Consolidated numbers are not at all bad. Quite impressive with respect to recent price action.

Is there any way to know detail numbers of subsidiary General Graphene? How it is and will contribute in consolidated numbers would be something to watch.

At current price for Graphite India, Market Cap is - 6,355 Cr. Company has a cash of Rs. 2577/- CR. And good part is management is at least declaring it and paying dividend as well.

However, what would be interesting is the expected run rate for earnings in next year based on prevailing and future contracts

Management compensated closed Bengaluru plant employee 55cr and declared as exceptional item expense. Employee friendly and transparent side of management, positive side. Real estate value unlocked by closing the Bengaluru plant land, positive. General Graphene corporation started contributing as subsidiary, will be interesting to see how it is taking shape. Paying good amount of dividend to shareholders, big positive.

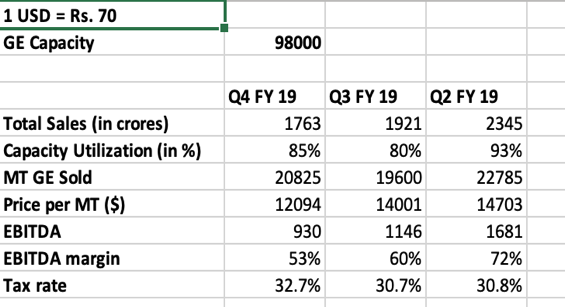

Here is some analysis on GI’s Q4 results:

a) The price per MT, while having dropped from 14K USD to 12K USD, is still quite high. Graftech has given a spot price guidance of 11.8K USD for Q1 FY 20, so sales should remain high for the next quarter too

b) Needle coke prices may be higher in Q1 FY 20 due to continued demand for lithium ion batteries, but is expected to soften going forward as per the GI presentation. Margins will definitely compress. In the GI presentation, it is mentioned that China will be adding an additional 600k tonne GE capacity by 2020. This is huge (more than what China needs for additional EAF steel capacity) and while we do not know the UHP/HP split, the prices of electrodes will most definitely reduce going forward. (1 tonne of steel requires 2-3 kgs of GE). The presentation can be accessed here:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5b869866-ebd0-4f8d-8180-8d6b63299125.pdf

c) While EPS is 28.75 for the latest quarter, it would have been around 33-35 (35 including impact of other expenses) had it not been for one time exceptional items. More analysis below:

- 55 crores related to one time payments to employees in Bengaluru unit (EPS Impact = 2.8)

- Additional depreciation of 10.84 crores related to closure of Bengaluru unit (EPS impact = 0.56)

- Additional taxes of 17 crores; tax rate in Q4 has been higher compared to other quarters (EPS impact= 0.87)

- Other expenses have gone up by 40-45 crores as compared to Q3 FY 19 and Q4 FY 18. This must be related to closure of plant (EPS impact =2 atleast).

d) A massive Rs. 35 dividend declared that is more than 10% of Friday’s closing price. Cash generated in FY 19 has been substantial and company has distributed a large chunk to shareholders.

e) Cash at hand is 2577 crores, of which 684 crores will be distributed as final dividend. Company will still have ~1900 crores in hand. Assuming a stress scenario wherein profits drop by 50% in FY 20 as compared to Q4 FY 19, company will still generate 1200 crores in cash, taking total cash at hand to atleast 3000 crores by FY 20. Friday’s closing market cap was 6321 crores. Stock has taken a severe beating and while it is too early to say whether stock will test its previous highs (it may not any time soon is my opinion), the current valuation looks inexpensive

