That is where the HFCs come who will take up these loans with a quick verification process. People want quick loans rather than a prospect of getting rejected after a thorough check.

In December quarter results presentation, Gruh has increased CAR i.e. from 16.81 to19.7. Leverage is reduced, it will reduce ROE and hence growth.

Reason is difficult to understand. It may be because they are not able to disburse enough loans because of higher base. Any comment ?

Gruh’s leverage has increased yoy as of Dec 2015. It is now at 12.5 vs 11.6 as compared to last year and significantly higher than its past average and hdfc has grown 20 percent for many years so higher base cannot be a reason for slow growth.

The CAR of all housing finance companies has increased last quarter. This is due to change in calculation of risk weighted assets for housing loans. The risk weight for housing loan is reduced by RBI/NHB.

2 Likes

An article on Gruh finance shared by @Doonsrini in the other forum.

GRUH Finance - FY16 results on April 19, 2016

Gruh Finance Ltd has informed BSE that the Company’'s Board Meeting will be held on April 19, 2016, inter alia, to consider the Audited Annual Financial Results for the year ended March 31, 2016 alongwith 4th quarter results, and to consider the recommendation of dividend, if any, for the year 2015-16.

In this connection, the trading window for dealing in the shares of the Company shall remain closed from March 25, 2016 to April 21, 2016 (both days inclusive) in terms of the Share Dealing Code and SEBI (Prohibition of Insider Trading) Regulations, 2015.

http://www.moneycontrol.com/stocks/stock_market/corp_notices.php?autono=3137341