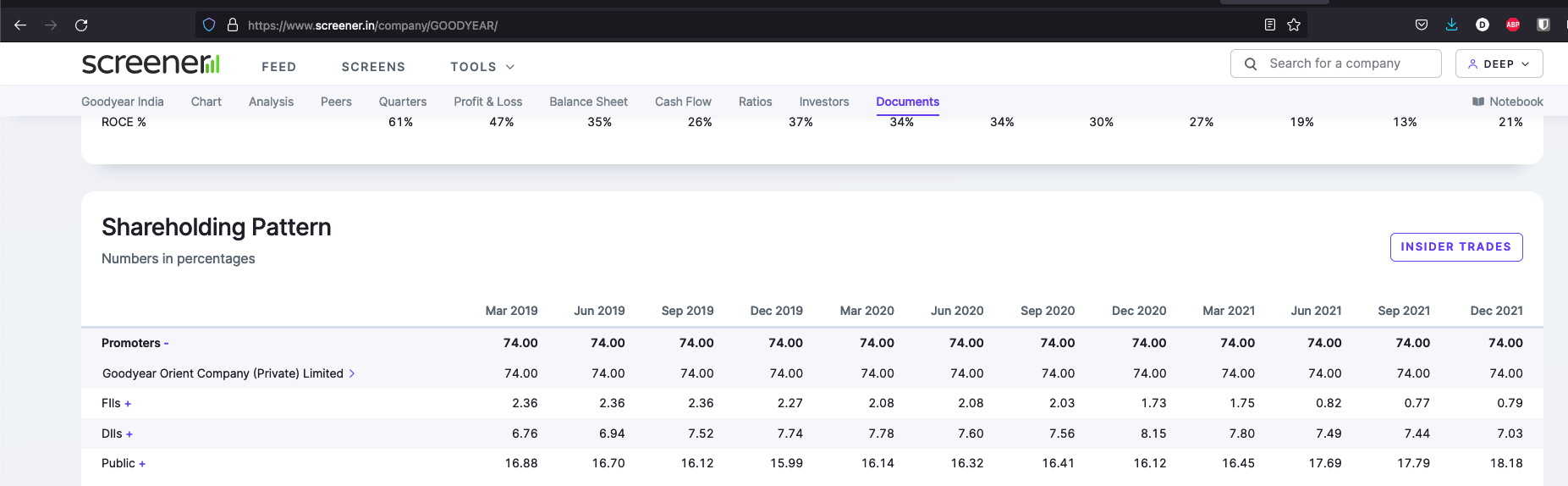

I haven’t read the annual reports, but cursory looks show that the Indian company is a majority owned subsidiary of Goodyear Orient Company (Private) Limited (See Shareholdings section in screenshot below)

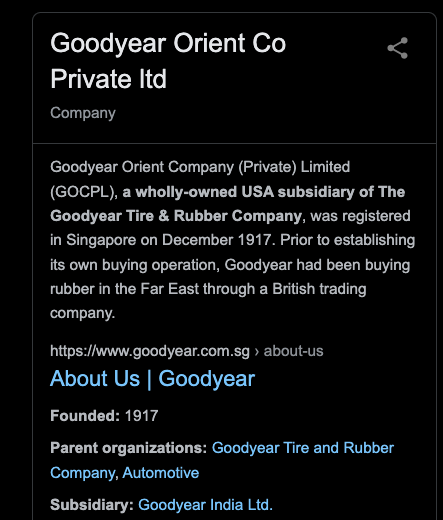

which in turn is a a wholly-owned USA subsidiary of The Goodyear Tire & Rubber Company, was registered in Singapore on December 1917