7 Likes

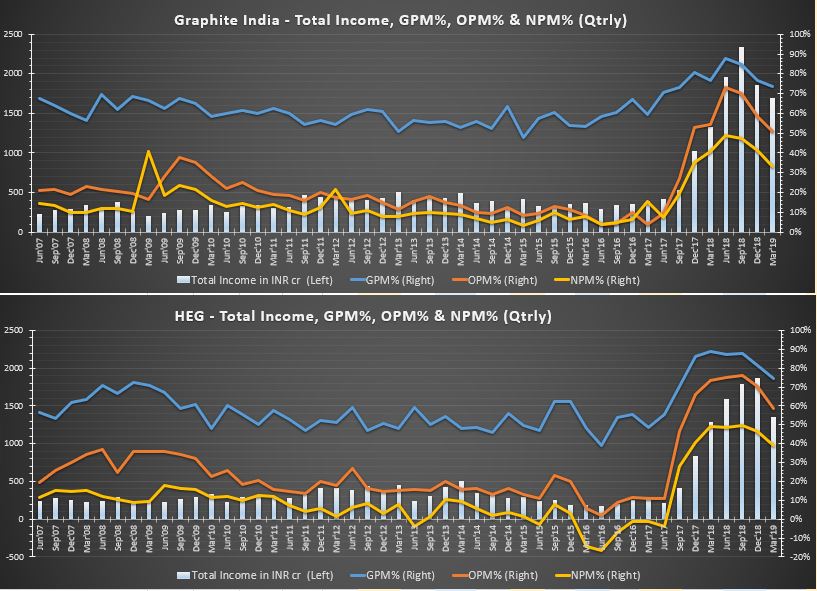

Some charts to chew (particularly for new members at ValuePickr/ Screener, in case they find stock attractive on P/E and/ or Dividend Yield basis).

3 Likes

thanks , Sandeep from which website is the above chart obtained

Roomy, chart has been put together using simple MS-Excel; not an online website snapshot. Cheers.

Somewhere in ValuePickr, read that, OPM% is a good parameter to see where the cyclicals stocks in the cyclical swing (If I’m not wrong, it must be from Jiten P). The entry and exit are very much visible in the chart, based on OPM%.

@spatel : The charts you have posted are not providing any further incremental information than what is already known. Yes, the margins are dropping and so is share price. This does not mean that we will encounter a situation like 2015-2016 where margins are 0-negative, and GI reaches double digits. (and HEG touches 500)

Here is a lot more information for new Valuepickr members as well as experienced members to think about:

P/E is irrelevant as it is difficult to estimate forward earnings beyond a quarter or two given the information at hand on supply from China. What is relevant though is comparison of multiples across different GE companies, but even that is quite dynamic. Further, competitors have different business models: Either, they are diversified into other carbon businesses or vertically integrated. This makes relative valuations difficult.

Dividend yield is definitely attractive, but the question is: Is it attractive enough? Here are some Pros and Cons:

Pros:

- Dividends means that profits are real

- Company is demonstrating “share-holder friendliness” given the intention of distributing profits to shareholders

Cons:

-

What if, instead of giving out dividends, the company had announced plans to diversify, like either being vertically integrated like Graftech, or perhaps a partnership with a EV battery maker?

-

Better still, would it not have been even more valuable to shareholders, if GI announced share repurchases from the open market (like Infosys). Instead of spending 700 crores in dividends, what if GI bought more than 1 crore shares from the open market till a max price of 700? This would have brought in much more value to shareholders than 35 Rs per share in dividends (Promoters would have

gained too given their increased stake in the company) -

Cash reduced means that the company has less cash to invest in the future.

The key question to ask is: Is it worthwhile to even attempt to catch the proverbial “falling-knife”?

If the belief is that China will flood the market with UHP GE immediately and worse-still, steel demand will reduce and further, both the GE companies are incapable of putting the cash-at-hand to judicious use, then yes, GI will go back to double digits and HEG to 500.

While anything is possible, how probable is the above scenario? If you think the probability is high, then better avoid these stocks.

I think that the probability of the above scenario is quite low. These are some important points to consider:

- HEG management has given a guidance of maintaining similar sales for FY 2020 as Q4 FY 2019, as they are confident of maintaining a relatively high UHP price per ton. They also think that utilization can be increased to 90% from the current 80%. This means that while margins will reduce, the reduction may not be drastic. You can access the interviews here:

-

While GI has mentioned that China will add 0.6 million tonnes of GE capacity, they have also said that: “The needle coke industry is highly concentrated, and the demand is growing due to its use in lithium-ion batteries. Hence, availability of additional needle coke at a reasonable price only shall determine the effective utilization of any meaningful addition to electrode capacity across the industry”. Further we do not know the UHP/HP split.

