ValuePickr Research

Resources

Basics

ValuePickr Forum

GNFC - The big becoming bigger!

Stock Opportunities

Chumantar

September 19, 2022, 12:18pm

348

image

521×585 154 KB

1 Like

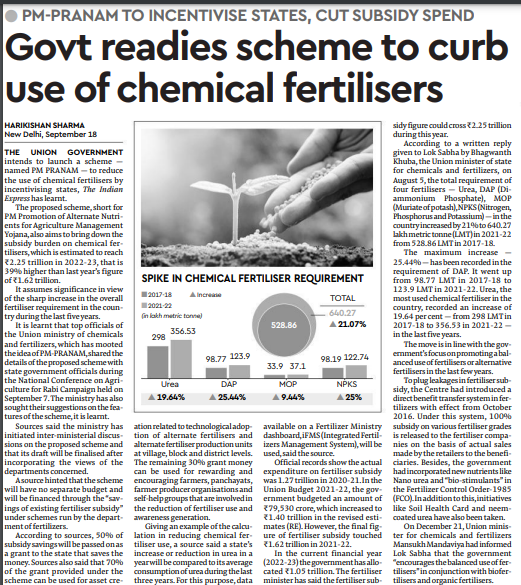

show post in topic