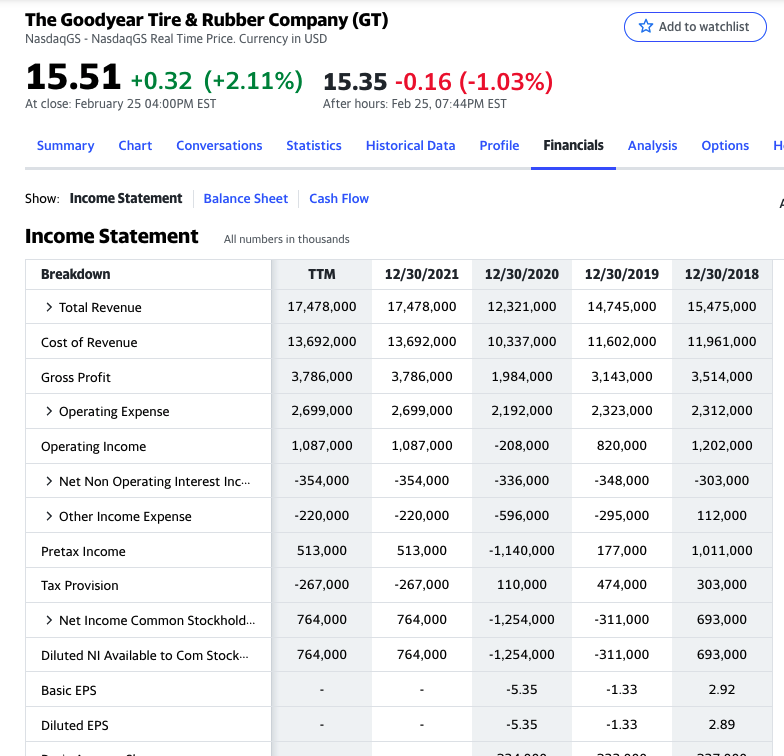

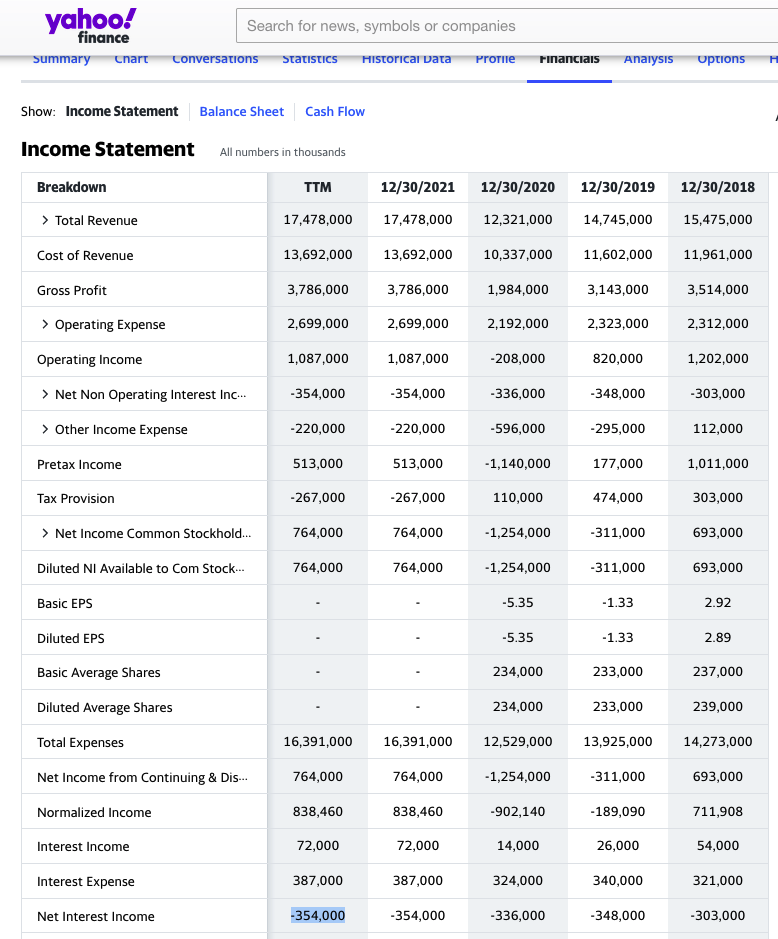

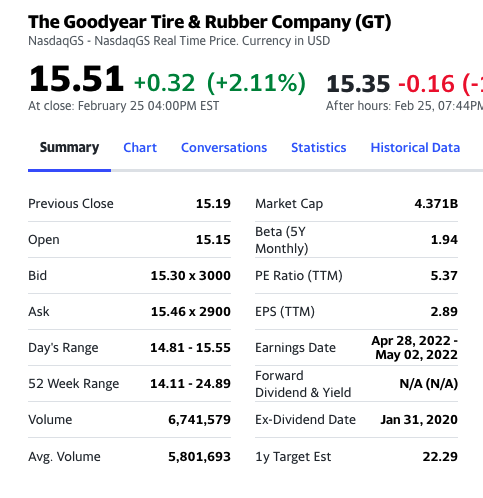

And the ultimate parent company, The Goodyear Tire & Rubber Company is heavily indebted and was in losses recently (previous two years before the year ended Dec 21)