-

While it is difficult to believe that China will never have the technological capabilities to produce UHP GE, it will not happen overnight either. I am guess-estimating a year’s time at least, by when Chinese suppliers will start competing with UHP GE manufacturers, resulting in substantial margin compression.

-

GI has BVPS of Rs. 274. This is driven primarily by cash and not by intangibles like goodwill, questionable receivables or inflated inventories. Net Cash works out to Rs, 132 per share. The Bengaluru plant is non-operational, and all dues have been paid. It is unlikely that Karnataka State Pollution Control Board will give approvals for any manufacturing activities as the plant is in the middle of a residential area filled with apartment complexes. The land might be monetized and could be worth anywhere between Rs, 25-40 per share (per online sources). As mentioned earlier, FY 2020 could generate Rs. 100-120 per share in cash, going by HEG mgmt.’s guidance. Given all this information, share price might not go below book value.

-

Further, both HEG and GI management are competent and capable of generating value. GI has been profitable during troubled times and paid dividends more often than not. HEG has generated more profits than GI despite having lesser capacity over the last year. HEG has played the GE cycle extremely well. With capable management at the helm, both companies should be able to use cash to drive more shareholder returns.

-

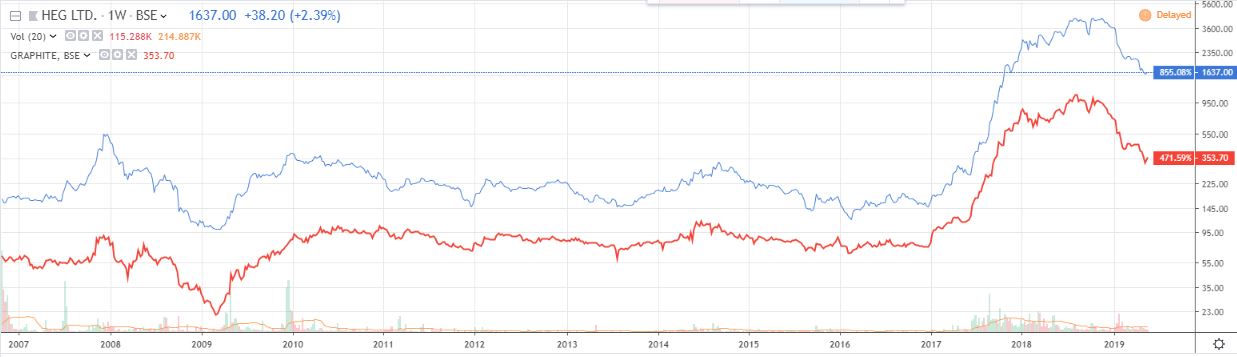

Looking at technicals:

For GI, 275-280 zones happen to be a fairly strong support area. If things go haywire, this support might be tested and should hold (It is also the BVPS). Resistance zones are 375, 395-405, 415, and 475-480. Of which, 395-405 will pose to be a strong resistance, as the stock took support here multiple times before breaking it. GI is already 17% up from its low of 309 and is at 361.

For HEG, 1920-2000 zones will be stiff resistance. 1840 is another resistance area. HEG is up 9% from its low of 1540

Putting the above information together, if you are an investor here, regular profit booking is advisable, especially at the stiff resistance zones described above. Keep some funds aside in case GI breaks to the downside and tests 275-280 or breaks to the upside conclusively beyond 395-405 (or 1920-2000 for HEG)

4 Likes

Some facts about Graphite Electrode -

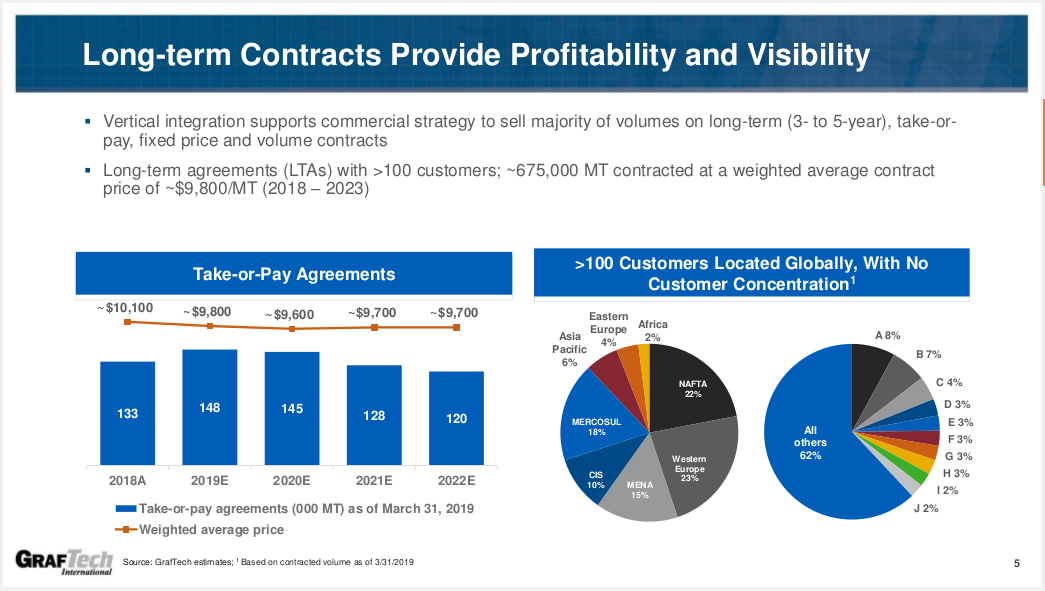

- Graftech in it’s Jan-Mar earnings presentation said that they have take-or-pay contract for 120k ton at price of $9,800/ton till 2023.

-

HEG after Jan-Mar quarter earnings said that their plant worked at 80% capacity utilization with average realization of $12k/ton and they are looking at similar trend for Apr-Jun 2019 quarter.

-

HEG said they are looking at 90% capacity utilization in financial year 2020. Assuming,

90% capacity utilization

$12k/ton realization

Needle coke prices remain same as in jan-mar 2019 quarter → Net margin = 38%

fy20 revenue = 6048 crore

fy20 net profit = 2298 crore

therefore,

fy20 EPS = 595

PE @ 1850 = 3.1

Disclaimer - Invested therefore views are biased.

2 Likes

There is a difference between Graphite Electrode and Graphite players. In my view we should not mix the two . Heg and GI are primarily GE players

1 Like

Some thoughts and analysis:

@aammiitt2, The information that you have posted is not relevant to Graphite Electrode (GE) manufacturing companies.

The term “Graphite” could mean different forms/variations of graphite, and they all have different properties resulting in varied applications.