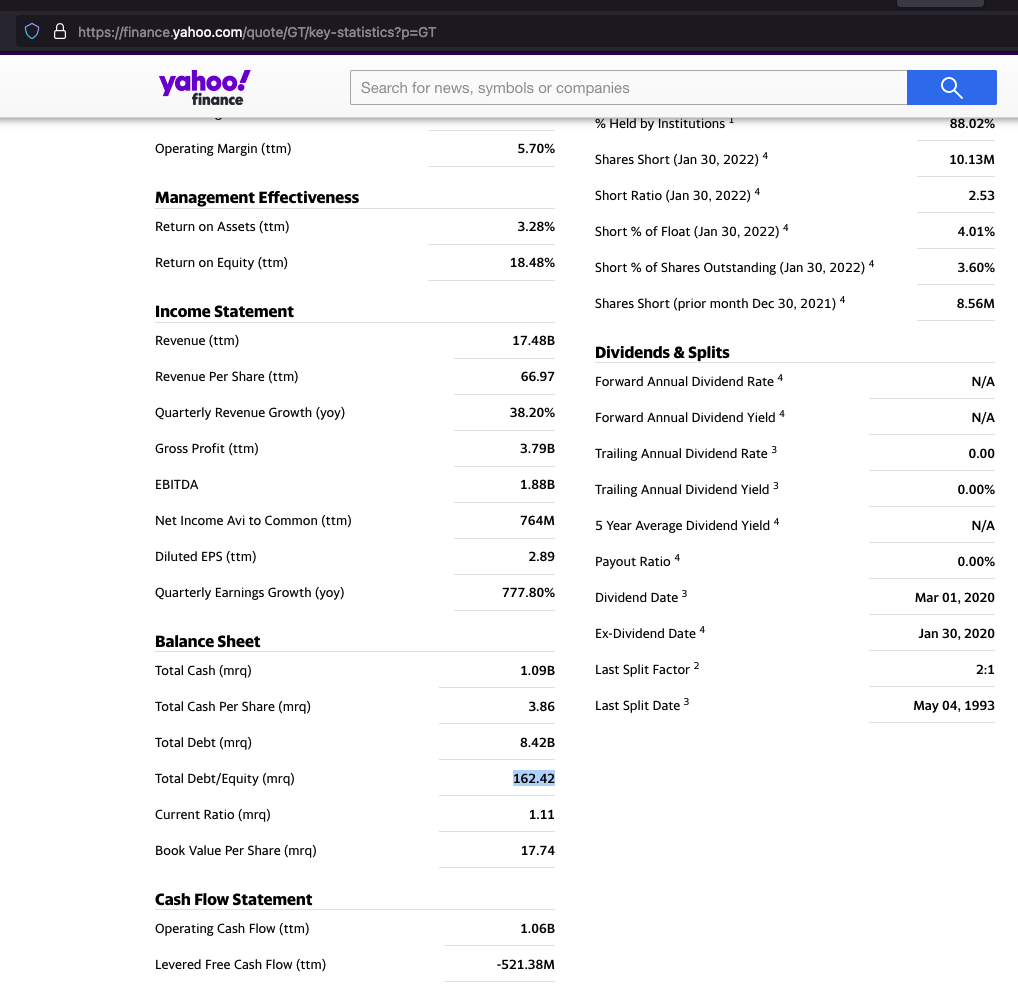

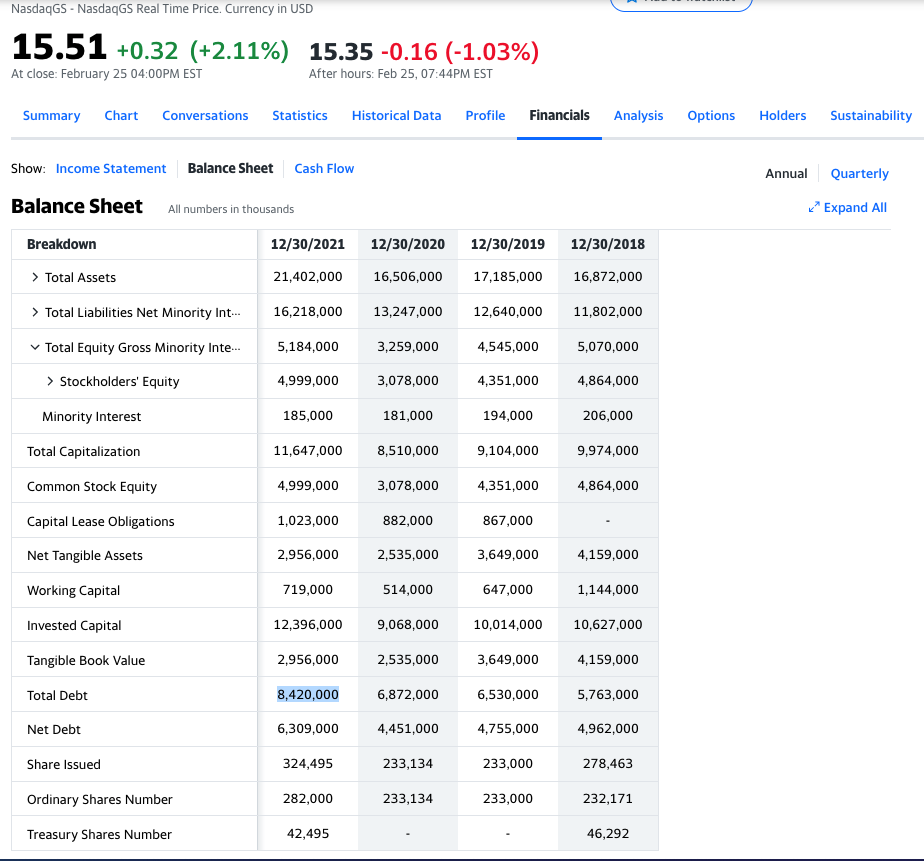

The parent company has total debt of USD 8.4 billion, ~63063 INR crores (30x the market cap of indian entity) against total equity of USD 5.2 billion (Hence debt is considerably higher than the equity)

Now Barron’s, in a recent article, says the parent would probably benefit from the EV boom, but I assume for the foreseeable future, this benefit would remain with Goodyear parent, and won’t cascade to Indian as in India, they don’t have that strong a standing in passenger vehicle segment.

Also at a business level, it further goes on to talk about somewhat dark times in near future due to increasing raw material costs, natural rubber costs, etc. But all these could be put aside as these might be short term gyrations. What makes it difficult to put aside though is, this company is a net cash negative incurring huge debt expenses. Hence the impact of short term gyrations could magnify depending on how extreme are these gyrations.

Lastly, it doesn’t inspire confidence of management being a good capital allocator. Why are they paying special dividends at a subsidiary level while their interest expense at parent company level is almost half of their Net Income?

(Notice Net Interest Income of -354000 against Net Income of 764000)

Summary

All in all, a company whose:

- Parent is not generating consistent profits (looking back past few years),

- Is heavily indebted, net cash negative (See Barrons) with possible near term negative consequences that could magnify due to large debt expense.

- Paying special dividends at subsidiary level and

- To top it all, at a parent level, is trading at a valuation much cheaper (in terms of earnings multiple) than its subsidiary (US entity is trading at 5x trailing earnings) despite being well discovered by market and several analysts following it (See Barron’s article linked above)

PS: I might be wrong as I am just trying to understand the larger org structure before I jump into its ARs. If you believe so, please ignore these thoughts

I just came across this through Barron’s, no holdings.