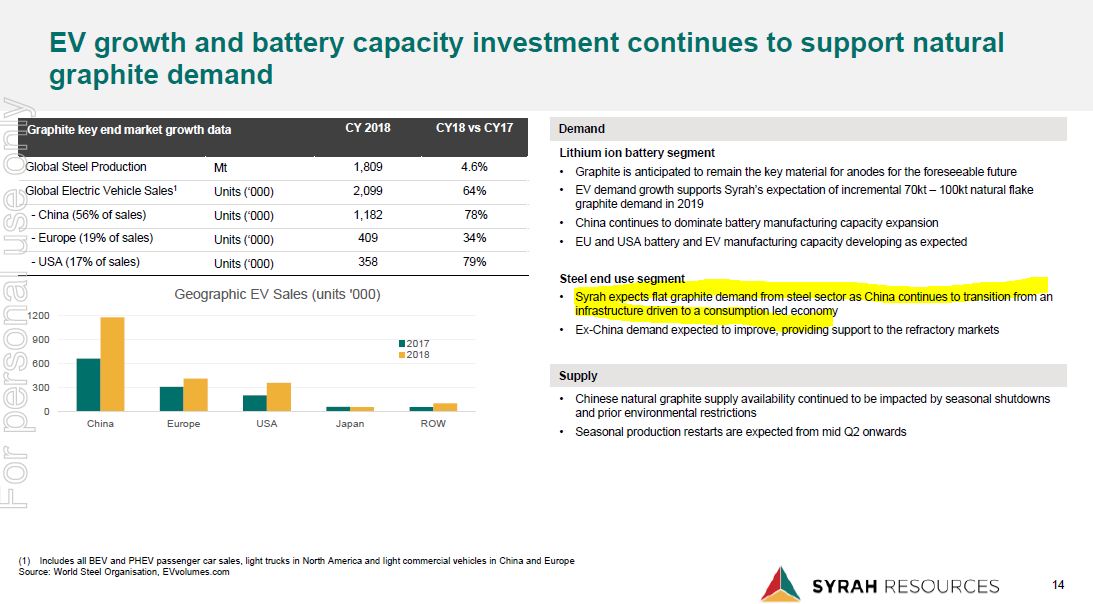

Broadly speaking, graphite can be divided into two kinds: Natural and Synthetic. Syrah Resources produces natural graphite. Graphite flakes also belong to this group. GE is a form of synthetic graphite, which is much more expensive, as it is purer (less sulphur for instance) and has a low coefficient of thermal expansion (can withstand high temperatures without deforming making it ideal for electric arc furnaces). For these reasons, synthetic graphite is also preferred for making anode materials that go into EV batteries.

In the slide displayed above, Syrah Resources is saying: “They expect flat graphite demand from the Chinese steel sector”. This is in fact good news for GE companies. Natural graphite is also used in the steelmaking process. It is used to build refractory linings in blast/EA furnaces and is added to steel to increase the carbon content and thereby its strength. Since China has been reducing its steel manufacturing from CY 15- CY 18 and closing factories with blast furnaces to keep pollution in check, the need for natural graphite has correspondingly reduced. That is what Syrah is saying. The rest of the world excluding China has been producing more steel to compensate (GI and HEG export electrodes to the rest of the world) and given that roughly half of this production comes through the EAF route, the requirement for UHP grade GE should continue to exist. Further, protectionist measures against Chinese steel exports could result in more steel production from the rest of the world benefiting the GE companies.

GE is produced from two different kinds of needle coke: Petroleum based (as a part of the oil refining process) and coal tar based. GE requires high quality needle coke and the one derived as a part of oil-refining is produced only by a few refineries in the world (either based in US like Phillips-66 or Seadrift/Graftech or in Japan). This variety of needle coke is also used to produce synthetic graphite that goes into lithium ion batteries. Synthetic graphite is preferred to natural graphite in batteries though a mix is used (Syrah is saying that natural graphite production/demand will be driven by EV batteries). Given the tight supply situation of needle coke due to competing priorities (GE, batteries), margins for GE companies might shrink because of increased costs. China has needle coke manufacturing setups but they are primarily coal tar based. Refineries are trying to manufacture petroleum needle coke but this is easier said than done. It will take a sizable investment, time, technological expertise and environment related regulatory clearances for new needle coke plants, particularly the coal tar-based ones. Further, China has the world’s largest number of Battery/Plug-in Hybrid (BEV, PHEV) based electric cars and buses and this is expected to increase, which will further fuel demand for needle coke. New GE capacity in China is meaningless unless good quality needle coke is available at a reasonable price, which is what the GI presentation was saying. Further the capacity is HP grade. In the HEG conf. call, the management has mentioned that the needle coke contracts are in place till June. The process to manufacture GE takes six months. The current contracts should cover GE manufacturing till the end of the year.

Putting all of this together, I think that a relatively high ASP for UHP GE can be maintained as long as the steel cycle (particularly for the rest-of-the-world excluding China) remains in an uptrend. HEG mgmt. also said that steel companies stocked up on UHP GE given the shortage witnessed in the second half of last year, and the inventory will be used up in around 3 months. Needle coke availability at a reasonable price could most probably be an issue, and this will keep the capacity utilization of existing GE players in check, but as long as increased costs can be reflected in ASP, margins should not deteriorate drastically.

3 Likes

1 Like

I am surprised by the omission of several current day facts like addition of new GE capacity in China , 5 yr length of Contract for all GE manufactures (only Graftech has signed long term contracts)

How much capacity has been added in China?

Doesn’t this indicate the demand scenario for graphite electrode? Why would anyone sign a take-or-pay contract for 2022 @ $10k/ton if there is possibility of getting it cheaper from elsewhere?

news share